Research — April 23, 2026

Apple earnings preview: Q2 2026

By Melissa Otto, CFA

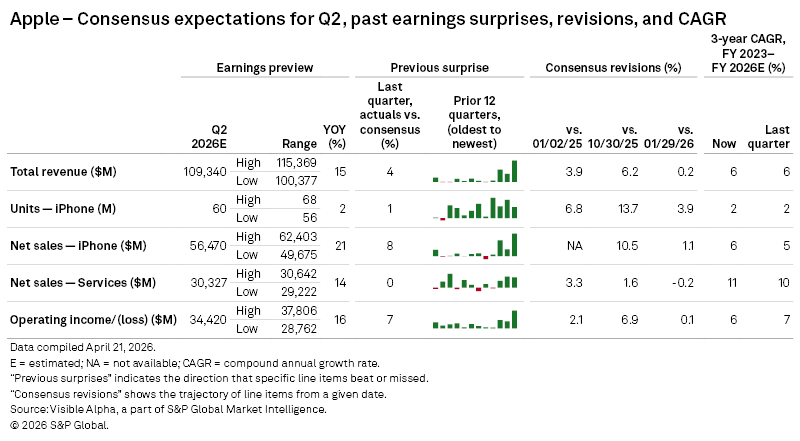

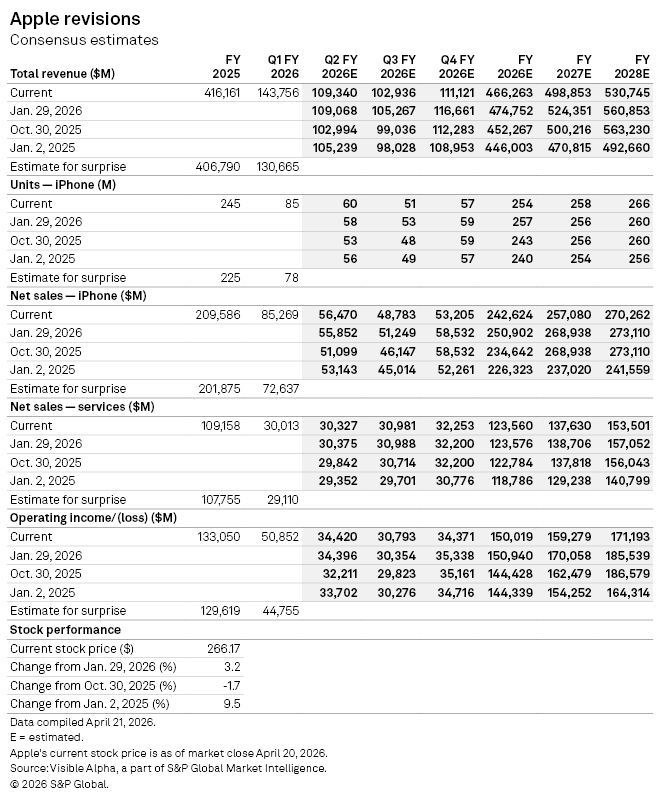

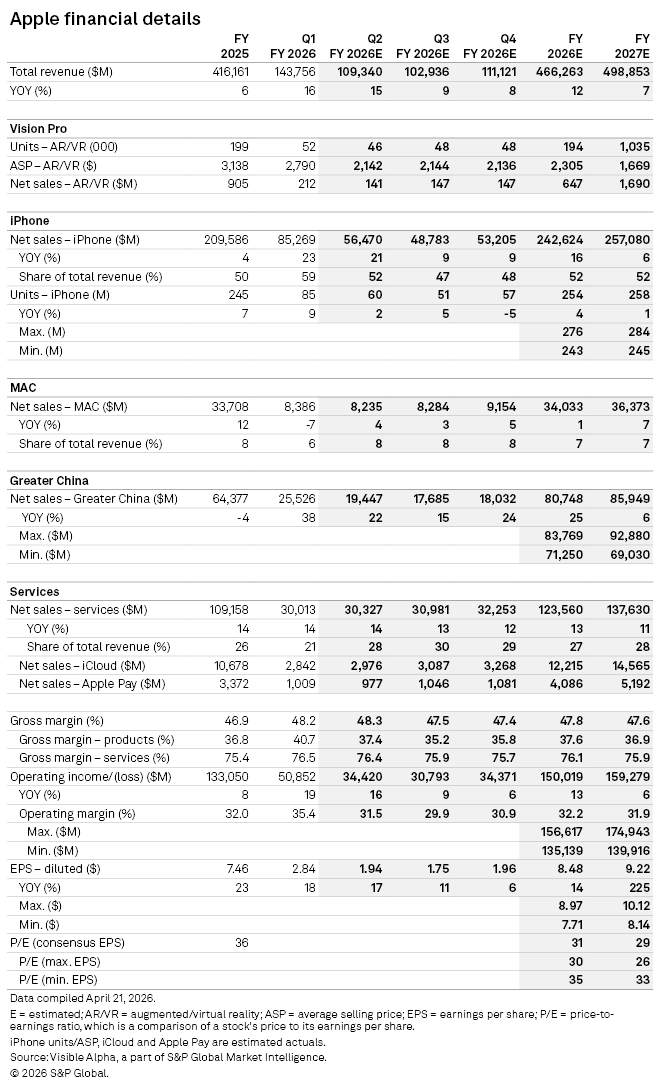

Apple's (NASDAQ: AAPL) total revenues expected for fiscal Q2 have ticked up since the fall but are flat from last quarter, according to Visible Alpha consensus, from $102.9 billion to $109.3 billion. Sentiment seems to reflect a view that iPhone buying is stable with improvements in China and users continuing to upgrade in the US. Since late January, expected Q2 iPhone units have edged higher to 60 million, but FY 2026 ticked down to 254 million. Currently, Q2 is expected to deliver $56.5 billion in iPhone sales and $242.6 billion in FY 2026 and $257.1 billion in FY 2027. Overall, large looming questions remain about the supply chain; however, iPhone expectations are continuing to show positive momentum this quarter, driven by upgrades.

Expectations for the high-margin Services segment remained stable for Q2 at around $30 billion. The gross margin for the Services segment is over 70%, significantly higher than the 37% gross margin for Products. Given the large installed base, we are looking forward to what the company says in the Q2 earnings release about growth in Services and the role of Apple Intelligence in FY 2026.

With CEO Tim Cook stepping down from September and new leadership taking the reins for the critical Back to School and Holiday selling season, the visibility of Apple Intelligence enhancements and new product roll outs will be a critical focus. In addition, will Apple use its over $100 billion cash position to buy back stock and increase dividends or make an acquisition?

Apple stock has been up almost 6% since last quarter. The consensus P/E for 2026 is 32x with a target price of $309. Could the Q2 release and outlook confirm the upgrade cycle and drive further outperformance in the stock?

Content Type

Products & Offerings