23 Jan, 2023

French banks face further income squeeze as regulated savings rate rises again

| France's Minister for the Economy, Finance and Recovery Bruno Le Maire announced the increase to the Livret A Feb. 13. |

France's largest banks face added pressure on their income following a government decision to increase the rate on the popular Livret A regulated savings scheme by 100 basis points to 3%.

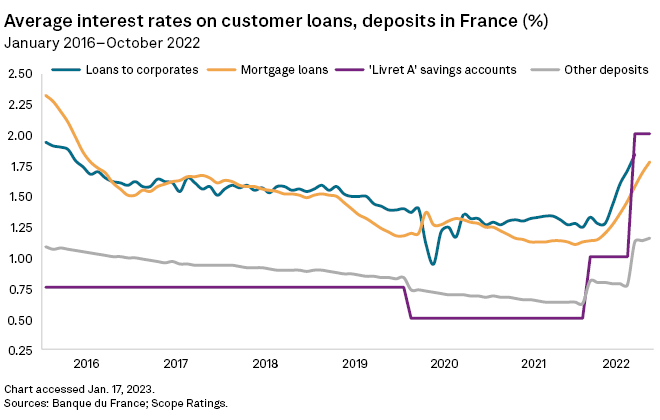

The latest hike to the rate, announced Jan. 13 and which takes effect Feb. 1, means deposit costs on Livret A accounts have increased by 250 bps for French banks since February 2022. The Livret A rate also provides a benchmark for rates on other popular regulated savings products in France, representing hundreds of billions of euros in additional deposits.

"The Livret A dampens French banks' profitability," Johann Scholtz, bank equity analyst at Morningstar, said in an interview. "It's one of the reasons all French banks still battle to get consistent, double-digit returns on equity."

The latest increase to the Livret A and other regulated savings accounts' rates will cost French banks almost €2.4 billion in additional deposit costs, according to Fitch Ratings. This represents around 1.4% of annual net banking income for the French banking sector and 4% of annual NBI for retail banking activities, Fitch said.

The increase in deposit costs for French banks comes as other revenue headwinds mount. The largely fixed-rate profile of their loan books means they are yet to see the same surge in lending income that many other European banks did in 2022.

French banks are also expected to reveal a slowdown in income from other streams such as investment banking, asset management and vehicle leasing — all of which helped produce bumper profits in 2021 — when full-year 2022 results are announced in February.

Strong inflows

Inflows into Livret A accounts, which are tax-free and can hold up to €22,950, have surged in the last year as the rate has risen. Some €25.78 billion was deposited into the accounts in first 11 months of 2022, much from life insurance accounts that offer lower rates.

France's largest listed lenders have varying degrees of exposure to regulated savings accounts. Société Générale SA had the largest portion of regulated deposits as a share of total customer deposits, at 14.4% as of the end of September, according to bank data and Jefferies. Crédit Agricole SA, or CASA, and BNP Paribas SA had just under 10%.

SocGen's greater reliance on French retail banking for its revenues and profits also means increases to the Livret A rate have a more significant impact on it than its domestic peers. Domestic banking comprised almost 33% of operating income and around 27% of pre-tax profit for SocGen in 2021, the last full-year for which data is available, Market Intelligence data shows. This compares to just over 16% of operating income and almost 14% of profit before tax for CASA. BNP's French retail banking business generated 13.5% of revenues and 8.4% of pre-tax profits in 2021, according to company filings.

Regulated savings accounts at CASA's French retail banking business Lcl Le Crédit Lyonnais were expected to cost the bank around €150 million in 2022, Deputy CEO Jérôme Grivet said during a third-quarter earnings call. This figure would rise to €350 million in 2023 based on the expectation that the Livret A rate averages 3.5% over the course of the year.

The Livret A is the most popular of several regulated savings schemes operated in France. Others include the Livret de Développement Durable, used to finance environmentally sustainable projects, the Livret d'Epargne Populaire — set to rise to 6.1% from 4.6% as part of the government's recent decision — that offers attractive rates for savers on low incomes, and the Plan Epargne Logement for those saving to buy a house.

