Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jun 09, 2017

Eurozone GDP revised higher, in line with buoyant PMI

Are we there yet? The European Central Bank has been waiting for signs that the eurozone has reached 'escape velocity', whereby growth is strong enough to be self-sustaining without the help of so much monetary stimulus. The latest ECB meeting merely showed that 'forward guidance' had merely been tweaked modestly, reflecting a more balanced outlook in terms of risks. However, recent upward revisions to GDP and signs of a further broad-based acceleration in growth will add to speculation that risks will soon become skewed to the upside.

Furthermore, survey evidence of employment and capex growth strengthening further in the second quarter will add to the views that criteria of growth becoming self-sustaining are increasingly being met.

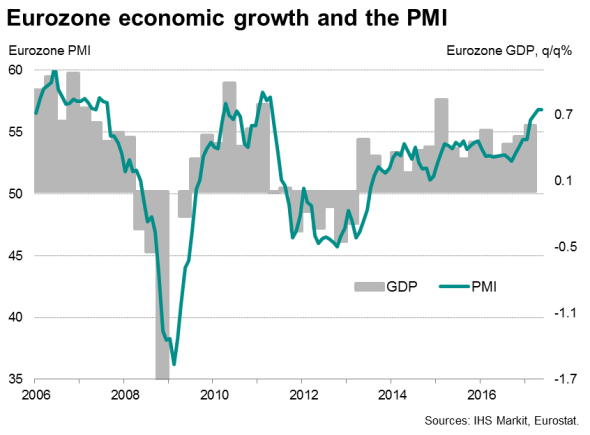

GDP revised higher, in line with PMI

Official data from Eurostat now show the eurozone economy growing 0.6% in the first quarter, up from a prior estimate of 0.5%. The faster growth is in line with the signals from the PMI surveys, which had been indicating a 0.6% expansion as far back as February*.

The first quarter expansion is no aberration. In fact, running at six-year highs, the PMI readings for April and May suggest that the rate of GDP growth will have picked up further in the second quarter, rising to 0.75%.

The upward revision to first quarter GDP mainly reflected faster growth in France and Italy, which brought previously-lacklustre performances more in line with the national PMI surveys. The revisions mean the official and survey data now indicate that the upturn became more evenly spread across the euro area's largest members, a trend that the PMI data indicate continued into the second quarter.

So far in the second quarter the PMI surveys are running at levels indicative of 0.7% GDP growth in France and Germany, with nearly 1% being signalled for Spain and 0.5% in Italy.

Rising capex

The revisions also mean the composition of eurozone GDP now aligns more closely with the PMI data. Notably, trade is now seen to be acting as less of a drag on the economy than previously thought, domestic demand is continuing to help drive growth and, perhaps most encouragingly, capital spending has picked up.

In the first quarter, exports grew by 1.2%, household spending was up 0.3% and gross fixed capital formation (capex) jumped 1.3%, building on a 3.4% surge in the fourth quarter of last year.

With the Eurozone Manufacturing PMI survey's new export orders index hitting six-year highs in recent months, the export upturn looks to have gained momentum in the second quarter. A ranking of PMI export orders shows euro member nations dominating globally, holding seven of the top eight places.

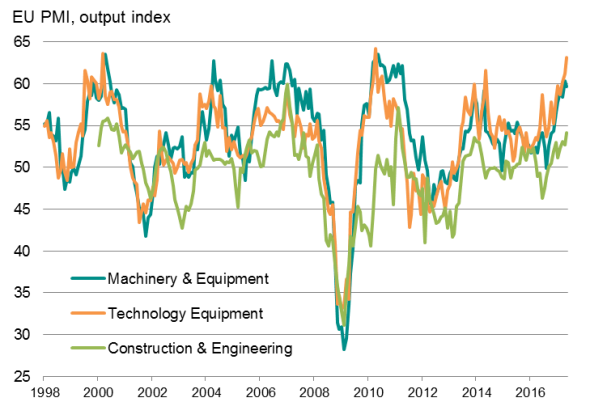

European PMI sector data meanwhile add to signs that business investment is rising strongly again in the second quarter. Output growth in capex bellwethers such as machinery & equipment, technology equipment and construction & engineering have all seen marked upturns in recent months, with growth accelerating especially sharply in the tech sector to a near-record pace in May. It was also the fastest growing sector covered by the PMI, with machinery & equipment manufacturing in third place.

European capex-related sectors

Investment accompanied by job gains

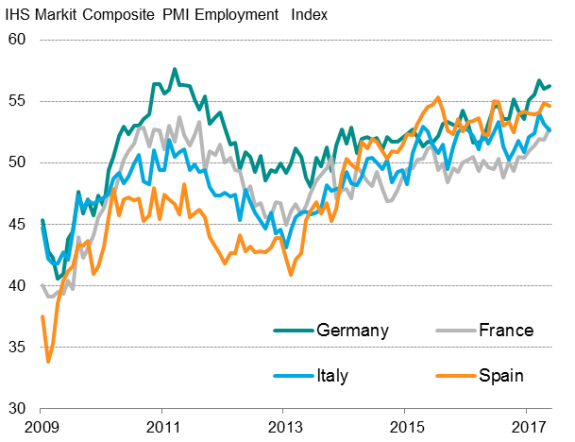

It is also encouraging to see that increased investment in capital equipment is not merely designed to replace labour. Instead, employment is rising sharply alongside the upturn in investment. Overall employment measured by the PMI is growing at one of the fastest rates seen over the past decade, with factory job growth hitting a two-decade high.

Jobs are also being created across all major euro member states, albeit led by Germany.

Strong jobs growth in all big-four euro nations

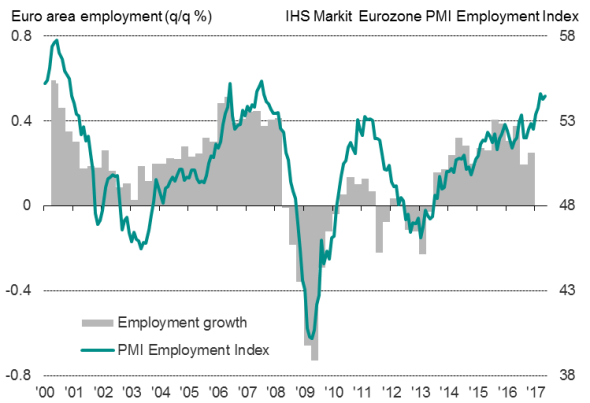

Eurozone labour market

Sources: IHS Markit, Eurostat.

Chris Williamson | Chief Business Economist, IHS Markit

Tel: +44 20 7260 2329

chris.williamson@ihsmarkit.com

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09062017-Economics-Eurozone-GDP-revised-higher-in-line-with-buoyant-PMI.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09062017-Economics-Eurozone-GDP-revised-higher-in-line-with-buoyant-PMI.html&text=Eurozone+GDP+revised+higher%2c+in+line+with+buoyant+PMI","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09062017-Economics-Eurozone-GDP-revised-higher-in-line-with-buoyant-PMI.html","enabled":true},{"name":"email","url":"?subject=Eurozone GDP revised higher, in line with buoyant PMI&body=http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09062017-Economics-Eurozone-GDP-revised-higher-in-line-with-buoyant-PMI.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Eurozone+GDP+revised+higher%2c+in+line+with+buoyant+PMI http%3a%2f%2fwww.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2f09062017-Economics-Eurozone-GDP-revised-higher-in-line-with-buoyant-PMI.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}