Natural Capital and Biodiversity: Reinforcing Nature as an Asset

This report reflects the discussion held by the S&P Global Ratings Sustainable Finance Scientific Council on March 11, 2021.

Published: April 22, 2021

By Maurice Bryson, Michael Wilkins, and Marion Amiot

Highlights

Climate change and biodiversity loss are interlinked, but solutions to reduce greenhouse gas emissions are unlikely to benefit biodiversity in the same way.

Instead, biodiversity needs to be given equal consideration in any nature-based climate solution offering.

The biodiversity crisis is a still-nascent ESG consideration for investors but it is climbing up the agenda.

Governments and companies are increasingly viewing the incorporation of natural capital into assessments of wealth and performance as fundamental to addressing biodiversity loss.

Targeted corporate and government actions to reduce deforestation linked to soy, beef, and palm oil will form a key part of the response, as will supporting smallholder farmers and indigenous communities to protect nature.

Biodiversity Loss – Where Do We Stand?

Biodiversity loss is a global phenomenon. The recent intergovernmental report on biodiversity and ecosystem services estimates that of the eight million plant and animal species on earth (75% of which are insects), around one million are threatened with extinction. In the U.S. and Canada, bird numbers have declined by a third since 1970, with even the most abundant species, like starlings, seeing a 49% decline over the same period. The Yangtze River dolphin, last seen in the early 2000s, is thought to be the first dolphin species to be driven to extinction by humans. Australia’s regent honeyeater is also facing extinction because declining numbers are inhibiting the males’ ability to learn their courting song.

What can governments and corporations do to reverse these alarming trends? The first step is to acknowledge the implications of the destruction of nature. Increasingly, biodiversity loss driven by habitat degradation and climate change, as well as by the introduction of invasive species and other anthropogenically-induced factors, is being recognized as a systemic risk with far-reaching consequences. The World Economic Forum estimates that more than half the world’s GDP, or $44 trillion, is moderately or highly dependent on nature and its services. With such a dependence on nature, why are we systematically destroying it? The question is perhaps best answered with another: what is driving the biodiversity decline?

The answer, on land at least, is relatively simple. Terrestrial biodiversity loss is tied to three consumer staples: palm oil, beef, and soy. These soft commodities are responsible for around 70% of the 10 million hectares of natural habitat that the UN Food and Agriculture Organization estimates is lost to deforestation globally each year. Marine biodiversity is also suffering, with shark and ray populations declining by 71% since 1970, driven by an 18-fold increase in fishing pressure, meaning that extinction is now a near-term risk. Such is the complexity of nature that the loss of a top-level predator from our oceans could have other far-reaching and unforeseen effects.

Indeed, with the COVID-19 pandemic we are experiencing how an invisible shift in nature can manifest as a global socioeconomic crisis. Many are beginning to note the connection between habitat or biodiversity loss and the growing risk of emerging infectious diseases, especially zoonoses (70% of emerging infectious diseases), upending society.

As this crisis has shown, the health of nature can determine our own wellbeing. However, despite this understanding, actions to stem biodiversity loss are not entirely obvious--as we see when we look at corporations' responses.

Nature’s Complexity Obscures Its Financial Materiality

Business and finance may have a key role in stopping the destruction of nature. Though some corporations are proactively addressing the nature-related financial risks that stem from biodiversity loss--such as disruption to supply chains or volatility in raw material prices--many more are unaware of such risks. The more complex and less palpable issues to which they are financially exposed--given their reliance on fragile, interconnected ecosystems--are especially underappreciated. Indeed, there is a historical disconnect between investee companies addressing nature loss and the questions investors are asking. This disconnect has been exacerbated by a lack of transparency and disclosure of nature-based metrics in companies’ financial reporting. The heterogeneity of biodiversity (the World Wildlife Fund records 867 distinct terrestrial assemblages of species and communities across the world) and its nascent status as an ESG concern, makes it difficult to aggregate biodiversity data at the enterprise level and to achieve consensus on relevant biodiversity metrics for companies.