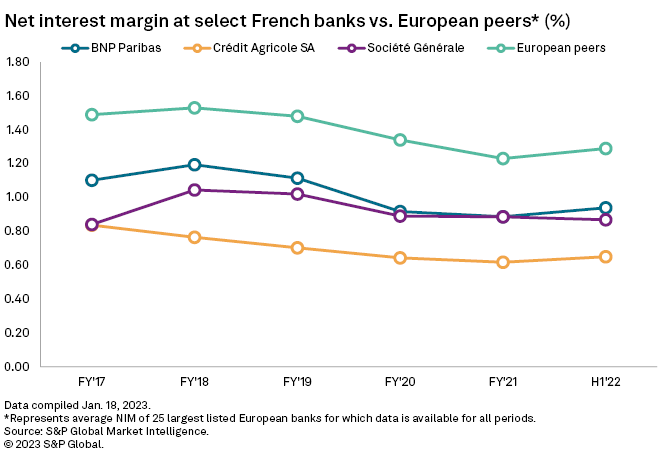

French banks' net interest margins — the difference between the interest income lenders' receive from borrowers and the interest they pay out to depositors — were already significantly lower than those of European peers before the Livret A began to rise last February. The average NIM of France's big three listed banks at the end of 2021 stood at 0.8% compared to an average of 1.23% for a sample of 25 of Europe's largest lenders, Market Intelligence data shows.

Other European lenders also received a bigger boost from rising rates in the first half of 2022 than the three French banks, the latest period for which NIM data is available for the Gallic institutions. NIM for the European lenders in the sample rose 6 basis points on average to 1.29% over the six months, compared to an average increase of just 2bps for France's three largest lenders.

"There has been already a repricing of deposits in France that has very much limited the NIM expansion," said Flora Bocahut, European bank equity analyst at Jefferies. "And the reason for that is the Livret A."

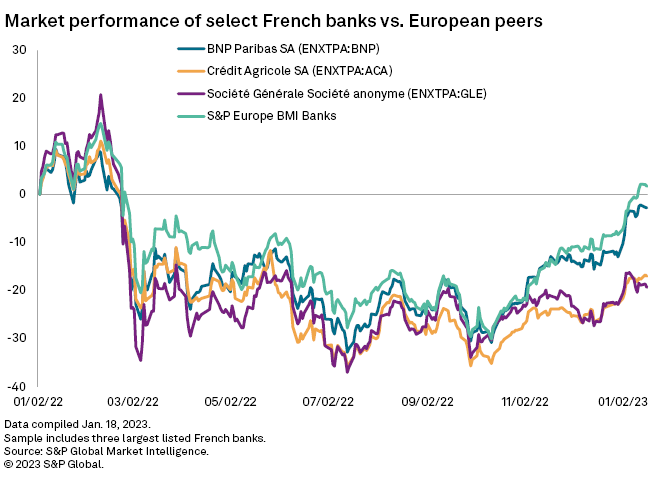

The negative impact of rising deposit costs on French banks' net interest income has weighed on their share prices. Since the first increase in the current Livret A cycle rate took effect Feb. 1, 2022, SocGen's share price has fallen almost 24%, CASA's almost 20% and BNP's just under 5%. This compares to a drop of just 0.3% for the S&P Europe BMI Banks Index, which captures the share price performance of the wider European banking sector.

Increases to the Livret A rate should slow in 2023. The formula for calculating the rate is partially based on inflation, which is expected to drop to around 4% in 2023, according to France's Ministry of the Economy and Finance. Inflation in France fell to 6.7% in December from 7.1% in November, data from country's statistics office showed.

Napoleonic debts

The Livret A was originally created by Louis XVIII in 1818 to repay debts from the Napoleonic Wars. The program is now used to finance social housing organizations and other public investments through France's state-owned investment group Caisse des Dépôts et Consignations.

Until 2009, France's publicly listed lenders were unable to offer Livret A accounts. All French banks are required to redirect 65% of their Livret A and Livret de Développement Durable deposit volume to CDC, which pays the banks a fee in return.

The Livret A and other regulated savings schemes' impact on French banks' profitability should not be the only consideration when assessing their value, said Sam Theodore, senior consultant at Scope Insights. The products also play an important role in the banks meeting their obligation to improving France's society and economy, Theodore said.

"If you look at everything purely from the margin perspective, then French banks are not really profitable when compared to the U.S. banks," added Theodore. "But then in the U.S., 24% of households are either unbanked or underbanked, while the French have 100% bank coverage."