15 Feb, 2023

USAA Federal Savings Bank's growth reverses amid recent regulatory tumult

By Lauren Seay and David Hayes

USAA Federal Savings Bank's total assets shrank in 2022, ending a decadeslong streak of steady growth at the privately held company, which has been grappling with a series of regulatory challenges in recent years.

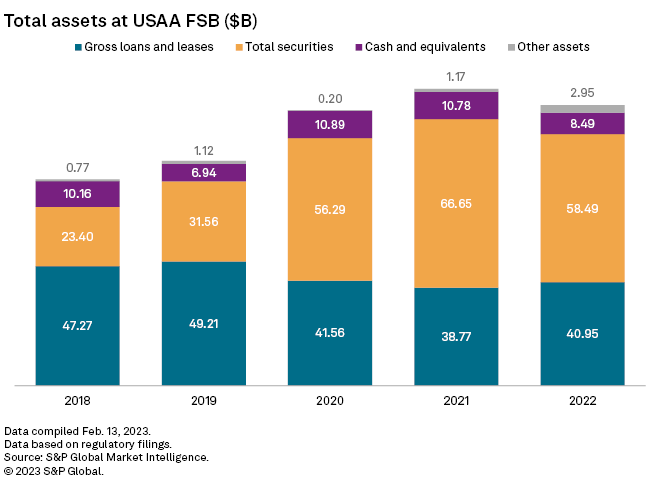

USAA FSB posted total assets of $110.88 billion at Dec. 31, 2022, down 5.5% from the end of 2021 when it reported $117.37 billion in assets. The decline bucks the trend of consistent year-end asset growth for the bank since at least 1990

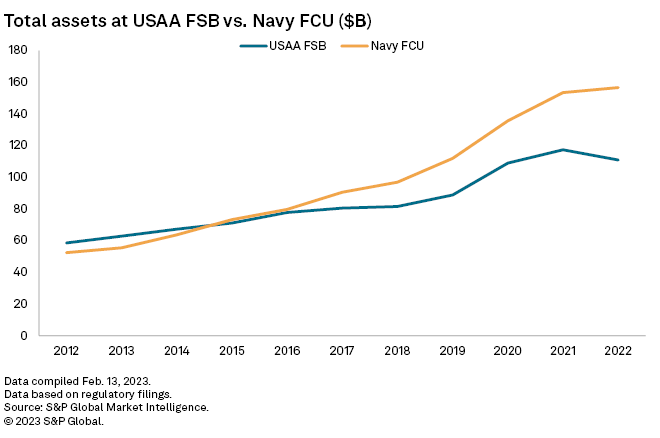

USAA FSB's growth has not only slowed compared to a group of peer banks but also compared to Navy FCU, a credit union aimed at serving the same customer base as USAA FSB: military members and their families.

USAA FSB and Navy FCU were around the same size at the end of 2012, when USAA FSB had $58.60 billion in assets and Navy FCU had $52.44 billion in assets. However, Navy FCU's growth has outpaced USAA FSB in recent years, and Navy FCU now has $156.65 billion in assets compared to USAA FSB's $110.88 billion. In the decade between 2012 and 2022, Navy FCU's assets have grown 198.7% compared to USAA FSB's 89.2% growth.

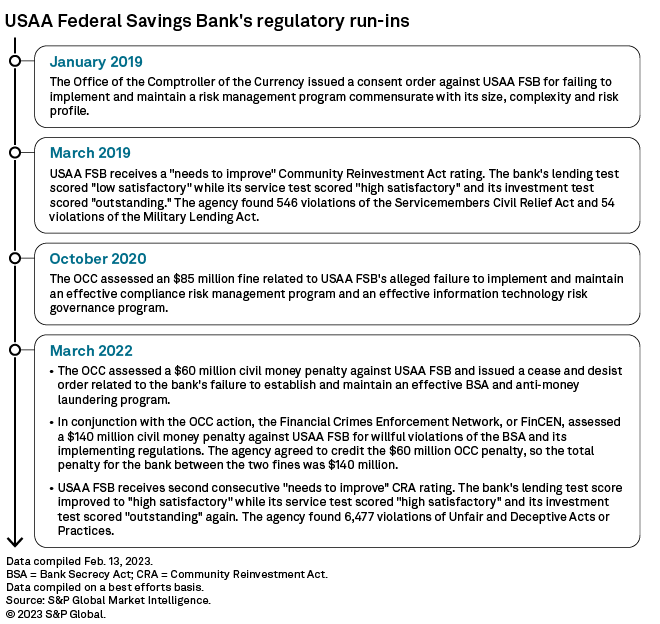

The slowdown in growth compared to peers comes amid a string of regulatory trouble for USAA FSB in which the San Antonio-based bank has received flak over compliance with its risk management, governance and Bank Secrecy Act/anti-money laundering, or BSA/AML, and Community Reinvestment Act, or CRA, programs dating back to 2019. In a statement, USAA FSB spokesperson Roger Wildermuth said addressing regulatory issues "has been and remains a top priority at USAA."

When asked about whether the bank's regulatory situation has impacted its growth, Wildermuth said in a statement that "USAA FSB is a strong and growing bank that is focused on serving our members in a compliant manner."

However, it is not uncommon for banks dealing with compliance matters to face growth restrictions, and the issues can weigh on expenses, capital and regulatory ratings, advisers said in interviews with S&P Global Market Intelligence. The challenges cited by the advisers underscore the cascading effect institutions can face once they end up in regulatory hot water.

