Research — February 18, 2026

Uranium’s next decade: From tight supply to a broader mining boom

By Arti Gupta

Global nuclear power is enjoying a renewed moment, as governments and corporates search for reliable, low-carbon electricity to meet rising energy demand. The surge in power consumption driven AI, data centers, and electrification is reshaping long-term energy planning, and pushing nuclear back into the center of the investment debate.

The International Atomic Energy Agency projects that global nuclear capacity could double by 2050, reaching between 561 gigawatts (low case) and 992 gigawatts (high case). Policy support is also strengthening. In May 2025, the US issued a series of executive orders aimed at quadrupling domestic nuclear capacity to 400 gigawatts by 2050, from roughly 100 gigawatts today. Other countries including China, India, Russia, Turkey, South Africa have also outlined expansion plans as they look to reduce dependence on fossil fuels and secure stable baseload generation.

Corporate demand is adding momentum. Over 2023 and 2024, several hyperscalers including Meta Platforms, Amazon's AWS, Alphabet, Microsoft, Oracle, and Equinix have announced a wave of nuclear-related initiatives, including power purchase agreements and equity investments in nuclear start-ups, signaling that big tech is increasingly willing to back atomic energy as a long-term solution.

This shift has brought uranium, the essential fuel for nuclear reactors, sharply back into focus. Prices have risen as demand tightens, and utilities move to lock in longer-term supply contracts at higher levels. Conditions are increasingly in place for a multi-year uranium upcycle, with benefits extending across miners, developers and the wider nuclear fuel chain.

Visible Alpha consensus forecasts suggest the industry is moving from today’s tight, concentrated supply base toward a broader and more competitive landscape.

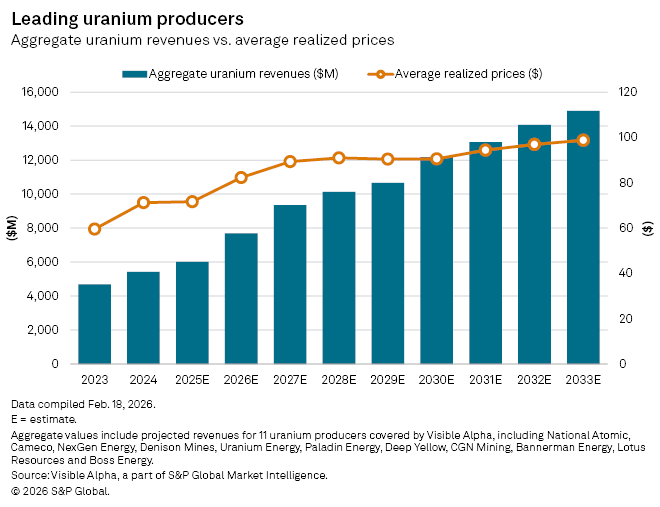

Aggregate uranium revenue across 11 listed global producers covered by Visible Alpha is estimated to climb from $4.7 billion in 2023 to $14.9 billion by 2033. Growth is strongest in the second half of the decade as new mines enter production. The revenue trajectory reflects both rising volumes and improving realized pricing.

Average realized uranium prices across the group are forecast to rise from $59.6 per pound in 2023 to $98.7 by 2033, with prices continuing to edge higher beyond that point.

