30 Oct, 2023

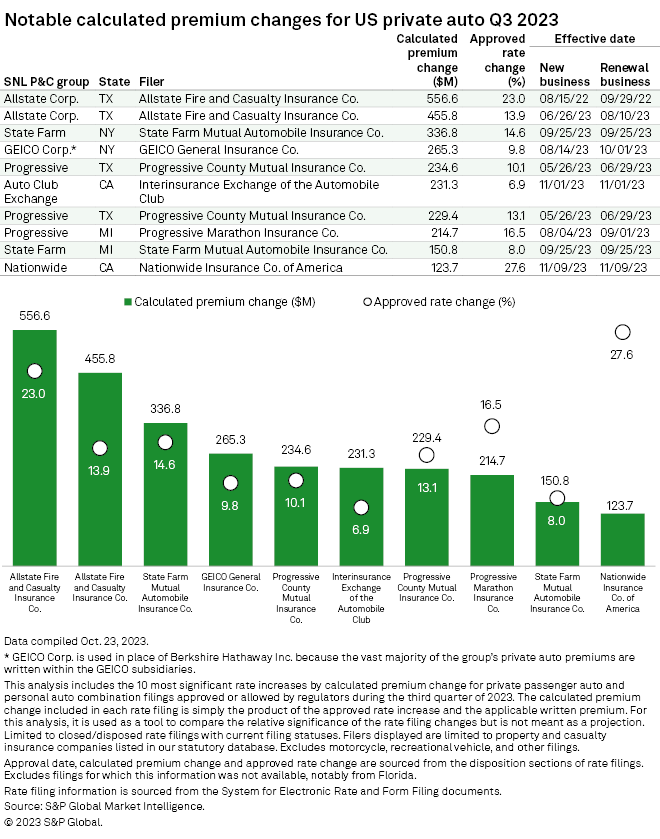

Allstate tops personal auto rate hike charts in Q3 2023

Subsidiaries of The Allstate Corp. secured approvals for several of the most-notable private auto insurance rate increases disposed during the third quarter, according to an S&P Global Market Intelligence analysis.

The two most significant rate hikes were granted to Allstate Fire & Casualty Insurance Co. in July and will impact policyholders in Texas. A 23.0% increase took effect Aug. 15, 2022, for new business and Sept. 29, 2022, for renewals. This summer the company sought to boost its rates again with a 13.9% increase that took effect June 26 for new business and Aug. 10 for renewals.

Regulators in the Lone Star State approved the largest number of rate hikes again during the third quarter, signing off on 125 increases, including 54 of more than 10%. Two other notable rate hikes in Texas were granted to Progressive County Mutual Insurance Co., a subsidiary of The Progressive Corp.

– Access the 2023 US Auto Insurance Market Report.

– Read insights about the US private auto market.

GEICO gets big hikes in Washington, Nevada

Multiple private auto carriers received rate increases in excess of 20% on books of business worth $20 million or more. Berkshire Hathaway Inc.'s Geico Corp. received such approvals in 11 instances. The bulk of these filings were in Washington and Nevada, with four rate changes in excess of 30%. The calculated premium change listed for the approved filings in the Evergreen State and the Silver State comes to aggregate totals of roughly $200 million and $176 million, respectively.

In California, Allstate subsidiary Integon Preferred Insurance Co. was approved for a 33.2% rate increase for its Cornerstone program. The new rate took effect Sept. 20 for renewal business and it will start to impact new business Nov. 21.

All figures in this analysis are based on as-reported numbers filed in the rate filings of each subsidiary in each state. The calculated premium change is not a final projection of the additional premium the insurer may receive in the upcoming year. The calculated premium change is reported by each insurer to reflect the most impactful premium changes based on the combined impact of the percentage change and the amount of business it affects. Changes to the insurer's policy mix or policies in force are not factored into the analysis.

US states employ a variety of rate regulation mechanisms, including prior approval, modified prior approval, file and use as well as use and file. Some states do not require explicit regulatory approval prior to insurers using new rates. This analysis is based on when rate filings are "disposed" by state regulators and does not take into account when those new rates became effective for new and renewal business. In some instances, a new rate may have been in effect prior to the month the filing was approved by the regulator.