Furthermore, though biodiversity is creeping up the agenda, climate change still dominates. Taking Larry Fink’s latest letter to CEOs as an example, "climate change" features about 27 times while he does not mention "natural capital" or "biodiversity" at all. Perhaps it is the complexity of biodiversity, or confusion about what biodiversity and natural capital are, that is causing this rift. Or maybe it is the current absence of direct and material financial ties to nature that explains why investors are not making ecosystems a focal point of their ESG analysis.

Nature-focused accounting, therefore, seems like a plausible way for corporates to prioritize nature-related risks and opportunities. One way would be to assess resource efficiency via an input approach--that is, the total input of natural capital that goes into a product across the value chain (where the output approach measures the greenhouse gas emissions, pollution, and waste caused by the creation of that product). Using an input assessment of resource efficiency would permit the inclusion of natural capital in profit and loss accounts, offering a more comprehensive assessment of the total economic cost of production and giving a more accurate representation of profit that factors in positive and negative externalities. Such methods of accounting can also be applied at the national level.

Biodiversity can be understood as the variety of life on earth, or the variation that exists in the natural world, such as the genetic variability between a group of individuals of one species, or between that species and another in its community--or between a whole ecosystem and another. The heterogenous nature of biodiversity--using species richness or the number of species in a given area, as a proxy measure--means that about 50% of all terrestrial species are found in just 7.2% of the global land area, with the Amazon, south-eastern Brazil, and parts of central Africa being the most notable biodiversity hotspots. Biodiversity is a measure of the variability that exists in “living” natural capital, and therefore is a feature of natural capital.