Revenue: Kazatomprom & Cameco dominate

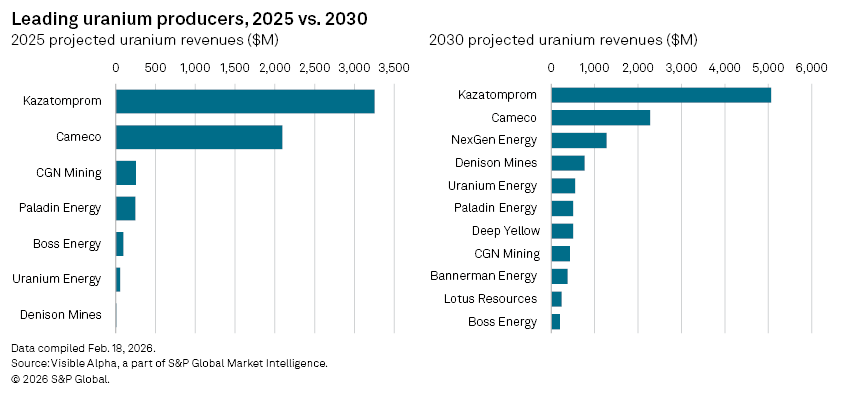

Despite the growing interest in new uranium supply, the market remains highly concentrated in 2025. Kazakhstan’s NAC Kazatomprom JSC (KAS: KZAP) and Canada’s Cameco Corp. (TSE: CCO) continue to account for the overwhelming majority of revenue and production.

Visible Alpha consensus forecasts show that Kazatomprom is expected to generate about $3.3 billion in uranium revenue in 2025, ahead of Cameco’s roughly $2.1 billion.

Both miners are also heavily geared to the commodity. Uranium accounts for about 91% of Kazatomprom’s total revenue and around 83% of Cameco’s, leaving earnings particularly sensitive to price swings and contract renewals.

Beyond the leaders, the market drops off quickly.

- China’s CGN Mining (HKG: 1164) is expected to post uranium revenues of $253 million in 2025

- Australia’s Paladin Energy (TSE: PDN) is seen generating $247 million

- Boss Energy (ASX: BOE) at $96 million

- US-based Uranium Energy (NYSE: UEC) is forecast at roughly $56 million, while

- Canada’s Denison Mines (TSE: DML) is expected to generate just $9 million

Over the longer term, however, supply is set to broaden. Developers such as NexGen Energy (TSE: NXE), Deep Yellow (ASX: DYL), Bannerman Energy (ASX: BMN), Lotus Resources (ASX: LOT), which are currently advancing projects through drilling programs and partnerships, are expected to contribute meaningful production within the next three to seven years.

While Kazatomprom and Cameco remain the anchors, the fastest revenue growth is seen among emerging producers including:

- NextGen, projected to see uranium revenues of $1.3 billion by 2030, up from virtually no revenue realization in 2025

- Denison Mines, moving from negligible revenue today to $768 million by 2030

- Uranium Energy, expected to grow from $56 million in 2025 to $548 million by 2030

Production set to surge after 2028

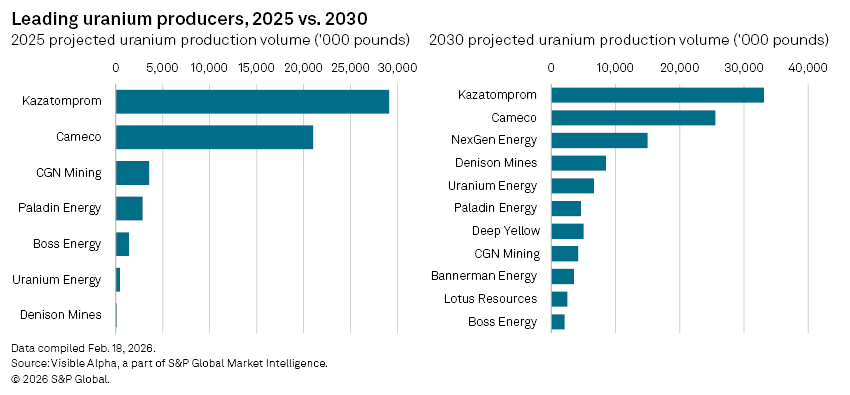

The production outlook tells the same story. Kazatomprom and Cameco’s production dominance is equally striking. Kazatomprom is projected to produce 29.1 million pounds of uranium in 2025, while Cameco is forecast at 21 million pounds. Combined, they account for roughly 86% of total output among the seven producers covered in this analysis in 2025.

