25 Apr, 2022

Australian banks' return to bond market to raise costs, pressure margins

By Ranina Sanglap and Cheska Lozano

Australian banks face greater pressure on their margins in the coming years as they will need to replace about A$190 billion of central bank-subsidized funding with costlier money raised in the bond market.

The three-year Term Funding Facility, or TFF, provided by the Reserve Bank of Australia to help local banks with cheaper money to tide over the pandemic, will mature between March 2023 and June 2024. The banks will then need to rely more on bond markets after two years of relatively low debt issuance. With interest rates expected to rise, banks will need to pay more for fresh funding.

"I expect further margin compression, unless they can recover the costs from higher mortgage rates, which is what they are trying at the moment," said Martin North, principal at Digital Finance Analytics. The banks have to repay the TFF over the next couple of years, North noted.

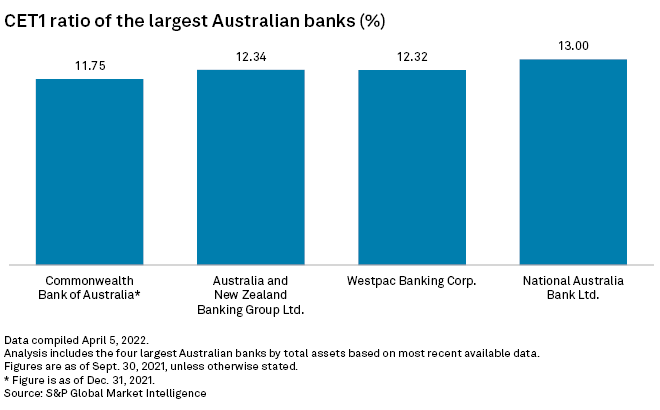

The TFF helped cushion some of the impact of the pandemic on banks' net interest margins, which have been on a downtrend for the major Australian lenders in recent years as the policy interest rate fell to a record low. For example, Commonwealth Bank of Australia, the country's largest bank by assets, saw its NIM drop to 2.03% in the fiscal year ended June 2021, from 2.15% three years prior.

Even when the benchmark cash rate starts to rise, banks may be unable to charge higher interest from customers as home buying has started to cool after property prices rose at a record pace in 2021.

Cheap funds

"Banks have been able to fund loan growth and replace maturing debt with customer deposits and the term funding facility in recent years," Nathan Zaia, an equity analyst at Morningstar, told S&P Global Market Intelligence. That may not change significantly in 2022, but "banks will likely be even more active from 2023 and into 2024 as they begin to refinance the term funding facility drawdowns," Zaia said.

Funds under the TFF were initially made available at a fixed rate of 0.25% when it was introduced in 2020. As the Reserve Bank of Australia, or RBA, cut the cash rate to 0.1% over the course of the pandemic to support the economy, the rate on TFF also was lowered in line with the benchmark. The TFF was closed to new drawdowns in June 2021.

Commonwealth Bank of Australia saw its debt market issuance drop to A$2.16 billion in 2021, from A$8.50 billion in 2019.

"Higher issuance costs may impact banks' funding costs over time as banks issue more new debt, to the extent that this issuance is more costly than maturing or existing funding," the RBA said in a March 17 report. In aggregate, banks' lending rates declined more than funding costs over 2021, in part due to competition in housing lending, as well as a shift to lower-margin products, it said.

The major banks did not issue new bonds, which account for the bulk of their wholesale funding, through the first quarter of 2021, the RBA said. However, as banks started to issue more bonds in the second half of 2021, their costs started to rise too.

The aggregate funding cost for Australian banks was already up by around 100 basis points as some lenders tapped bond markets in the second half of 2021, analysts said.

Normal levels

Australia and New Zealand Banking Group Ltd., or ANZ, the country's second largest bank by assets, expects financial institutions to return to more normal levels of debt market issuance in 2022. The bank expects the level of issuance from financial institutions to reach A$53 billion, from A$28 billion in 2021, ANZ's head of capital markets, Paul White told the Australian Financial Review.

ANZ's own debt issuance in 2020 stood at A$1.86 billion, down from A$5.06 billion in 2019. In 2021, the bank's debt issuance increased to A$2.22 billion.

Australian bonds will also be attractive to investors searching for capital stability as the commodities supplier nation's economy may accelerate in 2022.

"Australian bond yields will likely be the most sought and see a rise in demand as interest rates are rising for the first time in 14 years," said Jessica Amir, Australian market strategist at Saxo Markets. That would support yields as investors look for better returns, Amir told Market Intelligence.