Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 12, 2020

Daily Global Market Summary - 12 August 2020

European and US equity markets closed higher on the day, while APAC markets were mixed. The S&P 500 came very close to a new record high, while US and European governments bonds posted a second consecutive day of significant selling. iTraxx/CDX credit indices tightened across IG/high yield and oil was sharply higher on the day, while gold recovered slightly after yesterday's sharp sell-off.

Americas

- US equity markets closed higher on the day and near the highest levels of the day; Nasdaq +2.1%, S&P 500 +1.4%, DJIA +1.1%, and Russell 2000 +0.5%. The S&P 500 closed at 3,380, which is only 0.4% away from the all-time intraday high level of 3,393 on 19 February.

- 10yr US govt bonds closed +4bps/0.68% yield and 30yr bonds closed +5bps/1.38% yield. 10s are now +18bps from this month's low yield of 0.50% on 4 Aug.

- CDX-NAIG closed -2bps/65bps and CDX-NAHY -9bps/390bps.

- Crude oil closed +2.5%/$42.67 per barrel.

- Gold closed +0.1%/$1,949 per ounce.

- As the earnings season draws to a close, companies within the Russell 2000 stock index — the small-cap benchmark — have reported an aggregate loss of $1.1 billion, compared to profits of almost $18 billion a year earlier, according to data provider FactSet. Meantime, the much bigger companies within the benchmark S&P 500 index have posted a 34% aggregate drop in earnings, to $233 billion. (FT)

- The US consumer price index (CPI) jumped 0.6% in July, matching

June's increase. Energy prices rose by 2.5% as gasoline prices

continued to rebound. The food CPI declined 0.4%. The core CPI rose

0.6%, the largest one-month increase since January 1991. (IHS

Markit Economists Ken Matheny and Juan Turcios)

- Consumer prices have risen sharply over the last two months, partially reversing declines from March through May. Recent increases leave the levels of the headline and core CPIs below their pre-COVID trends, as consumer price inflation remains muted.

- The core CPI rose 0.9% over June and July following a 0.6% decline over the prior three months. Gasoline prices rose 18.6% over the last two months, reversing about two-fifths of a 31.5% decline over the prior three months. In contrast, the CPI for food fell in July, the first decline following large increases during April, May, and June that totaled 2.8%.

- Twelve-month inflation rates remain low. The 12-month change in the overall CPI rose 0.4 percentage point to 1.0% in July. The 12-month change in the core CPI also rose 0.4 percentage point, to 1.6%. Twelve-month rates of change for both headline and core CPI remain below their pre-pandemic (February 2020) readings of 2.3% and 2.4%, respectively.

- The Securities Industry and Financial Markets Association

(SIFMA) has published US equity and debt issuance figures for July

2020. (IHS Markit Economist Brian Lawson)

- Primary equity sales of common stock fell to USD18.3 billion in July, versus USD67.5 billion and USD58.1 billion in the two preceding months.

- The July issuance level was slightly below that for July 2019 (USD18.5 billion), in stark contrast with the two preceding months when sales were roughly double those for the corresponding months in 2019.

- This activity had been heavily focused on capital increases, which totaled USD99.8 billion between May and June before declining to USD9.5 billion in July.

- In the fixed income markets, July corporate debt sales were US93.3 billion (versus USD117.7 billion in July 2019).

- This was well below the USD238.1 billion and USD301.1 billion of corporate debt sold in the two preceding months, with year-to-date (YTD) issuance standing at 1.526 trillion, 78.9% above the USD852 billion sold in the first seven months of 2019.

- Another notable growth segment is mortgage backed debt, where YTD issuance stands at USD1.826 trillion, versus USD998 billion between January and July 2019.

- By contrast, US Treasury issuance of USD1.98 trillion is 19.5% above the USD1.65 trillion sold in the first seven months of 2019.