The most notable shift in the Visible Alpha projections comes after 2028, when a second wave of producers begins to scale meaningfully. Total uranium production across the group is expected to expand from 58.5 million pounds in 2025 to 141.2 million pounds by 2033. That is a near 2.5x increase in less than a decade.

The incremental supply is driven by developers transitioning into production:

- NexGen Energy is projected to ramp to more than 14.9 million pounds by 2030

- Denison Mines rises above 8.5 million pounds by 2030

- Uranium Energy expands beyond 6.6 million pounds by 2030

- Australia-based developers including Deep Yellow, Bannerman, Lotus, and Boss Energy also add meaningful volume

Capital spending accelerates

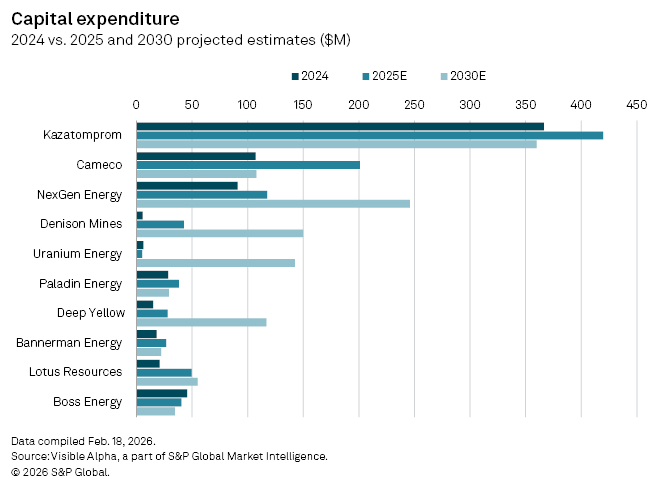

Capital spending (capex) is already accelerating. Aggregate uranium capex is expected to rise from $704 million in 2024 to $969 million in 2025, and a peak of $1.6 billion in 2027, before reducing to $1.5 billion in 2028 as big players like Kazatomprom and Cameco scale back investment.

Spending is front-loaded, with developers investing heavily before production begins:

- NexGen capex rises above $500 million by 2028

- Denison, along with Lotus Resources, accelerate capex sharply, with triple-digit growth rates in 2025 and 2026

- Paladin and Deep Yellow are also seen to scale investments

Over time, as the largest producers moderate spending, smaller entrants are expected to take on a greater share of investment.

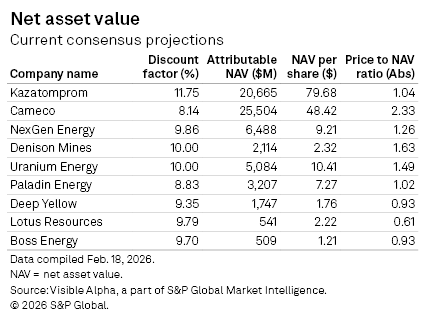

Price-to-NAV signals a two-tier uranium equity market

Looking at valuation metrics, Visible Alpha consensus net asset value estimates highlight an increasingly segmented market between premium incumbents and discounted developers.

Cameco remains the clear standout, with attributable NAV of $25.5 billion and a price-to-NAV multiple of 2.3 times relative to peers. Kazatomprom, despite its comparable asset base at $20.7 billion, trades much closer to intrinsic value at just 1.0 times NAV, suggesting geopolitical and jurisdictional risk continue to cap its valuation.

Mid-tier names such as NexGen, Denison, and Uranium Energy sit in the middle, trading between 1.3 and 1.6 times NAV, indicating markets are already pricing in meaningful upside from projects still moving through the buildout phase.

In contrast, smaller Australian developers Deep Yellow and Boss trade below NAV, while Lotus Resources trades at only 0.6 times.

Overall, Visible Alpha projections suggest the uranium market is moving into a fundamentally different phase. 2025 remains defined by tight supply, improving pricing and dominance by major producers. But by the early 2030s, a wave of new production reshapes the supply curve, with output more than doubling and developers turning into meaningful competitors.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment