ECONOMICS COMMENTARY — Sep 18, 2024

Comparing the NBS and Caixin manufacturing PMI surveys

Download Full Report in Chinese (中文)

Comparisons between two PMI surveys for mainland China - one published by the National Bureau of Statistics of China (NBS) and the other by Caixin, compiled by S&P Global Market Intelligence - have often been made, especially during times when the figures diverge in short-term trends. Here we explore the most recent divergence for the manufacturing gauges in more detail, and draw the conclusion that both surveys are in fact sending similar signals on the health of the manufacturing economy in mainland China. While the Caixin PMI is slightly more aligned with official data over the year-to-date in terms of the production trend on average, it overstated growth late in the second quarter such that the NBS survey sent an earlier signal of a slowing manufacturing economy.

A tale of two PMIs

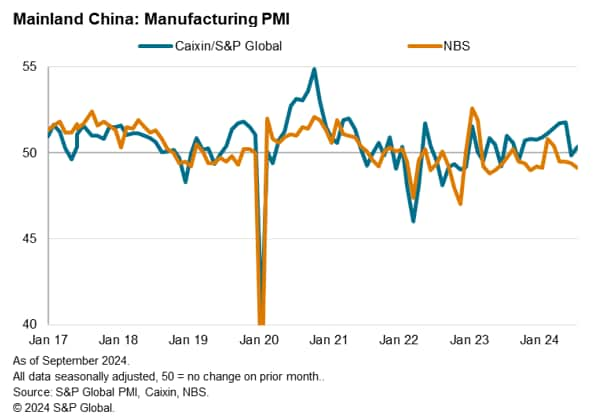

A gap has developed between the two manufacturing PMI surveys published in mainland China. The PMI survey compiled by the National Bureau of Statistics (NBS) has recorded lower readings than the PMI compiled by S&P Global Market Intelligence on behalf of Caixin. The NBS PMI has averaged 49.6 in the year to August compared with an average reading of 51.0 for the Caixin PMI.

Variations between the two surveys are by no means unusual, and in index points-terms the recent divergence is modest. Recent coverage in the markets and media of the two PMIs and their divergence is due to the diffusion index methodology used by the PMI surveys, whereby readings of 50 signify no change in business conditions. Hence, being marginally below 50.0, the NBS survey has been signaling modestly deteriorating manufacturing business conditions on average so far this year whereas, being slightly above 50.0, the Caixin PMI has been signaling modestly improving business conditions.

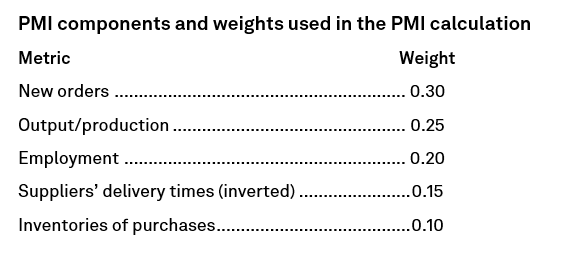

To understand more of this difference, we need to investigate the detail of the headline PMIs. These indicators are calculated from the weighted average of five individual survey indices, each of which is based on a question asking companies whether a given metric has risen/improved, fallen/deteriorated, or remained unchanged on the prior month. The variables with the greatest propensity to lead the business cycle are accorded the highest weight. Hence new orders carry the highest weight and inventories carry the lowest weight. The weights are the same for both the NBS and the Caixin PMI.

