Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Jul 06, 2020

Momentum in Asia fights off a second wave of value in Europe and the US

Research Signals - June 2020

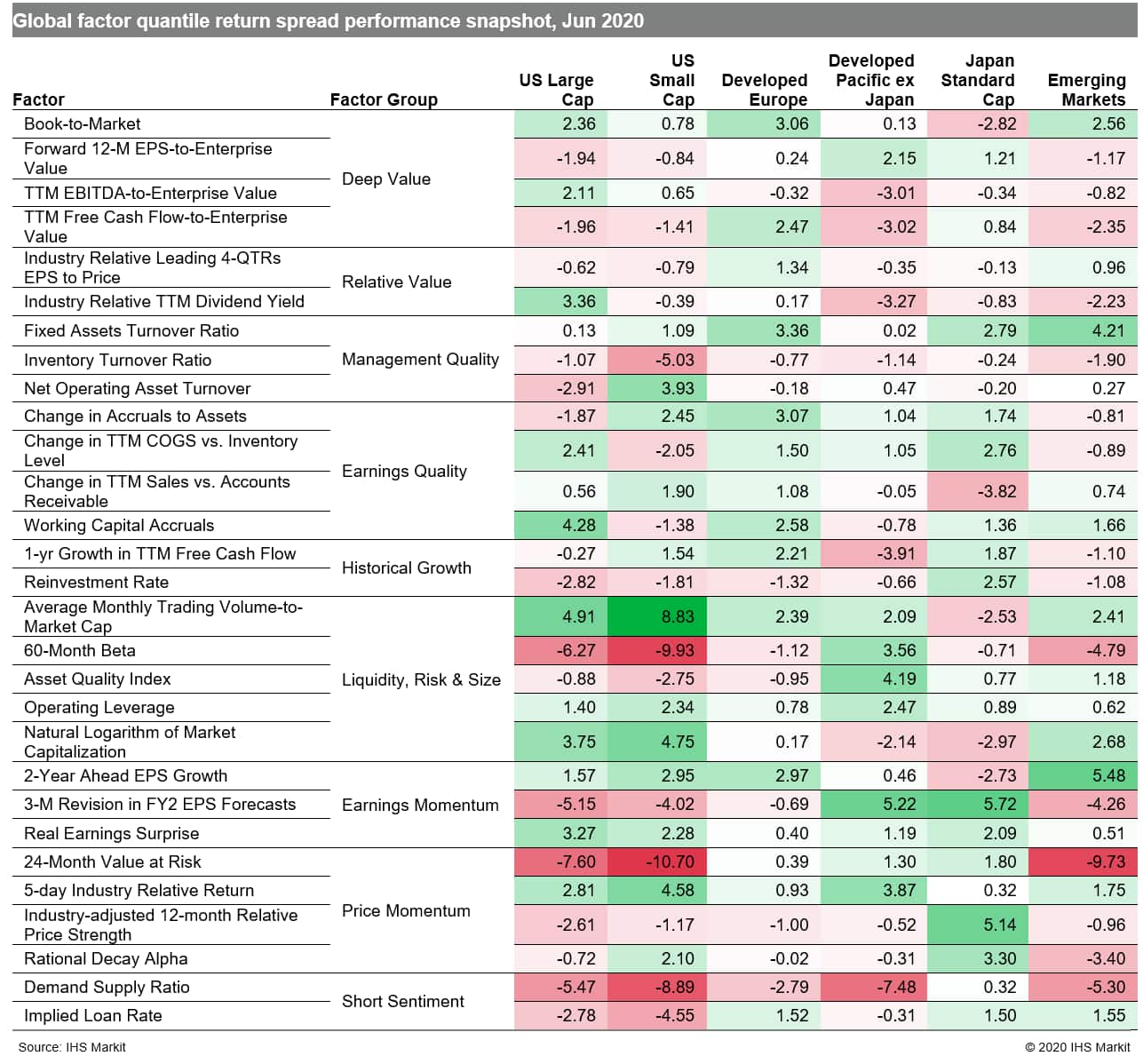

Several regional equity benchmarks posted their best quarter in years on optimism that their economies are recovering from coronavirus shutdowns as restrictions are eased, while weighing the risk of a second wave in COVID-19 cases. The J.P.Morgan Global Manufacturing PMI provided one such positive economic data point, signaling that the global manufacturing sector downturn eased sharply in June after starting on the recovery path in May. However, while increased risk taking was evident from factor performance across many regional universes, varying degrees of investor positioning were found, with momentum factors outperforming in developed Asia markets, whereas value prevailed in Europe and the US (Table 1).

- US: Increased risk taking was evidenced by underperformance to measures such as 60-Month Beta and 24-Month Value at Risk

- Developed Europe: Book-to-Market rebounded with an 11-percentage point increase in month-on-month spread performance

- Developed Pacific: Industry-adjusted 12-month Relative Price Strength returned to its winning ways in Japan after a one-month respite

- Emerging markets: 24-Month Value at Risk captured a robust aversion to low risk names, while undervalued names were favored based on Book-to-Market performance

Table 1

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmomentum-in-asia-fights-off-a-second-wave-of-value-in-europe-and-us.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmomentum-in-asia-fights-off-a-second-wave-of-value-in-europe-and-us.html&text=Momentum+in+Asia+fights+off+a+second+wave+of+value+in+Europe+and+the+US+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmomentum-in-asia-fights-off-a-second-wave-of-value-in-europe-and-us.html","enabled":true},{"name":"email","url":"?subject=Momentum in Asia fights off a second wave of value in Europe and the US | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmomentum-in-asia-fights-off-a-second-wave-of-value-in-europe-and-us.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Momentum+in+Asia+fights+off+a+second+wave+of+value+in+Europe+and+the+US+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fmomentum-in-asia-fights-off-a-second-wave-of-value-in-europe-and-us.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}