Why Accounting For Natural Capital In Wealth Is Not Enough

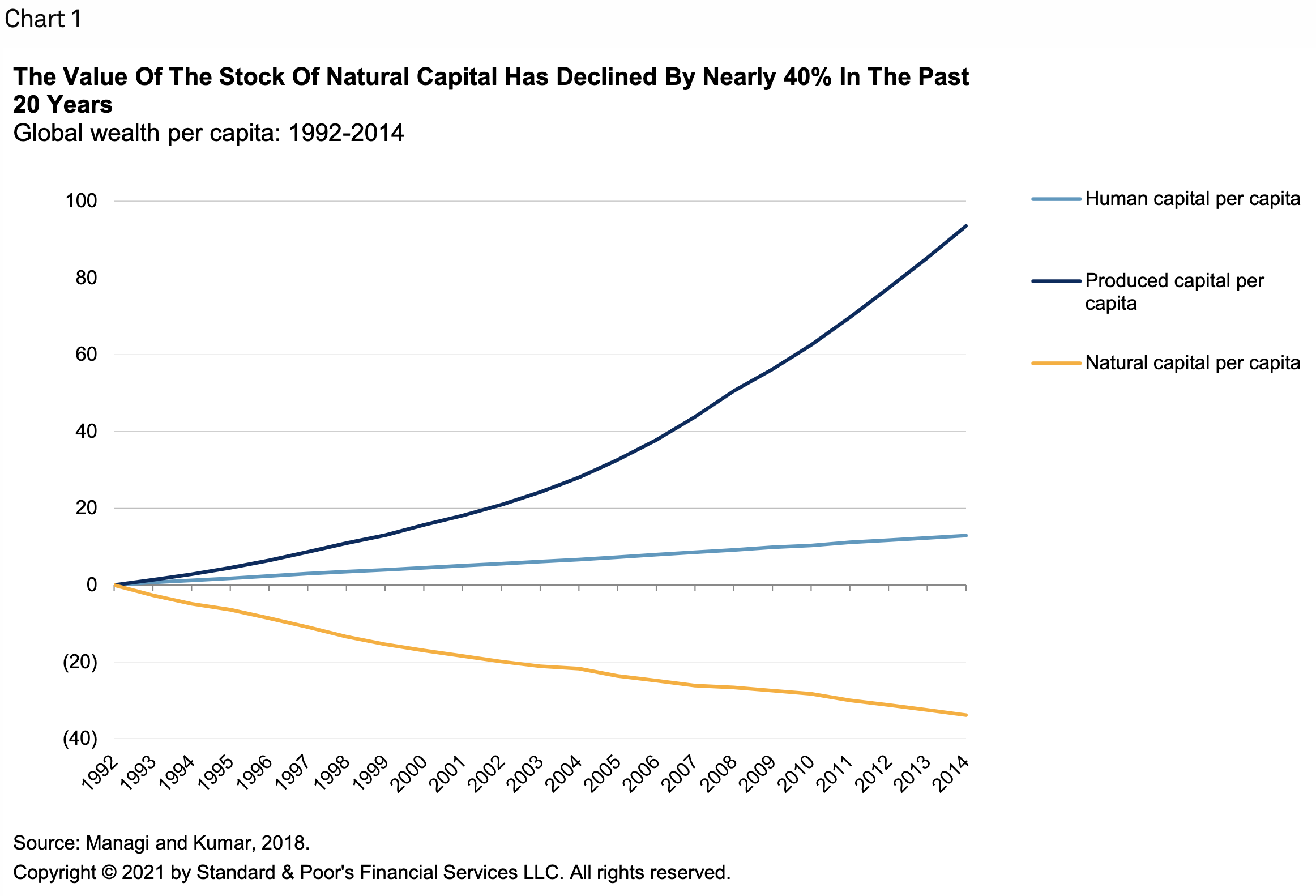

Perhaps the solution to our prodigious loss of nature lies in how we measure economic growth. One suggestion to improve our management of natural capital is to include the stock of natural resources available to us when we assess wealth. Professor Sir Partha Dasgupta of the University of Cambridge explains in his recent review that "sustainable economic growth requires a different measure than gross domestic product." He says we should adopt not just a flow (GDP) but also a stock approach to wealth--that is, one that considers the aggregate value of all capital assets--to take our use of natural capital into account (see chart 1).

A key reason why natural capital is still largely neglected, and is in decline (chart 1), is that it is a global public good--it can be accessed or used by all. Nature’s ubiquity and lack of ownership gives rise to the “free rider” problem, whereby users have no monetary incentive to contribute to or share the cost of its preservation. As Dasgupta highlights, coordination is even more difficult as biodiversity is silent, invisible, and mobile, decreasing users’ awareness of the ecosystem services they use. Equally, nature extends across borders. For instance, oceans are mostly open and free for all to use, so unilateral policies to address overfishing or water pollution might not only prove insufficient but also likely leave the first mover worse off.

The free rider problem has amplified calls to put a price on nature. In theory, pricing would be the most effective way to push firms and individuals to account for environmental damage. However, understanding and capturing the value of natural capital is still a relatively new concept and challenging to incorporate into policy making. The UN’s System of Environmental Economic Accounting is among the more advanced attempts to create a natural capital accounting system but has yet to be widely adopted.

From a macroeconomic standpoint, putting a price on nature through ecosystem accounting can raise our awareness of our use of, and impact on, nature for productive purposes. However, it can also be a source of false precision because it equates value with price. As such, it is unlikely to reliably indicate optimal natural capital usage, points of no return associated with nature’s depletion, or nature’s future benefits, when all these factors are subject to radical uncertainty. Pricing nature also raises questions, such as whether the intangible benefits of nature--for example those associated with wellbeing--can be measured at all, or whether nature should be valued in relative terms. For example, is a tree more valuable in the Amazon rainforest than in the U.K.? Pricing, therefore, cannot be the sole solution to preserving nature. Professor Dasgupta suggests quantity restrictions for when we don’t know how to value nature’s services, and notes that nature’s limits cannot always be overcome through technological advances.