- US electric vehicle (EV) specialist Lucid has announced that it has independent verification of its upcoming Air sedan reaching 517 miles on a single charge, based on US Environmental Protection Agency (EPA) testing protocol. According to a press statement from Lucid, FEV North America performed the testing, using the EPA's Multicycle Test Procedure (SAE J1634 Oct 2012 standard). Lucid says that FEV's results confirm that the sedan is the longest-range EV to date. Lucid also notes that FEV's test results are similar to what the startup automaker had found in its computer modelling. Lucid notes that its technology division, Atieva, played a "large" role in developing the battery pack, drawing on its experience of providing battery packs for Formula E racing. Rawlinson also noted that the 517-mile range was achieved even as the company reduced the battery pack's capacity, reducing vehicle weight and cost. Lucid also reconfirmed that the Air will be revealed fully on 9 September, including final interior and exterior designs, new details about product specifications, available configurations, and pricing. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Argentina recorded a drop in exports of soy and corn last month, according to the Rosario Stock Exchange (BCR). Soymeal exports declined by 22% to 2.4 million tons and soy by 23% to 1 million tons. Meanwhile, soy oil was the only commodity to perform positively, up 8% to 586,736 tons, it said. Between April and July, only soymeal exports decreased by 11% y-o-y, totaling 10.2 million tons. Despite the decline, the segment is still the main soy product exported by Argentina, while soy and soy oil increased to 5.2 million tons (+ 28%) and 2.4 million tons (+ 19%), respectively, it indicated. Meanwhile, corn shipments also fell in July by 5% y-o-y to 4.2 million tons, albeit smaller than soymeal and soy. Corn shipments, through ports based on Gran Rosario, dropped by 13% compared to the previous year. Gran Rosario which processed over 3 million tons in July, remains the main exporting route, BCR said. While corn shipments from Southern Santa Fe and Northern Buenos Aires grew sharply by 284% to 115,806 tons, the total volume is still small compared to other flow paths. Growth was owed to record low water levels of the Paraná river, preventing vessels to leave the Gran Rosario ports fully loaded, and complete shipments further South, it indicated. Gran Rosario was also the major road for soy and by-products exports which reached 3.4million tons in July, accounting for 84% of total oilseed shipped, while soymeal represented 70% share. Additionally, a total of 372,295 tons of wheat was exported via Gran Rosario in July down 15% y-o-y, where around 315,625 tons were shipped, it concluded. (IHS Markit Food and Agricultural Commodities' Ana Andrade)

Europe/Middle East/ Africa

- European equity closed higher across the region for the second consecutive day; UK +2.0%, Italy +1.1%, France/Germany +0.9%, and Spain +0.5%.

- 10yr European govt bonds closed lower again across the region; UK +4bps, Germany +3bps, and France/Italy/Spain +2bps.

- iTraxx-Europe closed -1bp/52bps and iTraxx-Xover -7bps/335bps.

- Brent crude closed +2.1%/$45.43 per barrel.

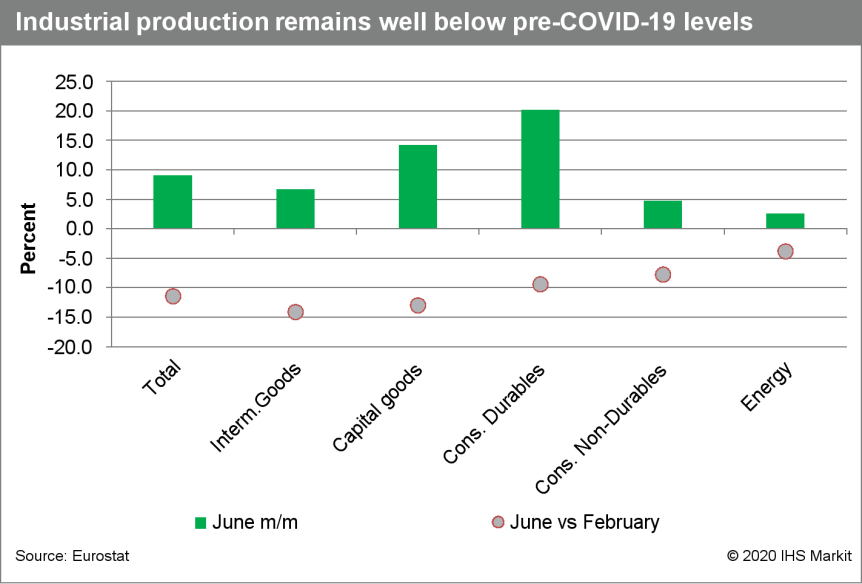

- The eurozone's industrial production rose by 9.1% month on

month (m/m) in June, below market consensus expectations (-10%

m/m), according to Reuters. Production is now estimated to have

increased by 12.3% m/m in May, slightly revised downwards from

12.4% m/m. (IHS Markit Economist Diego Iscaro)

- Given the substantial m/m declines in March and April, industrial production still collapsed by 16.0% quarter on quarter (q/q) during the second quarter, by far the largest quarterly contraction on record. Moreover, output was still 11.4% below where it was in February.