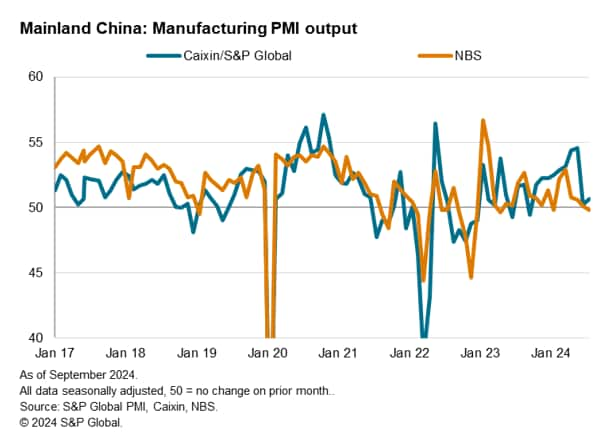

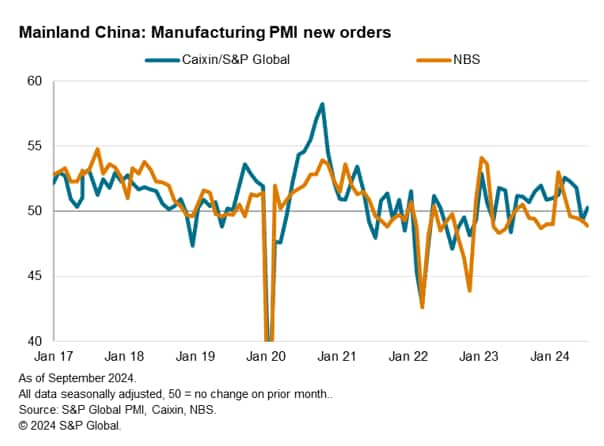

These PMI components from the two surveys are charted in the appendix, but recent trends can be summarized as follows:

- The Caixin survey has signaled stronger trends for both new orders and output than the NBS survey so far on average in 2024. This contrasts with typically higher readings of the NBS PMI compared to the Caixin PMI prior to the pandemic. The gap between the PMIs has narrowed since July August.

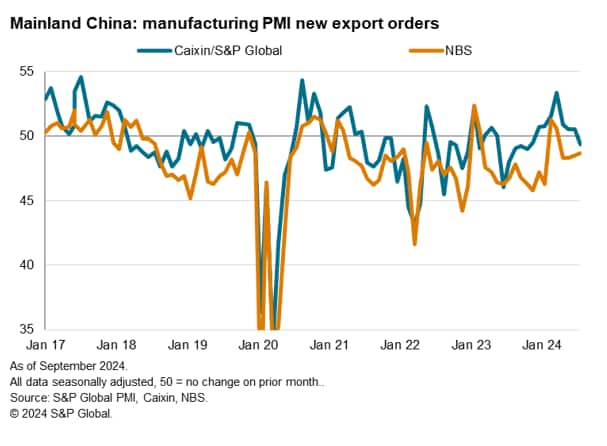

- The export orders element of the order book situation (not itself a PMI component but included via the New Orders Index) has notably also diverged, with the Caixin survey signaling stronger exports than the NBS survey so far this year, though the divergence has narrowed in recent months.

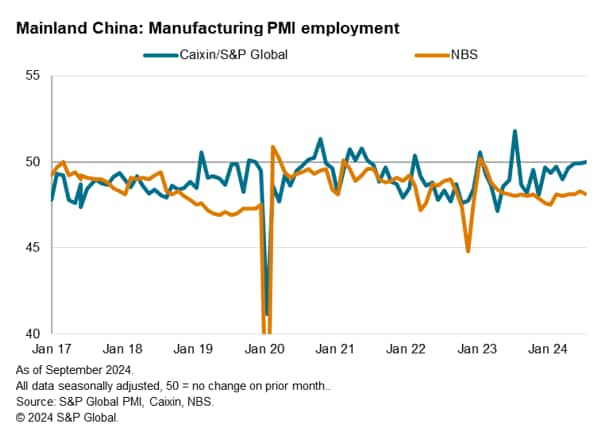

- The Caixin survey has signaled fewer job losses than the NBS survey so far this year, and even signaled no change in employment in August, in contrast to the job losses still being reported in the NBS survey.

