Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Apr 18, 2019

Rebound hopes fade as flash Eurozone PMI signals slow start to second quarter

- Flash Eurozone PMI falls to 51.3 in April indicating weak start to second quarter

- Steep (albeit easing) decline in manufacturing accompanied by slower service sector expansion

- Job growth defies slowdown to gain momentum, but backlogs of work fall sharply

The eurozone economy started the second quarter on a disappointing footing, with the flash PMI falling below consensus expectations to one of the lowest levels since 2014.

The data add to worries that the economy has failed to rebound with any conviction from one-off factors that dampened activity late last year, and continues to show only very modest growth in the face of headwinds from slower global demand growth and subdued economic sentiment.

Slow start to second quarter

The IHS Markit Eurozone Composite PMI® fell from 51.6 in March to 51.3 in April, according to the ' flash' estimate. The April reading was the third lowest since November 2014, running only marginally above the recent lows seen in December and January.

At this level, the PMI indicates that quarterly eurozone GDP growth has slowed to just under 0.2%. A similar 0.2% rate of expansion is being signalled for Germany, where the composite PMI ticked higher to 52.1, but France stagnated as the PMI merely edged up to 50.0 and the rest of the region moved closer to stalling, the rate of output growth sinking to the lowest since November 2013.

German firms reported that a declining car industry, strong competition across Europe and generally subdued global demand continued to dampen business growth.

Similarly, in France, although the stabilisation of output in April is further evidence of the dwindling economic impact of the 'gilets jaunes' demonstrations (protestor numbers have fallen to approximately 10% of their peak and the remaining disruption has been limited), companies reported a persistent underlying slowdown in demand.

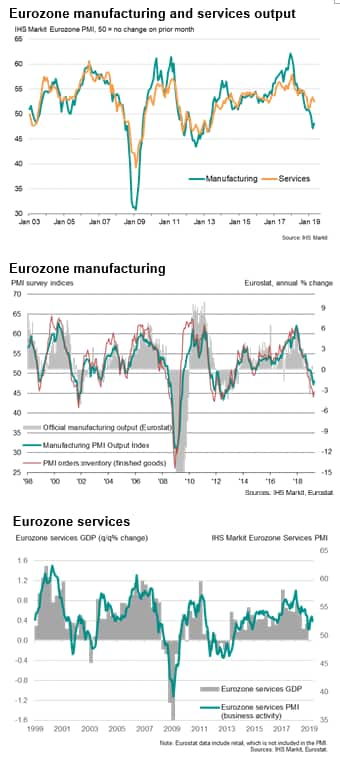

Steep manufacturing downturn persists

Manufacturing remained the key area of concern, with output continuing to contract at one of the fastest rates seen over the past six years. Forward-looking indicators such as the orders-to-inventory ratio and the gap between output growth and new order inflows collectively showed some signs of improvement, but all remain deeply in negative territory to suggest the factory malaise has further to run. The backlogs of work index meanwhile showed the largest drop in work in hand since November 2012, highlighting the paucity of fresh order inflows.

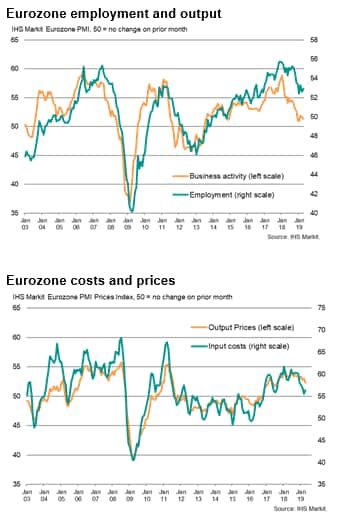

The slowdown also showed further signs of engulfing the service sector, where growth cooled again to one of the weakest seen since 2016. Some encouragement can be gleaned from an improvement in employment growth, although even here the pace of hiring is among the lowest seen for three years. Firms often remained reluctant to take on additional staff in the face of weak demand and an uncertain outlook.

Darkest outlook for five years

Business expectations about the year ahead continued to run at one of the gloomiest levels since late-2014, dipping for a second successive month in April to the lowest since January.

Reduced optimism was often linked to the recent slowing in demand and sales enquiries, as well as downgraded forecasts for economic growth. Specific concerns focused on rising political uncertainty, including Brexit, trade wars and protectionism. The weakness of the auto sector was once again often cited as a key area of concern.

Although input cost inflation across the euro area accelerated for the first time in seven months from March's two-and-a-half year low, in part driven by higher oil prices, average prices charged for goods and services rose at the slowest rate for 20 months as weak demand often stifled firms' pricing power.

Forecast revisions?

The persistence of the business survey weakness into the second quarter raises questions over the economy's ability to grow by more than 1% in 2019.

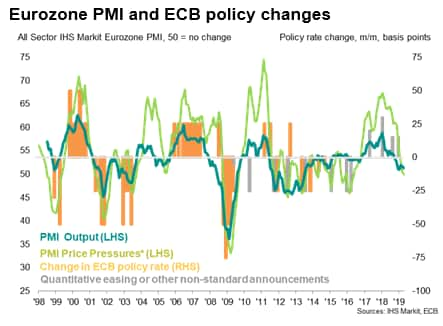

The data will therefore add to speculation that the ECB will need to take further steps to shore-up the eurozone economy in coming months, with the central bank having already made an about-face from its hawkish stance adopted throughout much of 2018.

Chris Williamson, Chief Business Economist, IHS Markit

Tel: +44 207 260 2329

chris.williamson@ihsmarkit.com

© 2019, IHS Markit Inc. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frebound-hopes-fade-as-flash-eurozone-pmi-signals-slow-start-to-second-quarter.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frebound-hopes-fade-as-flash-eurozone-pmi-signals-slow-start-to-second-quarter.html&text=Rebound+hopes+fade+as+flash+Eurozone+PMI+signals+slow+start+to+second+quarter+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frebound-hopes-fade-as-flash-eurozone-pmi-signals-slow-start-to-second-quarter.html","enabled":true},{"name":"email","url":"?subject=Rebound hopes fade as flash Eurozone PMI signals slow start to second quarter | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frebound-hopes-fade-as-flash-eurozone-pmi-signals-slow-start-to-second-quarter.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Rebound+hopes+fade+as+flash+Eurozone+PMI+signals+slow+start+to+second+quarter+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frebound-hopes-fade-as-flash-eurozone-pmi-signals-slow-start-to-second-quarter.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}