Indirect growth restrictions

While regulators do not place formal growth restrictions on banks, growth is indirectly stifled because regulators will not approve applications for things such as whole-bank M&A, branch acquisitions or branch expansions.

As such, "you're kind of stuck to just operating where you're at," said Stephanie Kalahurka, a partner at Fenimore Kay Harrison, in an interview speaking broadly rather than about one institution.

Moreover, regulators may informally tell banks to hold back on growth until the bank has addressed concerns, according to John Geiringer, a partner in the Financial Institutions Group at Barack Ferrazzano Kirschbaum & Nagelberg LLP.

"Even if a regulator does not explicitly restrict a bank's growth through an enforcement action, it may informally tell the institution to avoid significant organic growth, new products or services, and fintech relationships before addressing any identified weaknesses," he said.

Particularly, when a bank experiences regulatory issues related to BSA/AML, CRA or other compliance weaknesses, it is more likely to be precluded from engaging in expansionary activities, advisers said.

USAA 'needs to improve' CRA some more

Toward the end of 2022, the Office of the Comptroller of the Currency, or OCC, released USAA FSB's latest CRA exam results from March 2022, revealing that the bank received a "needs to improve" rating for the second consecutive time.

Even though the overall CRA rating stayed the same, USAA FSB's individual performance test ratings showed improvement from its prior exam. The company's 2022 lending performance test — the component that holds the most weight with regards to a bank's overall CRA rating — was "high satisfactory," an improvement from "low satisfactory" on the prior exam. The company's investment and services tests remained the same at "outstanding" and "high satisfactory," respectively.

However, the OCC uncovered nearly 6,500 violations of Unfair and Deceptive Acts or Practices due to the company not providing promised rate discounts on auto loans during the recent exam.

In the statement to Market Intelligence, Wildermuth said the company's CRA rating was adjusted due to "unrelated issues with a product that USAA discontinued in 2020."

USAA is hardly the only bank to face consecutive subpar ratings on CRA. Eight of the 15 banks or thrifts that received a "needs to improve" or "substantial noncompliance" CRA rating in 2022 also received a "needs to improve" rating in their previous exam.

BSA/AML can 'take years to fix'

Advisers said banks can face scrutiny for a while because improving internal controls takes time, and those improvements can lead to the identification of other issues.

"As you upgrade your systems and your reporting and your risk management, you can also find other things that have been missed by both the bank and the regulators before," Chip MacDonald, managing director of MacDonald & Partners LLP, said in an interview.

Specifically, BSA/AML issues "take years to fix," MacDonald said, and regulators want to see concrete progress before a bank is let out of the dog house.

"You've got to have multiple exams where the examiners come in and say, 'Show me what you've done and why you still don't have problems,'" MacDonald said. "And their tolerance is close to zero. You've got to really show them what you have done and accomplished. It's not what you're trying to do, it's what you've actually accomplished."

Trickle-down effect

Regulatory issues can hurt a bank's capital and funding positions, which has the effect of limiting growth.

For instance, many counties, cities and school districts have restrictions in their charters that their deposits must be held at an insured financial institution with at least a satisfactory CRA rating, according to Kalahurka. This issue is more common for community banks, she noted.

"We've had some institutions get downgraded and then not be able to bid on those deposits the next time around," she said. "If you lose a large public fund deposit that you've had for years and years, that can hit liquidity."

When it comes to BSA/AML, regulators can require companies to retain more capital than minimum requirements, if they feel banks pose an outsized risk related to their controls, according to Kalahurka.

A poor CRA rating or BSA/AML trouble will also likely hurt a bank's CAMELS rating, which measures capital adequacy, asset quality, management, earnings, liquidity and sensitivity on a scale of one to five, with five being the worst.

For USAA FSB, its recent string of regulatory troubles has likely weighed on its management rating, advisers said.

"It's got to adversely affect their management rating," MacDonald said.

The repetitive nature of USAA FSB's violations could adversely impact the company's management rating specifically, advisers said. Though the bank's individual CRA performance tests improved, the OCC noted in the 2022 exam that "management did not improve the bank's CRA performance with respect to compliance risk management from the last evaluation." Similarly, in the Financial Crimes Enforcement Network's March 2022 consent order regarding BSA/AML, the agency said the OCC began informing USAA FSB it had "significant problems" with its AML program in 2017.

Throwing money at the problem

Regulatory issues can often come with multimillion-dollar civil money penalties, but the costs associated with improving compliance also add up quickly.

"It can get very expensive just in terms of the amount of staff and resources to be allocated to that, and it can also just be a real distraction from what would be your normal day-to-day loan and deposit business if we're having to overhaul systems," Kalahurka said.

In addition to the cost of new technology and systems, another costly expense is hiring compliance professionals and executives.

"Compliance people are expensive these days. They're in short supply and great demand," MacDonald said. "But you've got to throw resources at it to solve the problem."

USAA FSB reported $5.87 billion in noninterest expenses in 2022, down from $6.12 billion in 2021 but up from $3.89 billion in 2017 prior to its string of regulatory issues.

USAA FSB is currently searching for a head of bank CRA program and strategy, according to a job posting on its website from Jan. 18, and it brought on a new chief risk officer in 2021.

Positions like those are "probably part of the solution" and done to "implement change," MacDonald said. "Regulators take that into account," he added.