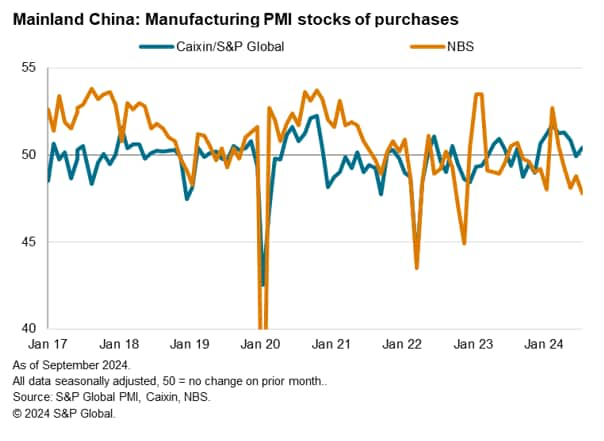

- The NBS data is signaling a steepening drop in inventories in August, in contrast to the modest growth trend being indicated by the Caixin PMI, and has generally signaled more incidences of inventory falls than registered by the Caixin PMI throughout 2024.

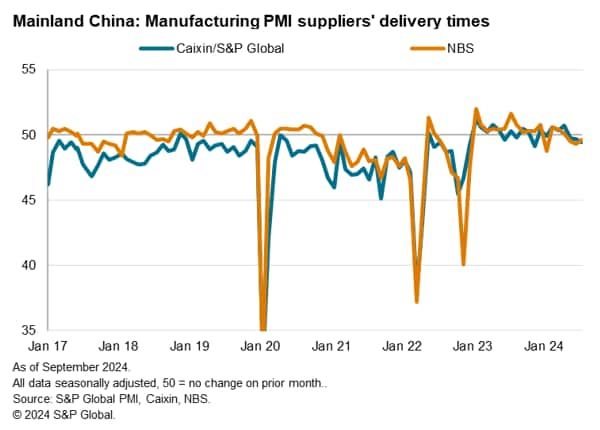

- The surveys have been indicating similar supplier delivery times trends throughout 2024, as has been the case since late 2021, though this matching performance is unusual: the Caixin survey has typically signaled more incidences of supply chain delays (associated with a busier economy) than the NBS PMI.

In short, the Caixin PMI has been elevated relative to the NBS PMI so far this year due to its signals of stronger new orders (notably exports), production, employment and inventories.

Assessing the divergence

To assess the significance of these divergences it is important to compare the PMI data with comparable official economic data, where available. This comparison requires the conversion of the PMI diffusion indices into comparable measures of official growth. This is achieved using OLS regression analysis, where the PMI index acts as the sole determinant of changes in the official rate of change in the variable being modelled.

The results of these regression analyses therefore provide clear and objective comparisons of the implied rates of change from the PMI surveys for official data where available.

In the case of mainland China, only official production data are available for comparison, and even here the official data are only available since 2018. Broader industrial production data are available, but this broader gauge is not directly comparable with the PMI manufacturing output index as it includes extractive industries such as mining and quarrying. Note also that, whereas the PMI measures month-on-month changes, we are limited to official data being available only on a year-on-year basis.

While official export data are also available, the PMI surveys measure these in volume terms whereas the official data record exports in value terms. Official, higher-frequency manufacturing employment data are no longer available, nor are data on new orders, inventories or supplier performance.

Manufacturing output comparisons

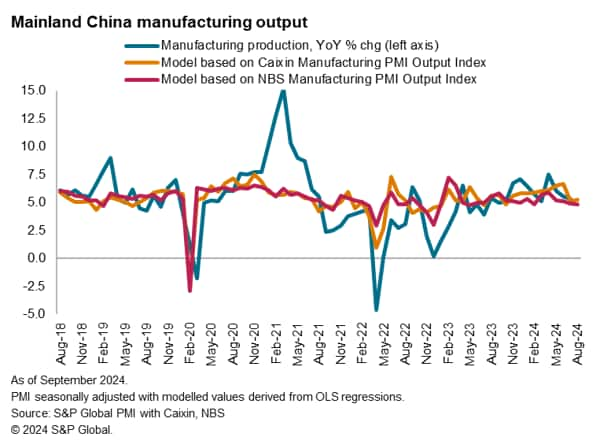

In the case of manufacturing production, the regressions from data over the past six years indicate that:

- The Caixin PMI's output index has been consistent with an average year-on-year rate of change in the official manufacturing production data of 6.0% in the first seven months of 2024, with a 5.2% rate signaled for August. That compares with an average 5.4% rate signaled for 2023. The Caixin PMI has therefore indicated stronger manufacturing output growth in 2024 so far compared to that seen on average over the whole of 2023.