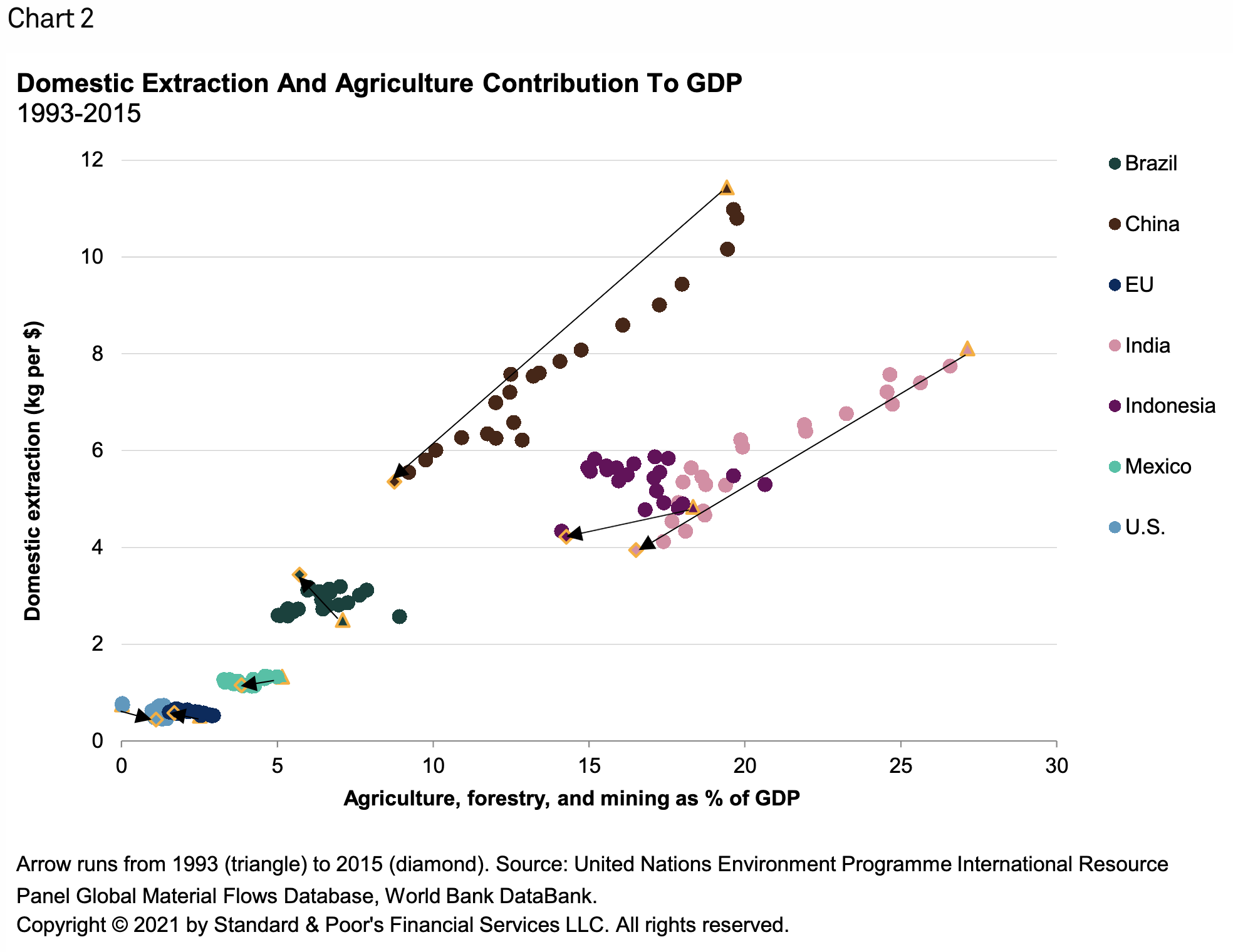

Some measures of resource-use efficacy also paint a misleading picture. A country’s nature usage per unit of output may be declining, but this could be because the relative contribution of agriculture-based growth is diminishing in total output and not because the production system itself has changed (chart 2). This caveat is notably shown in data from emerging economies in Asia-Pacific, such as China, India, and Indonesia, when we look at domestic extraction volume per unit of output as a proxy for natural capital usage.

Notwithstanding issues related to natural capital accounting, policymakers and institutions have started to incorporate nature preservation into policy measures. Globally, more countries have taken a user-pays approach to ecosystem services and protected areas. Trade deals are setting incentives to deal with the cross-border aspects of the problem. For example, the EU-Mercosur trade agreement includes a sustainable development chapter that covers issues such as the conservation of forests. On a local scale, the EU’s biodiversity strategy lays out steps to preserve biodiversity such as increasing protected areas (30% of member states’ land and seas to be protected by 2030), reducing pesticide use, and allocating an additional €20 billion to biodiversity annually.

