Fertilizers, Chemicals, Energy Transition, Agriculture, Maritime & Shipping, Renewables, Meat, Dry Freight, Grains, Livestock

March 06, 2026

FACTBOX: Middle East war raises farm-to-fork food inflation risks on fuel, freight, fertilizer disruptions

HIGHLIGHTS

War drives fertilizer prices up 10%

Hormuz shipping traffic drops 75% in days

Food inflation risk spreads via supply chain costs

The Middle East war is raising the risk of food inflation following the upward trajectory of fuel, freight and fertilizer markets, as concerns grow that farm-to-fork price transmission will deepen throughout 2026 due to disrupted trade flows and energy-intensive inputs at multiyear highs.

The Philippine Department of Agriculture said March 3 it was closely monitoring the conflict's impact on food and trade, warning that any prolonged escalation could quickly feed through via higher fuel, fertilizer and freight costs.

The country, which is a key importer of grains and fertilizer, warned March 5 of "heightened food security risks" as the diversion of shipments around the Cape of Good Hope is adding significant lead times and costs to basic staples.

A prolonged conflict could become a broader supply shock, with higher energy costs, disrupted logistics and a renewed inflation impulse across import-dependent economies, ING Global Markets Research said.

The "geopolitical risk premium is now fully embedded in the food-energy-freight nexus, threatening to further push 2026 food CPI in vulnerable markets," it said.

The war could have significant impacts on global sheep meat markets, although this will clearly depend on how long hostilities continue. A prolonged conflict would force Australia and New Zealand to redirect lamb away from the Middle East, said analysts from S&P Global Energy CERA in their Monthly Prices Report: Meat and Livestock.

"For India, a prolonged conflict in the Middle East could seriously impact bovine meat exports. Countries in the region spent more than US$2 billion on imports of Indian buffalo meat in 2025."

The following are key facts on how the conflict could impact farm and food prices.

Trade

- Agricultural cargoes have already started to slow, divert or pause around the Persian Gulf. Shippers are considering unloading cargoes in Oman to bypass the Strait via land routes, though the viability of this for large-scale deliveries to Kuwait or Iraq remains uncertain.

- Europe-based fertilizer producers have withdrawn offers to wait for market clarity, creating a supply vacuum that is being filled by higher-cost US and Southeast Asian origins.

- War-risk insurance costs have risen 50% for Persian Gulf transits, contributing to a 75% reduction in shipping traffic through the Strait of Hormuz.

- The Philippines' agriculture department said the transmission channels for an import-dependent farm system are immediate because higher bunker fuel costs can raise shipping rates and increase the landed cost of imported wheat and animal feed, which would then spill over into bread, poultry and pork prices.

Prices

- Fertilizer prices are moving rapidly. Platts, part of S&P Global Energy, assessed ammonia FOB Middle East at $505/metric ton March 4, up $30/mt from Feb. 27, as three ammonia ships were stranded in Hormuz, according to S&P Global Commodities at Sea and shipbrokers.

- Global agriculture hub Brazil saw granular urea prices rise to $540-$545/mt CFR March 3, the highest daily level since Platts began that series in August 2025.

- The US nitrogen market surged, with granular urea in New Orleans assessed at $540-$550/short ton FOB March 2, the highest since Platts began the assessment in August 2025.

- The supply chain shocks reverberated in China. Zhenjiang ex-works fertilizer prices rose to Yuan 4,500/mt March 4 from Yuan 4,100/mt Feb. 27, roughly a 10% increase in three days, while a 5,000-metric-ton South Korean cargo traded at $540/mt CFR China River.

- Other major food input prices like phosphates and sulfur are also rising. Platts assessed sulfur CFR China at $519-$522/mt Feb. 26 and diammonium phosphate fertilizer FOB China at $680/mt. The increased sulfur prices reinforced expectations that nitrogen, phosphate and potash would all trend up if the disruption persists.

- Protein and grain prices are beginning to reflect the logistics disruption. Platts assessed 90CL beef FCA Australia at $7,973/mt March 4, up 3.3% day over day, chicken leg CFR North Asia at $3,250/mt, up $50/mt day over day, and pork belly CFR North Asia at $4,620/mt, up $20/mt day over day.

- In grains, corn CFR Northeast Asia was assessed at $252/mt March 2, up $1/mt day over day, while US corn CIF New Orleans was assessed at $213.30/mt Feb. 27, up $1.40/mt day over day.

