Blog — 28 Sep, 2022

Worldwide smartphone shipment forecast through 2026: from small drop to mild recovery

By Milan Ringol

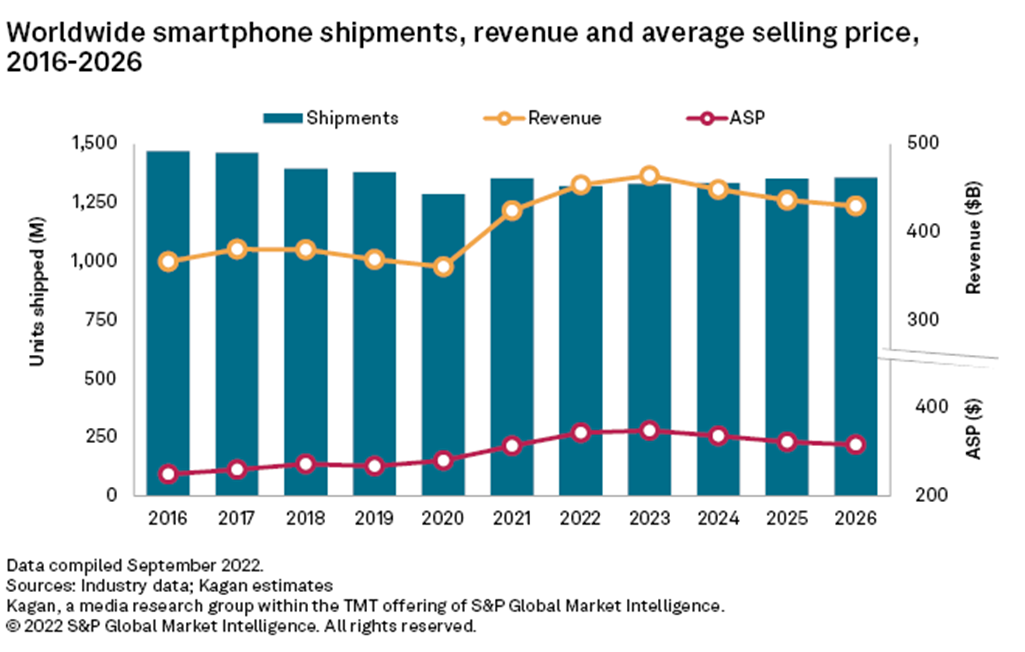

After a recovering in 2021 from a string of flat to down years that culminated with a near 7% drop in 2020, worldwide smartphone shipments are expected to decline by 2.4% in 2022 as inflation, component shortages and lengthening replacement cycles drive down demand for smartphones in the near term.

Beyond that, shipments are forecast to gradually recover as component shortages improve, supply chain disruptions decrease, and device adoption grows in underpenetrated markets.

However, Kagan expects these dynamics to allow the market only a modest improvement over 2021’s 1.35 billion units, growing annual shipments at a compound annual growth rate of less than 1% through 2026 to 1.36 billion units.

Key factors expected to impact the smartphone market in the coming years include:

- Many markets have reached, or are approaching, smartphone saturation with penetration rates above 80%. With fewer first-time buyers, smartphone shipments are driven primarily by replacement cycles that are gradually growing longer, resulting in declining shipments per year.

- The global semiconductor shortage is gradually easing as the demand curve settles closer to the available supply. A number of smartphone manufacturers noted year-over-year improvements to the situation as of the first half of 2022 but nonetheless still feel an impact on operations.

- China's strict institutional measures to curb sporadic COVID-19 outbreaks continue to impact global supply chains that rely on the country's manufacturing prowess. Aside from direct factory shutdowns, some land routes have been disrupted while a number of seaports remain severely congested as effects of city-wide lockdowns ripple out.

- Geopolitical tensions in the European subcontinent exacerbate the severe inflation in the current macroeconomic environment. Many markets around the world are falling into, if not already in, a recession and the prices of consumer goods are steadily rising. In such a situation, many consumers are thinking twice before buying a shiny new gadget.

- The strong marketing push for 5G networks and new 5G-ready devices is helping drive some upgrade purchases. Meanwhile, the gradual shutdown of legacy 2G and 3G networks in various markets worldwide are expected to drive some holdouts into finally upgrading to a smartphone.

Kagan's global smartphone forecast is built upon analysis of publicly available industry reports and proprietary data models. The report provides estimates on shipments, revenue, average selling prices as well as market share estimates.