Yet not all initiatives are proving effective, nor are they being applied coherently in policy making. While one policy might support biodiversity, another might harm it. Dasgupta highlights that nature-damaging subsidies still amount to around US$4 trillion-US$6 trillion per year, globally. Even if trade deals can encourage biodiversity preservation across borders, they are still subject to data comparability problems and a lack of transparency as to how nature is actually being used. Also, rules can exist but, absent an enforcement mechanism, those rules are likely to be less effective if there are few consequences for rule breakers. As highlighted in the Macron-commissioned report on EU-Mercosur's sustainability chapter, countries are not being held accountable for deforestation nor for their climate commitments. Additionally, trade deals boost demand. With the EU-Mercosur deal, this could lead to increased demand for agricultural products such as Brazilian beef. With no price changes affecting incentives to preserve biodiversity, the risk of deforestation in the Amazon is likely to be exacerbated.

Companies And Investors Have A Key Role In Biodiversity

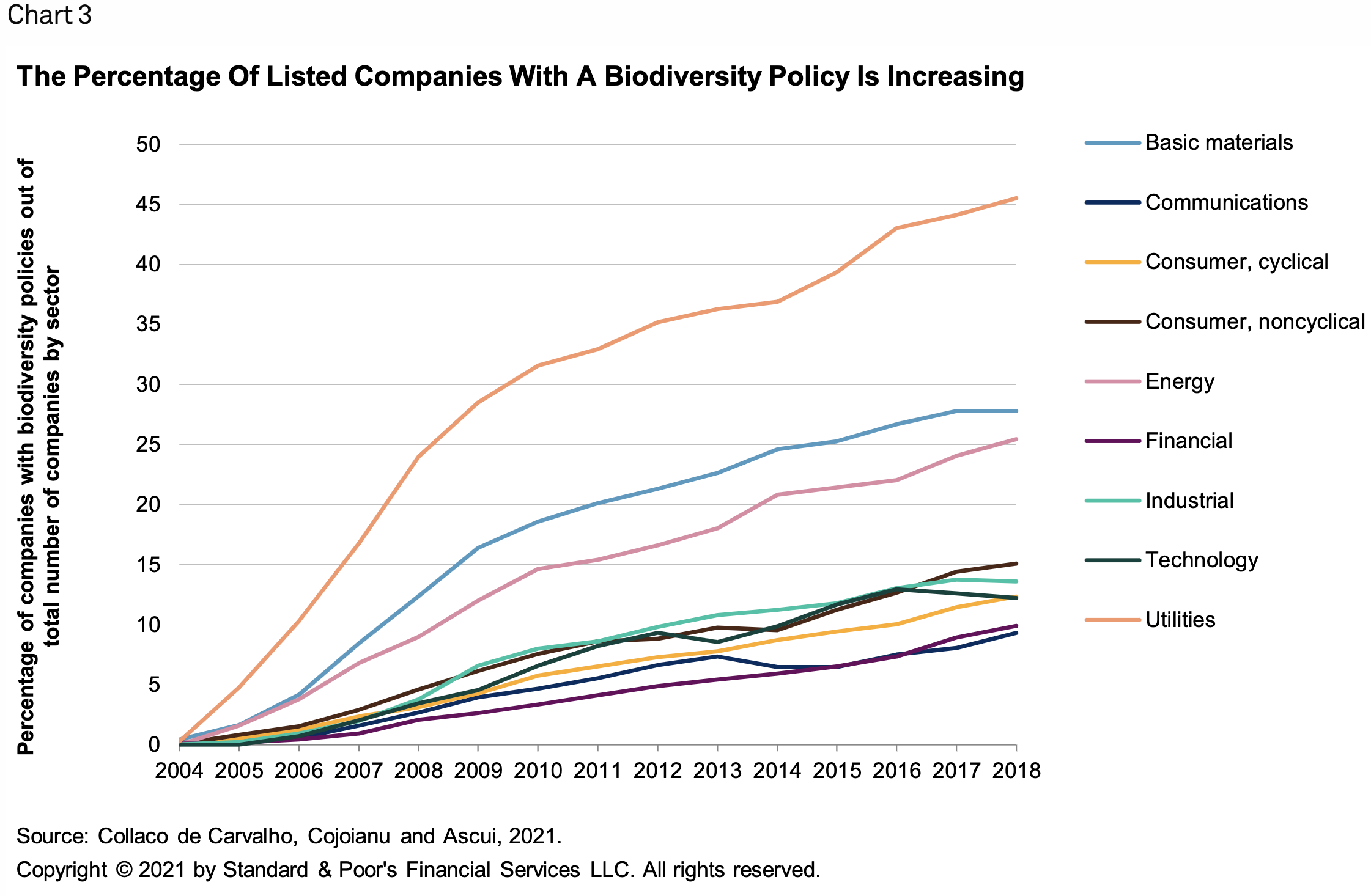

As we see tentative signs of progress to protect nature at the national level, a similar growth in awareness is being seen among corporates. While still in the minority, the percentage of listed companies with biodiversity policies is increasing (chart 3). However, policy does not necessarily equate with implementation. Similarly, there is evidence that investors are starting to pay attention to their investee companies’ reliance on unpriced natural capital in those sectors most highly and immediately exposed to biodiversity risk, such as soft