- June's increase was broad based across types of production, although production was particularly strong in the consumer durables (+20.2% m/m) and capital goods (+14.2% m/m) sectors. In May, production of intermediate goods grew below the average (+6.7% m/m).

- In all main sectors, production remained well below their pre-COVID-19 levels in February. Production of non-durable consumer goods was still 7.8% below February's level, while production of consumer durables stood 9.4% below where it was in February.

- Output of capital and intermediate goods performed even worse,

standing 13.0% and 14.1% below their pre-COVID-19 levels. On the

other hand, energy production was "only" 3.8% below February's

levels.

- The UK's Office for National Statistics (ONS) has reported that

the UK slipped into a short technical recession in the second

quarter, defined as two successive quarters of quarterly decline.

(IHS Markit Economist Raj Badiani)

- According to the ONS's first estimate, the economy shrunk by a record 20.4% quarter on quarter (q/q) in the second quarter after a 2.2% q/q drop in the first quarter.

- In addition, real GDP contracted by 21.7% year on year (y/y) in the second quarter, the biggest fall on record.

- This implies that the UK economy shrunk by a cumulative 22.1% in the first half of 2020, one of the most affected economies in the Organisation for Economic Co-operation and Development (OECD; see chart below).

- Consumer spending bore the brunt of tumbling activity during the second quarter, accounting for more than 70% of the fall of the expenditure measure of GDP. It fell for the second successive quarter after a 23.1% q/q decline in the second quarter, after rising uninterruptedly since the end of 2015. The fall in the first half of this year was because of falls in spending on tourism, restaurants and hotels, transport, and clothing and footwear.

- Other spending indicators confirm the dismal narrative. The volume of retail sales shrunk by 9.5% q/q in the second quarter, with declines across all store types except food stores and non-store retailing.

- Fixed capital formation fell for the third successive quarter, declining by 25.5% q/q in the second quarter. Business investment plunged, falling by a record 31.4% q/q, which is a staggering four times larger than the sharpest quarterly fall experienced during the 2008 global economic downturn.

- Service-sector output in the second quarter posted its sharpest quarterly fall on record, down by one-fifth compared with the first quarter.

- Construction output was the most affected by the COVID-19 virus lockdown, resulting in a very sharp drop in new work and repair and maintenance during April. The ONS reported that private new housing declined by 51.2% q/q, with social distancing measures halting housebuilding activity.

- The United Kingdom's national standards body, the British Standards Institution (BSI), has rolled out the first taxonomy for specifying the operational design domain (ODD) of an automated driving system (ADS). The new standard defines a common language for describing the ODD, including the type of road, traffic, and weather. The new standard, called "PAS 1883 Operational Design Domain (ODD) Taxonomy for Automated Driving Systems (ADS) - Specification", is the third publication from the CAV Standards Program. This program aims to fast-track the safe use of connected and autonomous vehicles (CAVs). Iain Forbes, head of the Centre for Connected and Autonomous Vehicles, said, "Connected and self-driving vehicle technology has the potential to level up transport across the nation by making every day journeys greener, safer, more flexible and more reliable. However, none of these benefits will be realized without public confidence that connected and self-driving technology is safe and secure. That is why BSI's CAV Standards Program is so important to the world-class work CCAV is leading on assurance, with PAS 1883 in particular supporting better communication and collaboration within the sector to enable even safer trialing and deployment of the technology." (IHS Markit Surabhi Automotive Mobility's Rajpal)

- According to all measures, the Swedish headline consumer price

inflation moderated in July. The consumer price index (CPI), which

is the national definition, came in at 0.0% year on year (y/y),

down from 0.7% in June. According to the EU-harmonised measure

(HICP), inflation was 0.7% y/y, down from 0.9% in June. (IHS Markit

Economist Daniel Kral)

- CPI at fixed interest rates (CPIF), which is the most closely watched indicator by the central bank, also moderated to 0.5% y/y in July, which is 0.5pp above the Riksbank's latest forecast from 1 July. CPIF excluding energy came in at 1.5% y/y, slightly higher than in June and also 0.2pp above the Riksbank's latest forecast.

- On an annual basis, electricity (-0.7pp), fuel (-0.3pp), and package holidays (-0.2pp) were the main drags on headline CPIF inflation. Food and non-alcoholic beverages, fruit, housing, and rents all contributed 0.2pp to headline inflation.

