Blog — 24 Jun, 2022

Inflation cools Q122 smart TV demand but revenue grows 10 percent YoY on higher ASPs

By Milan Ringol

Overview

After a surge that began in the second half of 2020 and ran through the first quarter of 2021, overall demand for smart TVs cooled down to pre-pandemic levels leading to an estimated 9.2% year-over-year decline in total smart TV shipments in the first quarter of 2022, according to Kagan estimates.

At the same time, a shift in product mix – with most vendors increasing the proportion of high-margin premium products in response to component shortages – raised the average selling price, or ASP, by 21% year over year and to an estimated $496. The price jump also contributed to the shipment decline that nevertheless resulted in a 10% year-over-year growth in first quarter. Q1 2022 smart TV revenues are estimated at $16.63 billion.

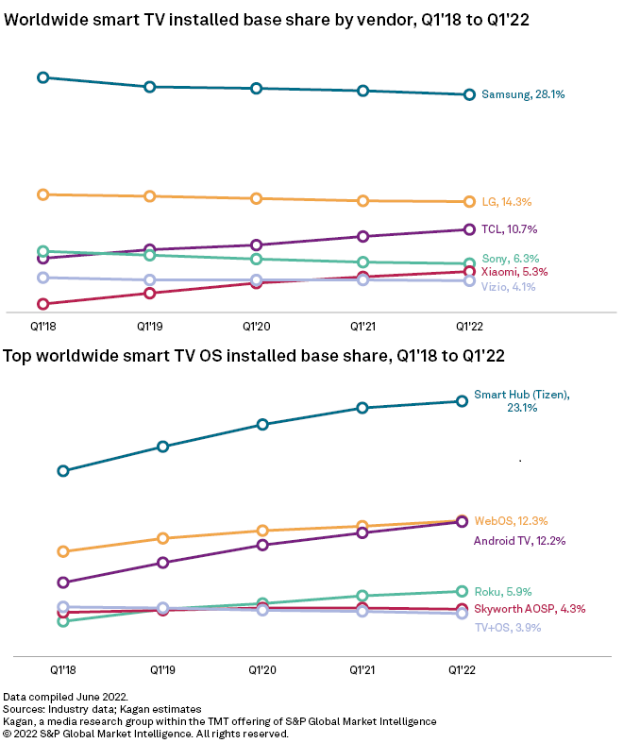

Smart TV Installed Base

In recent years, Samsung, LG and Sony, the leading smart TV brands since the early 2010s, have been slowly leaking installed base share to TCL and Xiaomi. Both Chinese companies are growing at least twice as fast as the more well-known Korean and Japanese brands with 19% and 27% respective year-on-year installed base growth in the first quarter of 2022. Competitively priced models from these rising stars have become attractive options compared to more traditional brands, as smart TV adoption gradually grows among emerging markets like India, Latin America, and the Asia Pacific.

With its head start in smart TV shipments and solid shipment volumes for the past seven years, Samsung's Tizen-based Smart Hub maintains the largest OS installed base worldwide with an estimated 23.1% share. Alphabet's Android TV is close to overtake LG's WebOS to be the second-largest smart TV platform by footprint. LG's move to license its OS to third-party manufacturers starting in 2021 may have been too little too late.

Kagan's quarterly global smart TV estimates of unit shipments, revenue, average selling prices, and installed base with vendor and OS breakouts are built upon analysis of publicly available industry reports and proprietary data models. Note that this analysis only includes TV sets used for home entertainment, excluding commercial sets used, for instance, in the hospitality industry and in public spaces and offices. Revenue estimates include only unit sales and not revenue generated from smart TV usage through ads, platform fees, or the like.