Blog — 16 May, 2023

US buyers are quietly coming back in Europe

By Iuri Struta

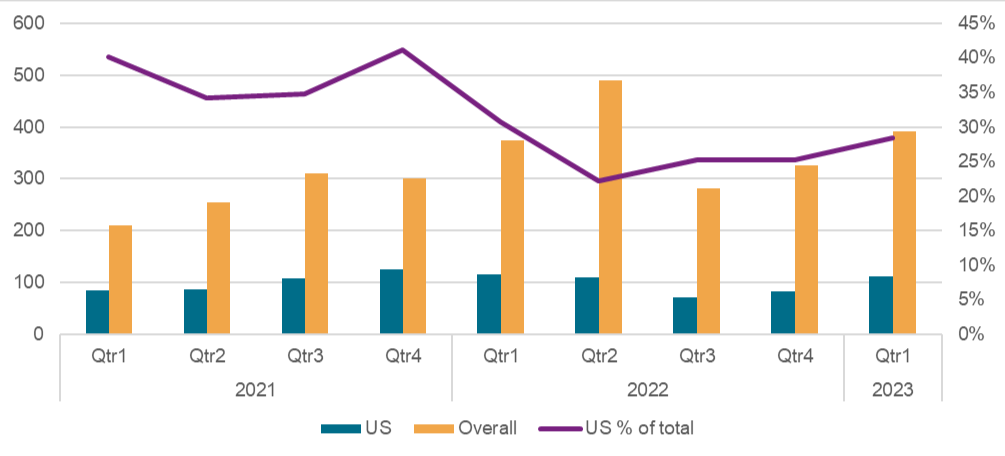

A defining feature of the European M&A market in 2022 was the exit of US buyers. At the market's peak in late 2021, American acquirers were responsible for nearly half of the consolidation activity across the pond. In the second quarter of 2022, that number fell to less than one-quarter and remained low throughout the year. This year, however, US buyers appear to be quietly returning.

Private equity firms have stepped up their M&A activity on European soil and are well on track to beat last year's deal flow. Only seven PE purchases are needed in Europe this year to equal 2022's tally, according to data from 451 Research's M&A KnowledgeBase.

In early March, Thoma Bravo made an investment in healthcare data analytics provider LOGEX International, marking its third ever direct investment in Western Europe (all others have been via portfolio companies).

Battery Ventures bought fleet management SaaS specialists Vimcar and Avrios International and combined them, after printing no transactions in 2022.

Marlin Equity Partners has already executed two buyouts this year in Europe, purchasing Google-focused cloud migration vendor Cloud Technology Solutions and environmental tech provider Tennaxia.

US strategic acquirers are also returning. In the first quarter of the year, strategics deployed more money into Europe than in any of the previous four quarters, according to the M&A KnowledgeBase. Zoom Video Communications Inc., Concentrix Corp. and Snap Inc. have been among those that have expanded in Europe this quarter. Of course, the size of the average deal remains low compared with 2021 standards.

One reason for the uptick in activity is that European companies have become cheaper. According to our data, targets in Western Europe this year are commanding a median valuation of 1.6 times revenue, compared with 2.2x last year. In many cases, this allows US buyers to beat out local competition for assets while still paying lower prices than at home, where the median multiple is 3.7x.

Figure 1: European acquisition activity by buyer (deal flow)

Source: 451 Research's M&A KnowledgeBase.

© 2023 S&P Global.

Location

Segment