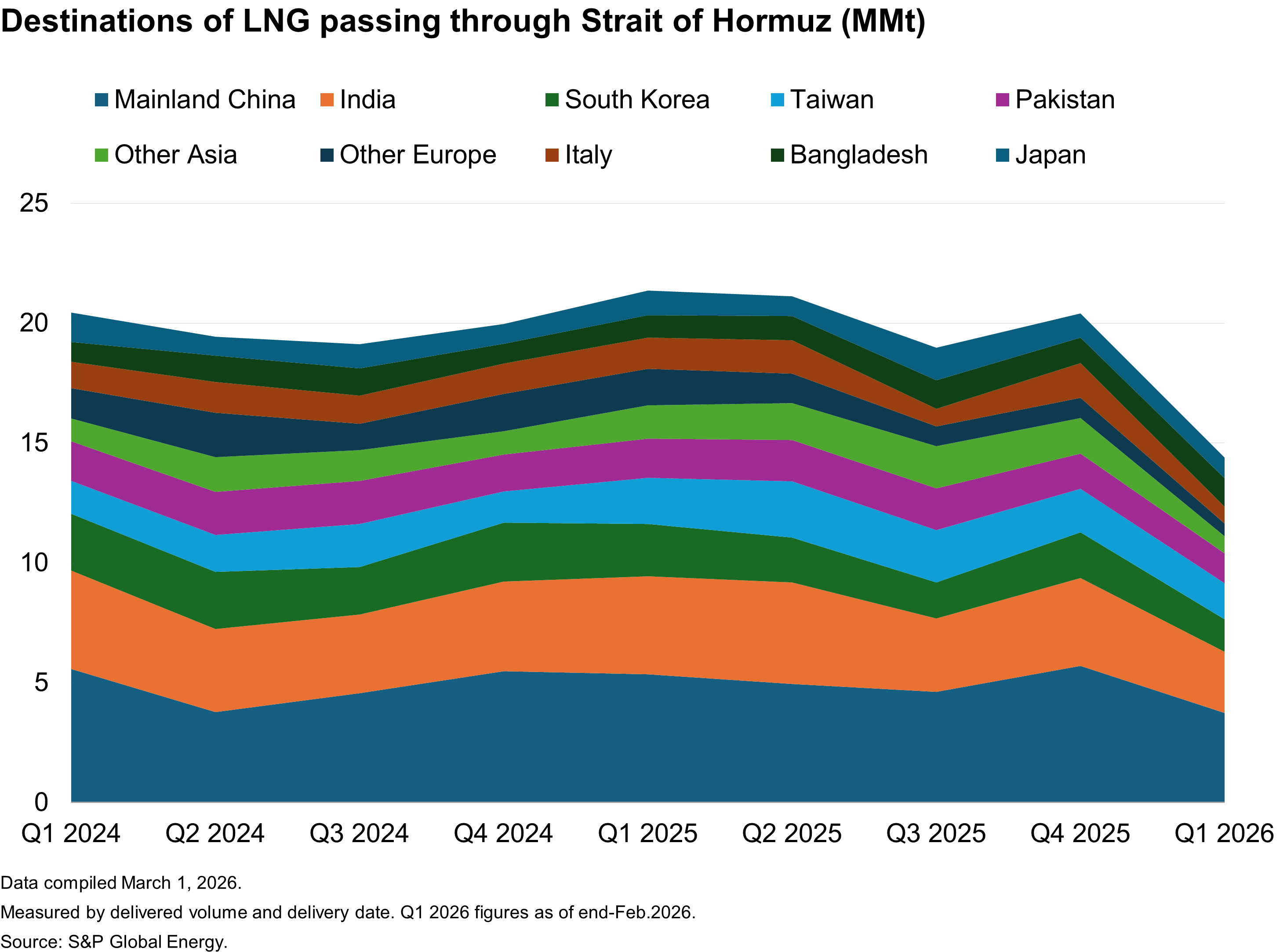

- Platts assessed JKM -- the benchmark price reflecting LNG delivered to Northeast Asia -- at $22.02/MMBtu March 5, up from $10.70/MMBtu Feb. 27, showing how quickly energy disruption can feed into fertilizer costs and then into food production economics.

- Additionally, container carriers have imposed emergency war surcharges of $2,000/TEU and $4,000/FEU on some Middle East cargoes, while major lines have suspended or rerouted services, raising freight costs and extending transit times.

- Some dirty tanker operators have seen freight rates triple since Feb. 27, underscoring how transport costs are feeding directly into delivered energy and commodity prices. Platts assessed cross-Mediterranean freight at $31.12/mt March 4, up 45.42% day over day,

Infrastructure

- Even a partial disruption to the Strait of Hormuz would amount to a supply shock of substantial proportions, ING said. The Philippines' DA statement highlighted the same point, calling Hormuz a narrow but critical waterway through which a significant share of the world's oil supply passes.

- Three ammonia ships — the 25,000-mt Green One, the 26,000-mt Eco Oracle and the 25,000-mt Searambler — were stranded in the western Strait of Hormuz as of March 4, according to CAS data

- Under normal circumstances, Persian Gulf producers ship around 15 million b/d of crude and 5.5 million b/d of refined products to the global market. A March 4 note from the US investment bank Goldman Sachs said five additional days of minimal transits through the Strait of Hormuz could result in "about 200 million barrels of Middle Eastern crude production losses" in March, equivalent to about 6.5 million b/d averaged over the whole month.

- Gas infrastructure has also taken a direct hit. Qatar Energy declared force majeure to affected LNG buyers on March 4 after halting production March 2. Qatar exported 82.4 million mt of LNG in 2025, representing just under 20% of global exports, according to CERA data.

- All 12 members of the International Group of P&I Clubs rolled back war-risk coverage for ships in the crucial Persian Gulf and Iranian waters, with cancellations taking effect from March 5, directly tightening ship availability and pushing freight higher.

- Rerouting around the Cape of Good Hope adds 10-14 days to a voyage and raises fuel burn by about 30%, which supports higher bunker fuel demand and a sustained freight premium.

- The conflict has resulted in immediate cost pressures for Australian importers and exporters, Australia's Freight & Trade Alliance and the Australian Peak Shippers Association said in a joint statement March 3.