ECONOMICS COMMENTARY — Jun 13, 2025

Week Ahead Economic Preview: Week of 16 June 2025

By Chris Williamson and Jingyi Pan

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Fed FOMC, BoE, BoJ meetings and mainland China data in focus

Central bank meetings will be in abundance in the coming week, including in the US, UK and Japan, while inflation figures in the UK and Japan will be scrutinized alongside activity data from both the US and mainland China.

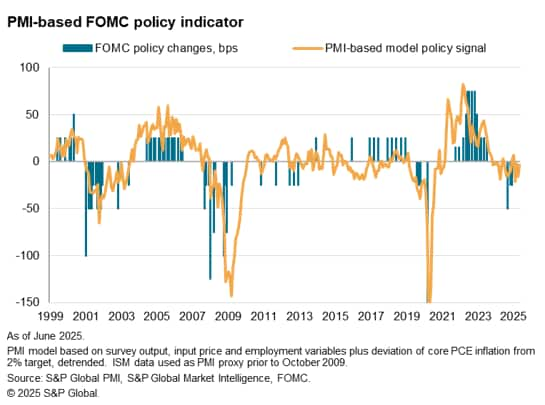

The Fed policymakers gather for the June FOMC meeting. Despite additional political pressure by President Donald Trump to lower rates and a lower-than-anticipated CPI report, US central bankers are widely expected to keep Fed fund rates unchanged in the near-term. Inflation remains above target at 2.4% and uncertainty about the potential impact of tariffs on prices remains a major concern at the Fed, all while the labour market continues to show encouraging resilience. The next move by the Fed nonetheless likely remains a cut, with money managers widely expecting up to 50 basis points of cuts in the second half of 2025, according to the latest June S&P Global Investment Manager Index (IMI). While the IMI survey has also indicated that the political environment remains the biggest drag on equities in the near-term, fiscal and monetary policy are acting as additional drags. As such, the Fed's stance will be closely watched for insights into the interest rate outlook and what may be a trigger for rate cuts.

A clearer bias towards the lowering of interest rates is meanwhile observed for the UK. Subdued growth conditions and softening inflationary pressures, according to May's UK PMI data, point to further rate cuts by the Bank of England, though it may not be until August when we see them move again, after having just lowered the Bank Rate by 25 basis points to 4.25% in May. The August cut is also likely to be followed by a further cut in November.

Meanwhile in APAC, the Bank of Japan faces greater challenges in their rate hike resolve amid signs of deteriorating economic trends. A near-stalling of growth has been signalled in May as US trade policy uncertainty dampened global trade. The impact was not limited to Japan, however, as APAC economies broadly experienced a slowdown in growth as export orders fell at an increased rate, according to PMI indications. To gain further insights into the impact of trade disruptions, mainland China's industrial production and retail sales figures will be in focus, while Japan also refreshes trade and inflation numbers for May.

PMI-based central bank indicators point to a further rate cuts in the UK while the bias is becoming less clear in the US, albeit temporarily as an inventory build-up buoy growth.

Key diary events

Monday 16 Jun

South Africa Market Holiday

China (Mainland) House Price Index (May)

China (Mainland) Industrial Production, Retail Sales, Fixed Asset Investment, Unemployment Rate (May)

China (Mainland) New Yuan Loans, M2, Loan Growth (May)

India WPI (May)

Eurozone Balance of Trade (Apr)

Canada Housing Starts (May)

United States NY Empire State Manufacturing Index (Jun)

Tuesday 17 Jun

Singapore Non-oil Domestic Exports (May)

Japan BoJ Interest Rate Decision

France IEA Oil Market Report

Eurozone ZEW Economic Sentiment Index (Jun)

Germany ZEW Economic Sentiment Index (Jun)

United States Retail Sales and Industrial Production (May)

United States Export and Import Prices (May)

United States Business Inventories (Apr)

United States NAHB Housing Market Index (Jun)

Wednesday 18 Jun

Japan Balance of Trade (May)

Japan Machinery Orders (Apr)

United Kingdom Inflation (May)

Indonesia BI Interest Rate Decision

Sweden Riksbank Rate Decision

South Africa Inflation (May)

Eurozone Inflation (May, final)

United Staes Building Permits and Housing Starts (May)

United States Fed FOMC Interest Rate Decision

Brazil BCB Interest Rate Decision

Thursday 19 Jun

Brazil, Poland, United States Market Holiday

New Zealand GDP (Q1)

Australia Employment Change (May)

Australia Unemployment Rate (May)

Philippines BSP Interest Rate Decision

Switzerland SNB Interest Rate Decision

Norway Norges Bank Interest Rate Decision

Taiwan CBC Interest Rate Decision

Türkiye TCMB Interest Rate Decision

United Kingdom BoE Interest Rate Decision

Friday 20 Jun

New Zealand, Sweden Market Holiday

Japan Inflation (May)

Japan BoJ Meeting Minutes

China (Mainland) Loan Prime Rate (Jun)

Malaysia Trade (May)

Germany PPI (May)

United Kingdom Retail Sales (May)

Taiwan Export Orders (May)

Canada Retail Sales (Apr)

Canada New Housing Price Index (May)

United States Philadelphia Fed Manufacturing Index (Jun)

Eurozone Consumer Confidence (Jun, flash)

* Access press releases of indices produced by S&P Global and relevant sponsors here.

What to watch in the coming week

Americas: Fed meeting, US retail sales, industrial production, building permits and housing starts data; BCB meeting; Canada retail sales

June's Federal Open Market Committee (FOMC) meeting unfolds midweek with the consensus pointing to no change in Fed rates at the mid-year meeting. According to the CME FedWatch tool, the market has priced in the next rate cut only towards the end of the year. Concerns over intensifying tariff-related inflationary pressures, coupled with a resilient labour market, as shown by the latest May S&P Global US PMI data and confirmed by the official labour market update, mean a rate cut only looks likely later in the year.

On the data front, US retail sales and industrial production figures will be key indicators to monitor, in addition to housing market updates. A solid rise in services activity contrasted with falling manufacturing production in May, according to PMI indications, and points to the likelihood of positive retail sales performance.

Central bankers similarly gather in Brazil to update monetary policy settings, with another hike not ruled out at present amid elevated inflation. That said, subdued growth conditions in May, according to the S&P Global Brazil PMI, add to the uncertainty for the interest rate outlook.

EMEA: BoE meeting, UK inflation, retail sales; Germany ZEW index; Eurozone trade data

Central bank meetings unfold in the UK, Switzerland, Norway and Sweden in the week ahead. While the Bank of England is expected to keep rates on hold according to consensus, the bias remains towards lowering rates on the back of subdued growth conditions and softening inflationary pressures, as seen via May's UK PMI update. Official UK inflation numbers will be due on Wednesday for an assessment of the latest CPI trend.

APAC: BoJ meeting, Japan inflation and trade data; mainland China activity data; Australia employment data; New Zealand GDP; BI, BSP, CBC meetings

A major central bank meeting also takes place in Japan, albeit with the Bank of Japan expected to hold its policy stance until later in the year. Key economic release includes Japan's inflation and trade, while a slew of activity figures will also be out from mainland China. Amid more subdued manufacturing sector conditions signalled by the Caixin PMI data, the industrial production numbers will be watched, while accelerating services activity growth hint at improvements for retail sales.

Australia meanwhile updates employment numbers and New Zealand releases first quarter GDP. Central bank meetings also take place in Indonesia, Philippines and Taiwan.

© 2025, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location

Products & Offerings