- On a monthly basis, CPIF rose by 0.2%. The main contribution to the monthly rate came from the price increases on rental cars, which added 0.2 pp to the rate, and higher prices for vegetables, which added 0.1 pp. These were offset by lower prices for electricity and dental care, both subtracting 0.2 pp from headline inflation.

- KINTO Share, a shared mobility program by Toyota, has selected Ridecell as the platform provider for its service in Stockholm (Sweden). KINTO Share offers vehicles for rental for any duration required; the vehicles must be picked up and returned to designated stations based in Stockholm. Ridecell will provide its high-yield mobility platform, which will enable users to have access to facilities such as customer verification, vehicle lock and unlock, service management, and yield monetization analytics. Ridecell is headquartered in San Francisco (United States) and has more than 170 employees in the US, Europe, Asia, and Australia. Ridecell's shared mobility platform will help KINTO Share users to get their fleet operational rapidly, as well as maximising efficiencies. Since March, Ridecell has added new customers including ZITY in Paris (France), GIG Car Share in Seattle (US), and now KINTO Share in Stockholm. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Kenya's parliament on 4 August reviewed amendments to section 157(9) of the Public Procurement and Assets Disposal Act 2015, which proposes increasing the required proportion of local suppliers used by firms that win government tenders from 40% to 60%. Moreover, government guidelines published this month stipulate that information and communications technology (ICT) companies must be at least 30% Kenyan owned to obtain an operating license. In response to increasing unemployment, caused in part by COVID-19 virus-related restrictions on businesses and movement, President Uhuru Kenyatta is also prioritizing policies to increase local employment. The fiscal year 2020/21 budget earmarked USD92 million for the "Kazi Mtaani" ("work on the street") scheme to provide extra jobs for more than 200,000 people in utilities, cleaning, and road maintenance. Having allied with the main opposition Orange Democratic Movement (ODM), Kenyatta has support from a majority of MPs and senators, likely ensuring that the amendment to increase the use of local suppliers in government tender works will be finalized and implemented. (IHS Markit Country Risk's William Farmer)

Asia-Pacific

- APAC equity markets closed mixed; Mainland China -0.6%, India/Australia -0.1%, Japan +0.4%, South Korea +0.6%, and Hong Kong +1.4%.

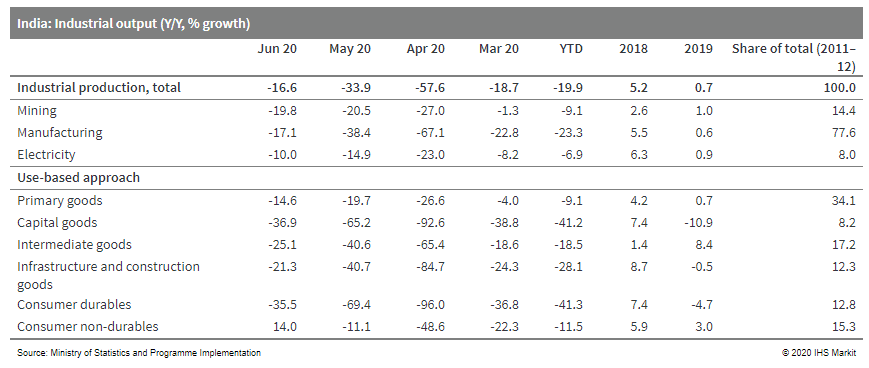

- Indian industrial production contracted by 16.6% year on year

(y/y) in June 2020. Despite the continued severe contraction, this

represented a significant improvement on the situation in May, when

industrial production fell by 33.9% y/y. (IHS Markit Economist

Rajiv Biswas)

- The easing of lockdown restrictions on the industrial sector in successive stages since 22 April has resulted in a significant rebound in industrial output during June.

- The overall contraction in industrial production for the April-June quarter was 35.9% y/y, owing to the severe lockdown in place during April, when production collapsed in many segments of manufacturing, such as auto manufacturing.

- Manufacturing output fell by 17.1% y/y in June. Although the extent of contraction remained deep, the June number reflected a significant rebound compared with the 40.7% y/y decline recorded for second-quarter 2020.

- Although most sectors of manufacturing continued to show y/y declines in output, the pharmaceuticals sector showed a strong rise, up 34.6% y/y owing to strong domestic and international demand for Indian pharmaceutical products, reflecting pandemic-related orders.

- The food manufacturing sector was also resilient, with output down just 2.6% y/y while output of chemical products was down just 1.9% y/y.

