8 Jun, 2021

BoE unveils climate change stress tests; results may affect supervision

By Jon Rees

The Bank of England has published details of its climate change stress tests and though the results will not be used to set capital requirements, they may affect the bank's supervisory approach.

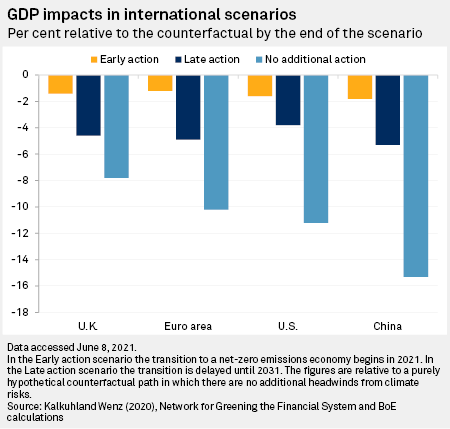

The BoE's Climate Biennial Exploratory Scenario uses three scenarios of early, late and no additional action to explore two key risks from climate change.

The first risk is that arising from the structural changes to the economy needed to meet net-zero carbon emissions and this is the transition risk. The second is the physical risk, which is the risk associated with higher global temperatures.

Assessing the scale of risk

The aim is to try to assess the size of the financial exposures to these risks of individual firms and the financial system, based on their 2020 balance sheets, to understand the challenges faced. The exercise is also intended to improve firms' risk management and banks will have to engage with their largest counterparties to understand their vulnerability to climate change.

The exercise will not be used to set capital requirements, and individual participants' projected losses will not be tied directly to actions participants are required to take, said the BoE.

Instead, the BoE said participants' submissions may inform its Financial Policy Committee's approach to systemwide policy issues and its Prudential Regulation Authority's approach to supervisory policy. It may also guide further work between participants and supervisors to address any issues highlighted, said the BoE.

Governor Andrew Bailey said the exercise would help it assess the risks from climate change for the biggest banks and insurers and the financial system as a whole.

"It's a novel exercise as firms will have to engage closely with their counterparties in order to get detailed data on those counterparties' exposures to these risks," he said.

|

"It will stretch the time horizon over which the banks and insurers assess these risks and it will require them to build up their own scenario analysis capabilities, helping them to understand better how they are exposed under different potential climate pathways. The end result will be more robust management of climate related financial risks across the sector."

Adapting business models

The tests will explore how companies intend to adapt their business models over time, in light of climate changes. The exercise also covers the management actions participants would anticipate taking in the published scenarios, as well as participants' present and future planned approaches to managing climate risk.

The three scenarios of early, late and no policy action are applied over a span from 2021 to 2050 to reflect the long-term nature of climate risks. There will be a qualitative questionnaire to capture banks' own views on their risks. The BoE will ask banks to use novel modeling to assess a detailed, bottom-up analysis of their largest counterparties. For the remainder of their counterparties, companies are expected to differentiate exposures by geography and sector.

For banks the exercise will focus on credit books, while for insurers the exercise will assess risks to both their assets and liabilities.

The BoE expects to publish results in May 2022.