- The NBS PMI's output index has been consistent with an average year-on-year rate of change in the official manufacturing production data of 5.3% in the first seven months of 2024, with a 4.8% rate signaled for August. That compares with an average 5.4% rate signaled for 2023. The NBS PMI has therefore indicated slightly weaker manufacturing output growth in 2024 so far compared to that seen over the whole of 2023.

The official production data have meanwhile so far shown a 5.9% average year-on-year rate of change in manufacturing production in the first seven months of 2024, with August data not yet available. That represents an improvement on the 5.3% rate signaled on average over the whole of 2023.

Thus, while both PMIs have been signaling similar robust rates of steady growth so far in 2024, the Caixin PMI is more in line with the official average growth rate according to the regression analyses, and has also been more in line with the official data showing the average year-on-year pace of expansion to have improved slightly in 2024 so far compared to the average seen in 2023.

That said, the Caixin PMI data were notably stronger than the NBS PMI and the official manufacturing data in June, hence being late in pointing to a slowdown in the rate of expansion.

Explaining the divergence

There may be several reasons for the PMI surveys to diverge, some of which are listed below:

- The surveys are produced by different compilers (S&P Global Market Intelligence and the NBS) and therefore use different samples of businesses to respond to the surveys. While both samples are carefully stratified to accurately reflect the true structure of the mainland Chinese manufacturing economy, there will inevitably be some differences.

- Both surveys are stratified using sample sizes proportionate to sub-sector contributions to total industry output. The S&P/Caixin survey weights responses according to company and sector size. It is not known if this practice is undertaken by the NBS.

- There are often assumptions made in the market, speculating that NBS focuses more on large state-owned enterprises (SEOs) whereas the Caixin PMI is biased toward smaller private sector firms, but the Caixin PMI in fact covers firms of all sizes with targets of accurate representation. Similarly, the NBS survey adequately covers smaller, private sector, firms to ensure this segment of the economy is correctly represented. Note that Caixin PMI data have shown smaller manufacturers underperforming relative to larger firms over the past two years and into 2024 (albeit with the divergence narrowing in recent months).

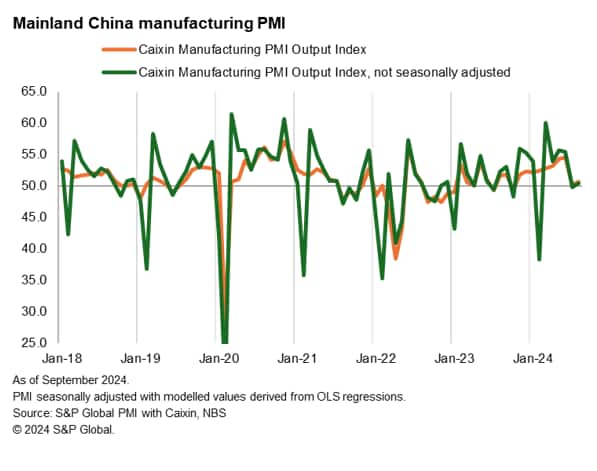

- The method of seasonal adjustments varies between the two surveys, with X12-ARIMA being used by both but potentially with different settings to allow for public holidays and other factors. In mainland China, the seasonal adjustment is made especially difficult due to the extended and changing timings of the Spring Festival. The non-seasonally adjusted Caixin PMI data are plotted below. It is likely that the impact of differing seasonal adjustment techniques is modest.

Appendix: PMI components compared

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

© 2024, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.