Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

CREDIT COMMENTARY

Jul 23, 2015

US IG CDS-bond basis review

The commodities slump in recent weeks has opened up several basis opportunities as cash bond spreads have not keep up with their CDS peers in the US investment grade space.

- 63 CDX NA IG constituents trade with a CDS-bond basis greater 50bps

- Positive basis trades have been driven by commodities slump over the last month

- Two of the names currently trading at a positive basis have limited supply of bonds to short

The CDS-Bond Basis captures the relative value between a cash bond and CDS contract of the same credit entity. Loosely defined, it is the bond's swap spread subtracted from its CDS spread.

CDS-bond basis = CDS spread - cash bond spread

Fluctuations in the basis give rise to arbitrage trading opportunities, since in theory the basis should be zero. Capturing a positive basis would involve selling the cash bond (pay spread) and concurrently selling protection (receive spread) on the same credit entity. Likewise a negative basis trade would involve buying the bond (receive spread) and concurrently buying protection (pay spread) on the same credit.

An analysis of the most liquid US investment grade 5 year CDSs which make up the 125 constituent of the Markit CDX NA IG and their corresponding reference bonds sees many such discrepancies which could be arbitraged away. This analysis is based on the actual CDS-bond basis (mid) as calculated by Markit's bond pricing service.

Using a 50bps threshold, there are currently four entities trading with a positive basis. The negative basis trade offers many more possibilities in the CDX NA IG, with 59 constituents of the index currently trading with a negative basis of greater the 50bps.

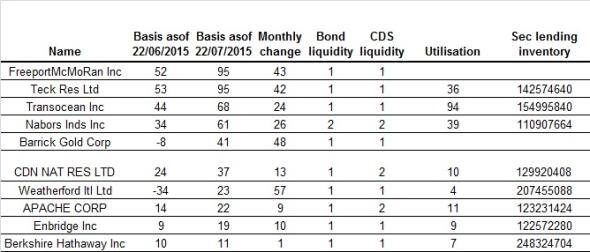

Positive basis

The positive basis universe is dominated by the commodity sector, which has seen the largest widening in basis over the last months. This phenomenon means that CDS traders have started to treat commodity names much more sceptically than their cash bond peers over the last month. This trend is no doubt driven by the recent slump in commodities prices, which has seen investors rush to buy protection, as well as prompting a slowdown in primary market bond issuance over the past few months; suppressing bond spreads

This trend has been seen in Freeport, which saw its CDS spread widen 161bps to 411bps over the past month. Its cash bond spread has also deteriorated in the last month, but to a lesser extent. This means that the basis trade is now 95bps, over twice the level seen a month ago. This gives Freeport the largest positive basis out of any index constituent.

Also near the top of the list is oil and gas producer Transocean and diversified mining firm Teck Res Ltd, with basis of 94bps and 67bps respectively. Both entities have a bond liquidity score of 1 and a CDS entity liquidity of 1; the highest possible grade.

But taking advantage of the trade would not be straightforward as it would involve shorting bonds in the cash market which would involve sourcing to borrow first. This would prove difficult for two of the four names currently trading with a positive basis. None of the reference Freeport five year bonds are currently in sitting in lending programs tracked by Markit Securities Finance, while over 90% of the $154m of Transocean five year bonds sitting in lending programs are currently out on loan.

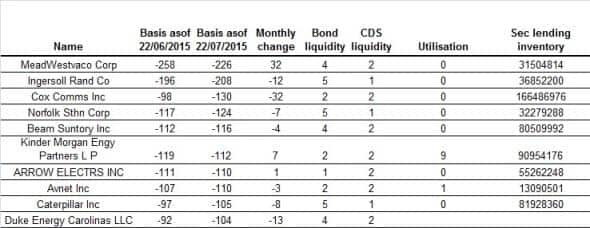

Negative basis

It comes as no surprise that most names in the list trade on a negative basis, as this follow the historic trend in the US over the past few years. This has been driven by the low interest rates seen in recent years, which has seen many reference bonds trade above par.

The above phenomenon throws off the basis trade as the seller of the CDS contract guarantees a par amount, usually 100, will settle for a lower spread in a case of default.

This is can be seen in MeadWestvaco Corp, the company with the widest basis, whose five year bond trades at 125 cents on the dollar.

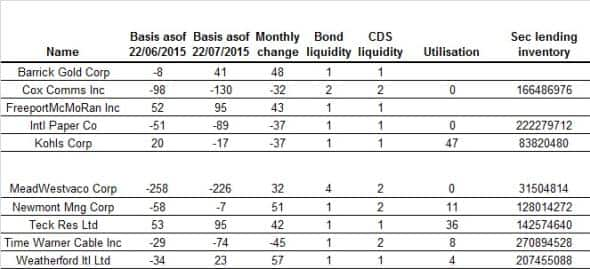

Biggest monthly movers

Neil Mehta | Analyst, Fixed Income, Markit

Tel: +44 207 260 2298

Neil.Mehta@markit.com

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23072015-credit-us-ig-cds-bond-basis-review.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23072015-credit-us-ig-cds-bond-basis-review.html&text=US+IG+CDS-bond+basis+review","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23072015-credit-us-ig-cds-bond-basis-review.html","enabled":true},{"name":"email","url":"?subject=US IG CDS-bond basis review&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23072015-credit-us-ig-cds-bond-basis-review.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=US+IG+CDS-bond+basis+review http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f23072015-credit-us-ig-cds-bond-basis-review.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}