- Many key sectors of manufacturing remained very weak in June, with auto manufacturing output down 48% y/y, and manufacturing of computers, electronic, and optical products down 24.8% y/y.

- June data continued to show a considerable decline in output of capital goods, which fell by 36.9% y/y, while output of infrastructure/construction goods fell by 21.3% y/y, reflecting severe weakness in domestic investment due to the pandemic and recessionary conditions.

- Output of consumer non-durables showed strong positive growth of 14% y/y in June, as the easing of lockdown restrictions on consumers since early May helped to boost demand for essential goods.

- Demand for big ticket items remained weak, with output of consumer durable goods contracting by 35.5% y/y.

- The contraction in electricity production narrowed to a decline

of just 10% y/y in June, while mining output recorded a contraction

of 19.8% y/y.

- Indian pharmaceutical company Cipla has announced plans to scale-up manufacturing capacity for remdesivir amid rising demand for the drug to treat COVID-19. Cipla, along with Jubilant (India), Hetero (India), and the Indian subsidiary of Mylan (US), was one of the companies that originally signed a non-exclusive licensing agreement with Gilead (US) for bioequivalent versions of Veklury (remdesivir) for distribution in 127 low- and middle-income countries as a treatment for COVID-19 (see India: 13 May 2020: Gilead signs non-exclusive licensing deals for remdesivir with five generic companies in India and Pakistan). Dr Reddy's (India) later also agreed a non-exclusive licensing deal for remdesivir under the same terms. Local news source Live Mint now reports that Cipla is planning to start the manufacture of remdesivir at its plant in Goa. Cipla had earlier contracted production of the drug to Daman-based Sovereign Pharma, which had capacity to supply 50,000 to 95,000 vials per month. Cipla's chief financial officer Kedar Upadhye stated that, "Demand continues to outstrip supply significantly". However, Upadhye added that he expects the supply gap to narrow as more Indian companies launch their licensed generic versions of the medicine. (IHS Markit Life Sciences' Sacha Baggili)

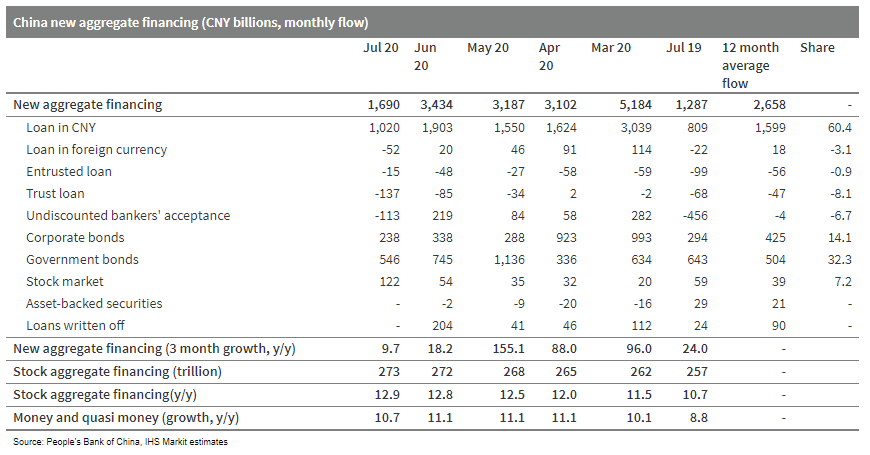

- China's new aggregate financing, the widest measure of net new

financing to the real economy, increased CNY1.7 trillion in July

2020, up CNY402.8 billion from a year ago while halving new

financing in the previous month, according to a release from the

People's Bank of China. The growth of stock TSF continued to rise

from 12.8% year on year in June to 12.9% y/y this month. (IHS

Markit Economist Yating Xu)

- Bank loans injected to the real economy increased CNY968 billion, up CNY181 billion from a year ago.

- New bank loans at CNY992.7 billion was lower than the level a year ago, the first year-on-year decline since the start of the pandemic, largely because of the decline in corporates' short-term borrowing, possibly reflecting the withdrawal of some temporary stimulus.

- Borrowing from households and long- and medium-term loans of corporates continued to rise, with sustained economic growth and financial support for major projects.

- Off-balance sheet financing, including entrusted loans, trust loans, and undiscounted bankers' acceptance declined by CNY88 billion in July, compared with a CNY622 billion reduction a year ago.

