ECONOMICS COMMENTARY — May 11, 2023

Taiwan economy slumps into recession

By Rajiv Biswas

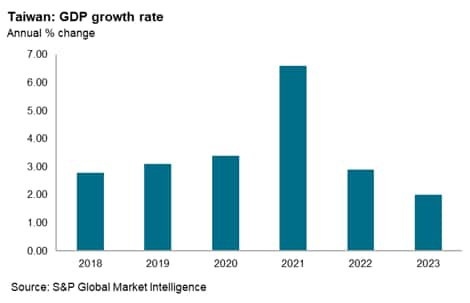

Taiwan's export-driven economy has been hit by slumping exports, resulting in GDP contracting by 3.0% year-on-year (y/y) in the first quarter of 2023, following negative growth in the fourth quarter of 2022. With two consecutive quarters of negative growth recorded, Taiwan's economy has entered a technical recession.

A key factor driving the export slowdown has been weak demand for Taiwan's electronics exports in key global markets, notably the US, EU and mainland China.

Taiwan slides into recession in early 2023

Taiwan's economy has recorded two successive quarters of negative growth during the fourth quarter of 2022 and the first quarter of 2023. This follows a period of strong economic expansion in 2021 and 2022. In 2021, annual GDP rose by 6.5% y/y. This was the fastest pace of annual economic growth since 2010, boosted by export growth of 29% y/y, with exports of semiconductors up by 27% y/y.

This was followed by continued positive GDP growth at a pace of 2.5% in calendar 2022, helped by strong global demand for electronics exports during most of 2022. Taiwan's merchandise exports rose by 7.4% y/y in 2022, buoyed by strong expansion in exports of electronics components, which rose by 16.4% y/y, while semiconductors exports rose by 18.4% y/y.

However, Taiwan's electronics sector exports, which are a key export, have weakened significantly during the second half of 2022 and early 2023, due to weak electronics demand in the US, EU and mainland China. The downturn in Taiwan's exports has been a key factor contributing to the economic slowdown.

Total merchandise exports fell significantly in the fourth quarter of 2022, contracting by 8.6% y/y. Taiwan's exports have remained weak during early 2023, with merchandise exports in March 2023 contracting by 19.1% y/y. Exports to mainland China and Hong Kong SAR declined by 28.5% y/y in March. Mainland China is Taiwan's largest export market, accounting for 28% of Taiwan's total exports, while Hong Kong SAR accounts for a further 14% of Taiwan's total exports. Exports to the US also fell sharply in March, down by 20.7% y/y.

Taiwan's manufacturing sector business conditions have remained weak during the early part of 2023. Industrial production fell by 14.5% y/y in March, with manufacturing output down by 15.2% y/y.

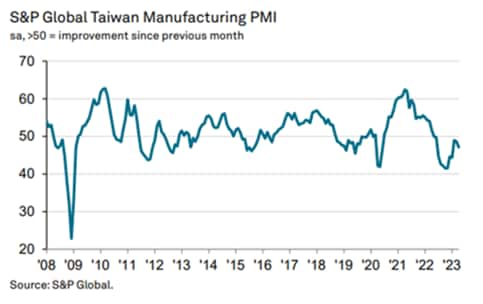

The S&P Global Taiwan Manufacturing Purchasing Managers' Index (PMI) fell from 48.6 in March to 47.1 in April, to signal a decline in the health of the sector for the 11th straight month. Pushing the headline index further below the neutral 50.0 level was a deterioration in total new orders in April. The contraction in sales reflected weak demand, both at home and overseas, and relatively high inventory levels at some clients.

New export business likewise fell at the quickest rate since January and sharply overall. Muted demand conditions led firms to cut production volumes again at the start of the second quarter. The pace of reduction of output was significant overall and the quickest for three months. Lower production requirements drove firms to cut back sharply on their input buying, while they maintained a cautious approach to their inventory holdings. Notably, stocks of both finished goods and pre-production items fell in the latest survey period.

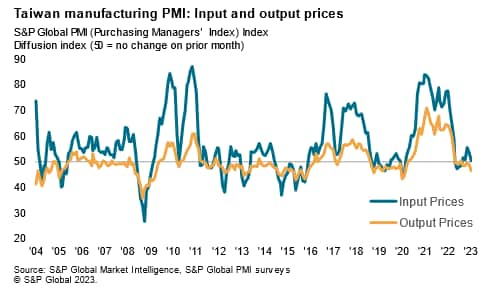

Waning demand for inputs meanwhile added further downward pressure on prices. Moreover, average input costs rose at the weakest pace in five months and only marginally overall. Efforts to stimulate sales led companies to cut their average selling prices again in April.

