Case Study — 23 Feb, 2024

A Green Lender Adopts a Robust Approach for Assessing Project Finance Credit Risks

Highlights

THE CLIENT: A Pacific-based non-bank lender

USERS: Investment team

Many countries around the world are launching investment organizations aimed at helping their economies transition to a clean, carbon-neutral environment by supporting private sector investments in low-emissions projects. These organizations are often interested in scalable companies, technologies and projects that are commercially ready, and they provide attractive terms that cannot be met by the mandates of traditional investors.

Members of the investment team at this Pacific-based non-bank lender were looking to increase the deployment of capital (from senior debt facilities to equity) across low-emission industries. The portfolio would mainly comprise project finance or asset-based finance investments, with a small number being corporate loans. Given this, a new approach was needed for assessing credit risk to guide the team's investment selection and loan pricing, since the existing internal credit risk model was based on a corporate ratings methodology.

Pain Points

Project finance plays a vital role in funding infrastructure development and is a critical tool in green financing and the transition to a low-carbon economy. A key challenge, however, is assessing the creditworthiness of transactions that often lack extensive default data needed to build complex credit risk statistical models.

Members of the investment team at this non-bank lender wanted to have a structured and independent approach to reliably measure the probability of default (PD) and loss given default (LGD) associated with their debt investments. To support their efforts, they needed:

- — A proven methodology with dynamic interrelationships between qualitative and quantitative factors.

- — The ability to generate consistent and reliable credit scores[1] following a guided approach.

- — Transparency into the inputs and outputs.

- — An approach to evaluate what could be recovered in the event of a default.

- — A way to calibrate PDs with historical default data.

The team was familiar with S&P Global Market Intelligence ("Market Intelligence") and reached out to learn more about available capabilities.

The Solution

Specialists from Market Intelligence described the Credit Analytics suite of models and the Project Finance Credit Assessment Scorecard that, together, would provide a holistic and globally recognized solution for the team's overall investment exposures. This would enable the team to:

|

|

Compare internal credit risk assessments for corporates with external assessments | The Credit Analytics solution blends cutting-edge models with robust data to help users easily monitor counterparty creditworthiness. The models include Probability of Default Fundamental Model (PDFN), CreditModelTM and PD Market Signals Model (PDMS). Together, they provide the ability to assess rated and unrated companies of any size and put in place an early warning system to detect possible defaults.Credit Analytics' proprietary scoring capability enables users to evaluate results from internal models, including assessments of early stage companies and potential recovery after default. |