- Government bonds and corporate bonds issuance declined by CNY56.1 billion and CNY96.8 billion respectively from a year ago, which was the main contributor to the lower than expected new TSF in July.

- Broad money supply (M2) growth slowed to 10.7% year on year in

July from 11.1% year on year in the previous three months.

Households' deposits posted the largest reduction over the past

three years, corporates' deposits registered a record decline in

July, while deposits of non-banking deposit institutions rose

sharply at the same time, suggesting that the move of deposits from

banking system to stock market drove the index rally in July.

- Record flooding through June-July has mostly caused damages in

Mainland China's rural areas, therefore helping reduce direct

disruptions in industrial and services sector; potential

post-disaster reconstruction could generate growth tailwinds. (IHS

Markit Economists Yating Xu and Lei Yi)

- Direct economic losses from floods have totaled CNY149.05 billion through the end of July, according to the estimates by the Ministry of Emergency Management (MEM).

- Losses of CNY109.74 billion, or nearly 74% were incurred in July. Cumulatively, flood-incurred cost from 1 June (the start of main flooding season) to 22 July is down 5% compared with the 2015-19 average.

- Record-setting floods in July have impacted around 38.17 million people nationwide and displaced nearly 3 million, up by 62.5% and 88.6% compared with the average of same-period values in the past five years respectively. Nonetheless, such evacuation efforts have helped to reduce casualties by over 50% compared with past five-year average.

- Emergency response of flood control has been lowered from third to the lowest fourth level on 7 Aug, as flooding started to recede towards the end of July.

- Thanks to the nation's expanding economic scale and flood control efforts, direct economic cost of flood disasters as a share of GDP has been declining over the past years. Flood-incurred losses reached 3% of nominal GDP in 1998, 1% in 2010, and 0.5% in 2006. This year, direct economic cost through July approximates merely 0.15% of mainland China's nominal GDP in 2019.

- Tesla sold 11,041 vehicles in China during July, according to data from the China Passenger Car Association (CPCA). The data do not include a breakdown by individual model, but the majority of Tesla's July sales are likely to have come from the locally made Model 3. Tesla does not report sales results for individual markets as of this reporting. Tesla's July sales results indicate that demand for its electric vehicles (EVs) remains strong in the Chinese market. Compared with June, the automaker's deliveries fell by 26.2% in July from 14,954 to 11,041 units, but the US manufacturer still outsold an array of local rivals, including strong startup contestants, to become the top seller in the new-energy vehicle segment. In comparison, NIO delivered 3,533 vehicles in July, while Li Auto sold 2,516 vehicles during the month. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Hyundai Autoever, a subsidiary of Hyundai Motor Group, will build 5G-based vehicle-to-everything (V2X) infrastructure in the South Korean city Daegu. V2X technology enables vehicles to communicate directly with other vehicles, pedestrians, devices, and roadside infrastructure, and facilitates the operations of automated vehicles. This project is scheduled for completion at the beginning of next year. Yoo-seok, CEO of Hyundai Autoever, said, "Through experience in Cooperative Intelligent Transport Systems (C-ITS) projects such as building a self-driving test bed, K-City, and C-ITS on expressways, we intend to contribute to becoming a leading autonomous driving city in Daegu. As a provider of future transportation solutions based on autonomous vehicles, Hyundai Autoever is striving to complete the 'Autonomous Driving Support Convergence Technology Platform' in line with its business expansion". (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Kyanite Investment Holdings, Temasek's wholly owned subsidiary, has withdrawn its USD 3 billion (SGD 4.1 billion) bid for Keppel Corporation after invoking the material adverse change clause. This came after the USD 490 million (SGD 697 million) Q2 net loss reported by Keppel Corporation. The clause in Temasek's offer states that Keppel's net profit must not fall by more than 20%, or about USD 405 million (SGD 557 million), over the cumulative four quarters from the third quarter ended September 2019. The group's recent results have breached the precondition. This move may negatively influence the widely speculated merger between Keppel O&M and Sembcorp Marine. Back in June 2020, Temasek has backed a USD 1.5 billion (SGD 2.1 billion) rights issue by Sembcorp Marine and its demerging from Sembcorp Industries. (IHS Markit Upstream Costs and Technology's Jessica Goh)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-12-august-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-12-august-2020.html&text=Daily+Global+Market+Summary+-+12+August+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-12-august-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 12 August 2020 | S&P Global &body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-12-august-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+12+August+2020+%7c+S%26P+Global+ http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-12-august-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}