Taiwan's consumer price index (CPI) inflation rate moderated to 2.4% y/y in March 2023, while core CPI excluding energy and food rose by 2.6% y/y, indicating retail inflationary pressures remain contained. Although inflation has been moderating in recent months, Taiwan's central bank raised its policy rate by 12.5% on 23 March 2023 in order to limit potential further inflation pressures, after having acted pre-emptively during 2022 with a series of modest tightening steps to contain inflation pressures.

The March 2022 tightening step of 25 basis points (bps) had been the first rate hike since June 2011, with the previous most recent change to policy rates having been a rate cut in March 2020 in response to the global COVID-19 pandemic. This was followed by a 12.5 bp increase in June 2022, a 12.5 bp hike in September 2022 and another 12.5 basis points in December 2022.

Global headwinds facing electronics industry

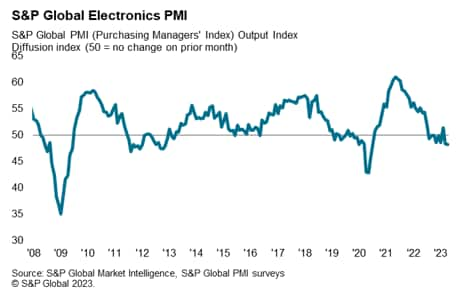

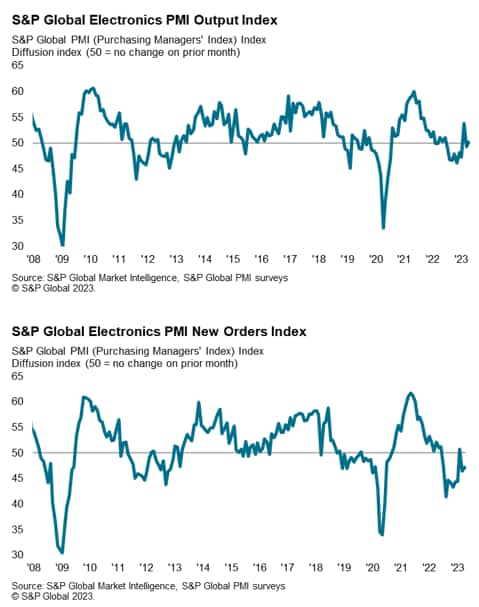

The near-term outlook for Taiwan's electronics sector remains weak, based on the latest S&P Global Electronics PMI survey results. At 48.2 in April, the headline seasonally adjusted PMI fell slightly from 48.4 in March to signal a sustained deterioration in operating conditions across the global electronics manufacturing sector at the start of the second quarter of 2023.

The Global Electronics PMI output index showed a marginal positive reading in April, but has been weak for many months. The Global Electronics PMI new orders index remained in contraction territory in April, with a reading of 47.2, well below the neutral 50.0 mark. These readings signal continuing headwinds for the global electronics manufacturing industry in the near term.

Global industry supply shortages for the semiconductors and electrical product industries have moderated in recent months, as supply-side bottlenecks have eased while weaker demand conditions have also contributed to improving supplier delivery times. The S&P Global Taiwan Manufacturing PMI Survey for April indicated that the weaker demand environment supported a further improvement in supply chain performance. Average lead times for inputs shortened for the second month in a row, albeit not as quickly as that seen in March.

Global electrical and electronics industry supply shortages

Economic outlook

After rapid economic growth in 2021 and continued firm expansion in 2022, Taiwan's economy is forecast to moderate in 2023, mainly due to the downturn in exports. This reflects continued weakness in key markets for Taiwan's electronics exports, notably the US, EU and mainland China. Taiwan's export orders fell by 25.7% y/y in March 2023, signalling continued near-term weakness for the manufacturing export sector.

Taiwan's medium-term outlook remains for sustained positive expansion at a moderate pace, underpinned by improving global electronics demand during 2024 and 2025. The impact of the COVID-19 pandemic has accelerated the pace of digital transformation due to the global shift to working remotely, which has boosted demand for electronic devices, such as computers, printers and mobile phones.

The medium-term outlook for electronics demand is underpinned by major technological developments, including 5G rollout over the next five years, which will drive demand for 5G mobile phones. Demand for industrial electronics is also expected to grow rapidly over the medium term, helped by Industry 4.0, as industrial automation and the Internet of Things boost rapidly growth in demand for industrial electronics. Taiwan's electronics industry will continue to benefit from its leading role in production of advanced semiconductors as well as from its production of a wide range of other electronics products for consumer and industrial electronics.

Rajiv Biswas, Asia Pacific Chief Economist, S&P Global Market Intelligence

Rajiv.biswas@spglobal.com

© 2023, S&P Global Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.