9 Jul, 2021

US corporate debt levels fall as revenues recover from pandemic slump

By Peter Brennan and Tayyeba Irum

U.S. companies reduced debt levels and largely continued to improve their ability to service loans in the first quarter of 2021, according to the latest data from S&P Global Market Intelligence.

Companies took on debt in 2020 to plug the gap in their balance sheets left by missing revenues as the COVID-19 economic crisis took its toll. But as revenues recover amid the broader economic resurgence, those debt levels have fallen closer to pre-pandemic levels.

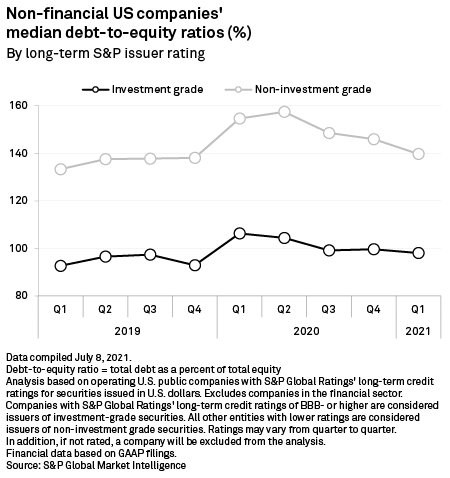

The median debt-to-equity ratio — a measurement of corporate leverage whereby total liabilities are calculated as a percentage of shareholder equity — of U.S. investment-grade rated companies fell to 98% in the first quarter of 2021. The ratio climbed to a peak of 106.3% during 2020 from 92.9% before the crisis.

|

For the non-investment-grade universe — companies rated BB or lower —the recovery has been even more comprehensive. A debt-to-equity ratio of 139.7% in the first quarter was only slightly higher than the pre-pandemic level of 138.1% and well down on the crisis peak of 157.5%.

"The outlook for U.S. companies is fairly constructive, bar a massive relapse in the COVID situation," said Greg Venizelos, senior credit strategist at investment management company AXA IM, in an interview.

Better positioned to repay debts

The rate of defaults among U.S. companies had been expected to surge when the crisis struck, but the low cost of borrowing and improving corporate revenues have, for now at least, removed that concern.

"The overall levels of debt are extremely manageable," Christopher Rossbach, manager of the J. Stern & Co. World Stars Global Equity Fund, said in an interview. "The cost of debt is very low, so the capacity of companies to take on leverage is very high. You're seeing that in [increased] mergers and acquisitions and accelerating investment."

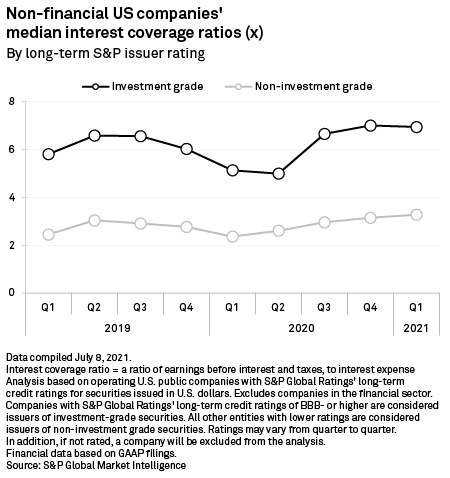

The median interest coverage ratio — a measure of a company's ability to repay its debts calculated by dividing earnings before EBIT by the cost of its debt-interest payments — improved in the investment-grade segments of eight of the 10 sectors, excluding financials, that Market Intelligence tracks.

|

For all investment-grade U.S. companies, the median ratio was 6.9 in the first quarter of 2021, meaning their earnings cover their interest payments 6.9 times over. This was up from 5.1 a year earlier and higher than the pre-COVID level of 6.

Similarly, lower-rated, non-investment-grade companies were able to cover their interest costs 3.3 times over in the first quarter, up from 2.4 a year earlier and 2.8 times before the pandemic.

The broad-based recovery now includes the energy sector, which had been lagging but has now been buoyed by a strong recovery in oil prices that have more than tripled since the lows of March 2020 as global demand recovered.

The interest coverage ratio for investment-grade-rated energy groups rose to 4.6 in the first quarter of 2021, up from 3 in the previous quarter. The ratio had slumped to a low of 2.4 from a pre-pandemic level of 4.5 as the world economy ground to a halt, reducing oil consumption.

Credit conditions 'extremely favorable'

Credit conditions for North American companies are "extremely favorable" according to S&P Global Ratings' outlook for the third quarter of 2021, "underpinned by investors' continued thirst for yield and a strong economic rebound."

The rating agency said the boost in sales from the reopening economy was allowing companies to return to pre-pandemic revenue levels sooner than expected.

Meanwhile, borrowing costs are low, even for non-investment-grade-rated companies. The yield-to-worst — a measure of the lowest possible yield on a bond assuming the issuer does not default —

|

The Federal Reserve's ongoing ultraloose monetary policy, which sees the bank buy up billions in bonds each month and provide a liquidity backstop, in addition to private investor demand, has kept borrowing costs low.

All of this means the expected default rate continues to decline. Ratings' trailing-12-month, non-investment-grade corporate default rate forecast — which predicts the percentage of the total non-investment-grade debt volume that will default — is 4% by March 2022, down from 6.3% as of March 2021.

But risks remain, particularly if inflation persists and forces either a tapering in the Federal Reserve's $120 billion-per-month asset purchasing program or a rise in interest rates. The minutes of the rate-setting Federal Open Market Committee meeting in June showed that Federal Reserve officials may ease purchases earlier than they had anticipated.

Axa's Venizelos said tapering will result in a mild widening of credit spreads by some 5%-10%, increasing the cost of borrowing for companies. But if inflation persists for longer than the Fed has indicated, the market reaction could be significant.

|

"A years' worth of elevated inflation is transitory. If it's five years that's a different scenario. Then the Fed will be seen as being behind the curve in that respect and there will be a massive repricing," Venizelos said.

The U.S. core personal consumption expenditure price index rose to 3.4% in May, the highest it has been since August 2008 and significantly higher than the Federal Reserve's target of 2%.

"The prospect of uncomfortably high inflation could be one catalyst for investors to reset their risk-return demands, resulting in the repricing of assets, higher debt-servicing costs and tighter financing conditions," Joe Maguire, lead research analyst at S&P Global Ratings Research, wrote in the agency's third-quarter credit outlook report.