|

|

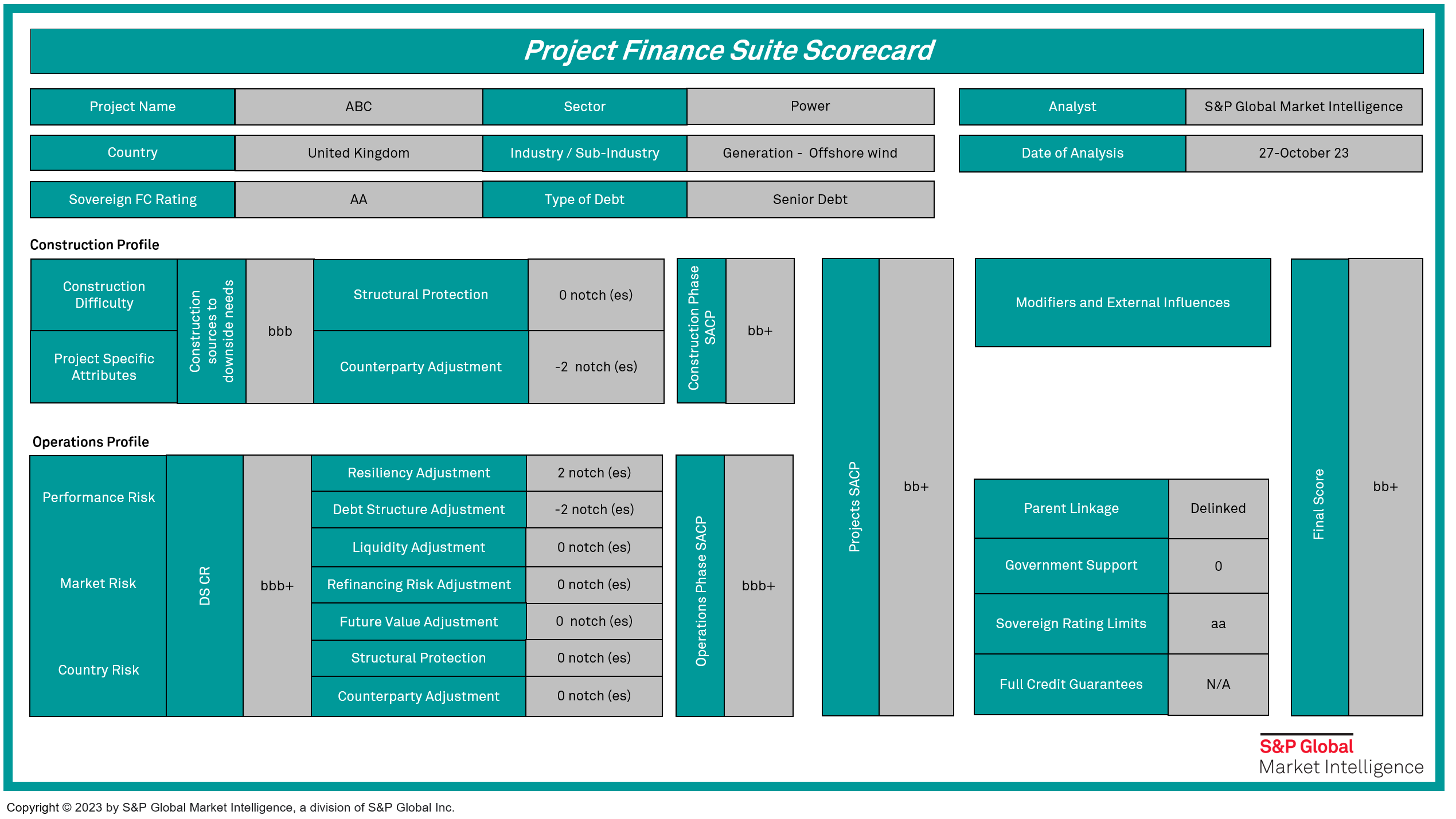

Evaluate the PD of a wide range of green projects | S&P Global Market Intelligence’s Project Finance Scorecards provide a general framework for the analysis of project finance transactions, across a range of sectors and geographies, with the use of well-established project finance debt rating criteria developed by S&P Global Ratings. The Scorecards capture atypical structures, can evaluate 100+ different project types and can run PD assessments from preliminary stage through the entire life cycle of a project. The framework is different from the corporate sector framework, including construction and operational risk as part the project-level assessment. |

Figure 1: Project Finance PD Scorecard Source: S&P Global Market Intelligence. For illustrative purposes only. Source: S&P Global Market Intelligence. For illustrative purposes only. |

||

|

|

Consider LGD in the analysis | The LGD Scorecards can supplement the PD Scorecards, bringing together statistically validated PD and LGD methodologies and market benchmarks to build a single, robust framework to identify and manage project finance credit risks. |

|

|

Evaluate potential recovery | Additionally, the LossStats™ model helps estimate the loss and recovery levels of fixed income and lending facilities, considering industry- and instrument-specific characteristics. Broad coverage helps users better understand the impact of specific collateral types on recovery statistics from all assets, including Plant, Property & Equipment, Real Estate, Oil & Gas Reserves, Intellectual Property and more. |

|

|

Have access to top-notch support | In-depth credit training is available on the application of the tools, and full technical documentation describes the analytical/statistical processes used to develop a Scorecard, identifies the data used in construction and provides testing performance results. A User Guide and PD mapping document are also available. In addition, annual recalibrations ensure that the Scorecards are highly predictive of default risk. |

Key Benefits

Members of the investment team saw the combination of Credit Analytics and the Project Finance Scorecards as a way to assess credit risk with confidence, consistency and convenience and subscribed to the capabilities. Quick deploymentwiththe off-the-shelf solution enabled them to free up resources for other activities, and they are now benefitting from having:

- — Assistance with decision-making on new projects, including pricing of contracts, provisioning for potential losses from bad loans and loan structuring.

- — A sound way to validate their corporate credit assessments by comparing results with a trusted external system.

- — An effective framework to navigate today’s project finance environment with easy-to-use tools that draw on a mixture of quantitative and qualitative questions in a check-box style to identify key risks.

- — A way to assess low-default portfolios that, by definition, lack the internal default data necessary for the construction of statistical models that can be robustly calibrated and validated.

- — Scorecard numerical scores that are broadly aligned with S&P Global Ratings’ criteria and further supported by historical default data from 1981.

[1] S&P Global Ratings does not contribute to or participate in the creation of credit scores generated by S&P Global Market Intelligence.