commodities. Many of the largest institutional investors are signatories of the Cerrado Manifesto Statement of Support, which advocates a halt to deforestation in the Brazilian Cerrado, a 200-million-hectare tropical savanna famed for its biodiversity and a key source of soy for European and Chinese livestock producers. Though investor engagement initiatives may have clear biodiversity goals, direct investments--such as the purchase of real assets or offsets under REDD+--are often more focused on climate change mitigation than biodiversity protection. In a recent Environmental Finance survey of 168 financial institutions engaged in natural capital investments, resilience against climate change was the most cited motivation for investing in natural capital.

Supply Chain Management

Efforts to address terrestrial biodiversity loss are likely best made at the source: the soft commodity supply chain. Between 1991 and 2005, it is estimated that more than 80% of deforestation in Brazil was linked to beef production. This clear link to natural capital destruction has led to concerted pressure on the three largest Brazilian beef producers to monitor their supply chains. In September 2020, JBS, the world's largest animal protein company, agreed to monitor its entire supply chain by 2025. Yet given the breadth of its direct and indirect supply chains--JBS states that it has 50,000 direct suppliers but does not disclose the number of indirect suppliers--monitoring is not without its difficulties. Advancements in satellite imagery and tracking systems are providing solutions but it remains unclear when and if attestations (JBS had originally pledged to monitor indirect suppliers by 2011) and technologies will halt the deforestation of the Amazon.

