Research — 13 Aug, 2024

Bonding with Style Investing: Value and Momentum in Corporate Bonds

By Temilade Oyeniyi and Amritpal Sidhu

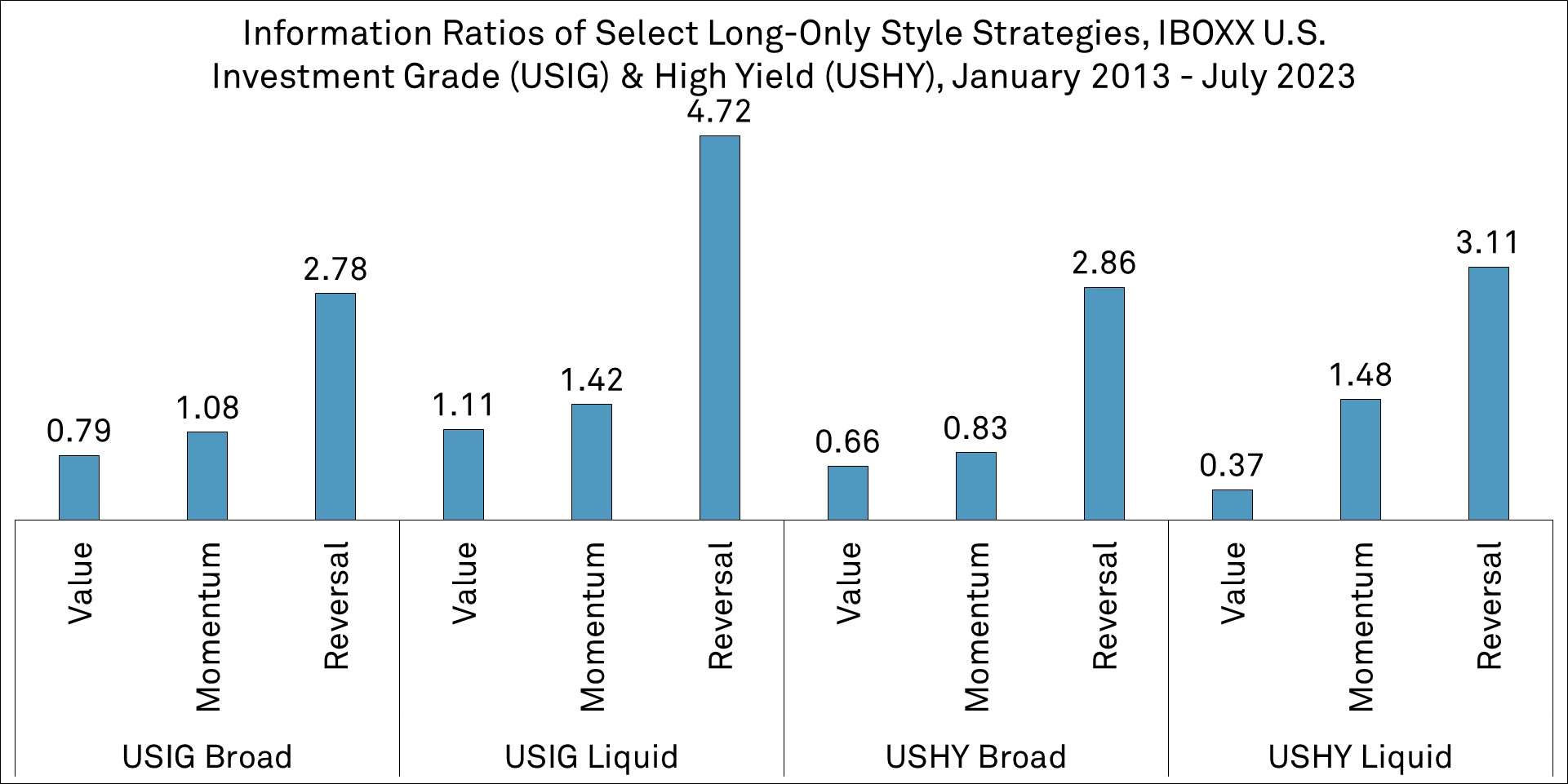

The application of 'smart beta' strategies is expanding into corporate bonds, beyond its equity roots. This paper explores value, momentum, and short-term reversal styles in fixed income, highlighting the potential to enhance returns and diversify portfolios. The analysis shows that value and momentum strategies in iBoxx U.S. investment-grade (USIG) and high-yield (USHY) bonds generated statistically significant alpha, with low correlations to the comparable equity styles and markets premia.

VIEW THIS PAPER’S SOURCE CODE

(with your S&P Global Marketplace Login)

Source: S&P Global Market Intelligence Quantamental Research. Data as of July 2023.

Key research findings include:

- Value and Momentum: Back-test results show long/short USIG (USHY) value and USIG (USHY) momentum styles delivered 2.0% (2.7%) and 1.1% (4.7%) annualized alpha respectively, after controlling for common equity styles and markets risk premia.

- Momentum and Liquidity: Momentum performed better in the liquids bond universe relative to the broader bond universe with an annualized 0.4% in the USIG and 0.9% in the USHY.

- Low Correlations: Returns to value and momentum styles have historically shown weak correlations with commonly used style factors including equity styles. Correlations range from -0.3 to 0.3, suggesting diversification benefits.

- Value, Momentum and Credit Rating: Value performance strengthened as spread dispersions widened from AAA to BB ratings. This advantage diminished in B ratings, as default risk subsumed the value premium. The momentum signal proved more effective in lower rated credit with more room for price appreciation.

Explore the data used to conduct this research

S&P Global Market Intelligence bond pricing and liquidity data forms the basis of bond returns and liquidity-related robustness checks. Bond pricing data is updated daily covering US, European and Asian corporate bonds with historical records available since January 2013. We used the following S&P Markit iBoxx fixed income indices and their analytics in signal and factor portfolio construction.