Case Study: Tackling Deforestation In Palm Oil Supply Chains

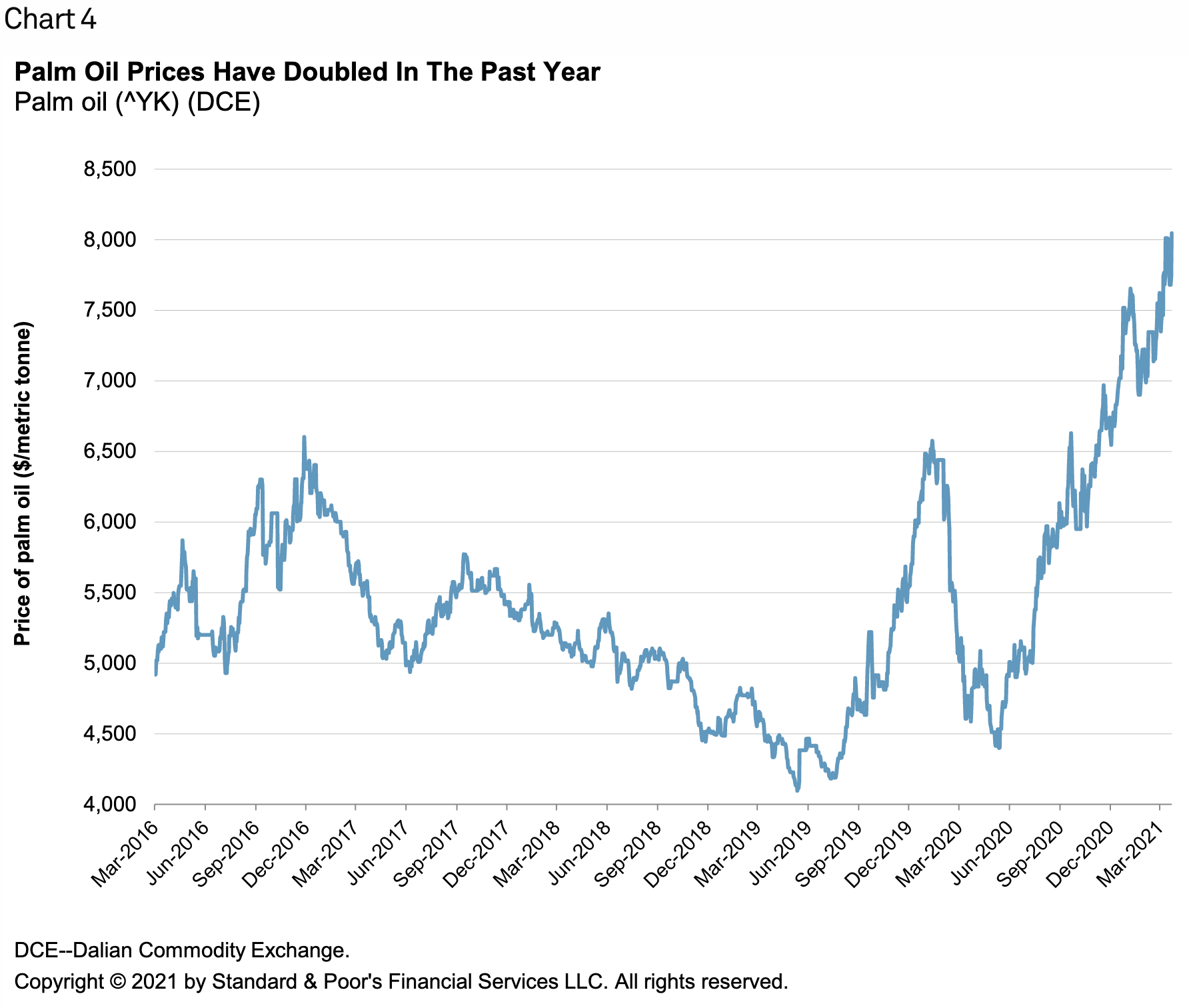

In southeast Asia, supply chain monitoring seems more advanced than in Brazil. Prolonged campaigns originally targeting palm oil refineries and latterly off-takers (consumer goods companies), and the banks' financing of palm oil concessions, have begun to have an impact. Through various certification schemes such as the Roundtable on Sustainable Palm Oil, or sourcing policies such as No Deforestation, No Peat, No Exploitation (NDPE)--both likely aided by historically low palm oil prices (chart 4)--it seems that land expansion pressure in Indonesia, and the most recent palm-oil-linked deforestation, has largely abated.

Companies and palm oil traders are now starting to focus on how to recover and restore degraded lands in their historic supply chains. Such actions--to compensate for past deforestation--are an emerging trend in the NDPE market, as investors and nongovernmental organisations (NGOs) increasingly see deforestation policies as not going far enough. Innovative financial tools, such as Lestari Capital’s Sustainable Commodities Conservation Mechanism, may enable palm-oil-reliant companies to meet their commitments on restoration and, as such, could prove instrumental in this latest iteration of supply chain management.

There Are Key Lessons To Learn From Palm Oil

Palm oil, although not perfect, is more advanced in terms of sustainability than other deforestation-causing soft commodities. The palm oil story offers four key lessons that could help arrest global deforestation.

The first is about developing robust monitoring. Understanding where deforestation risk is greatest in the supply chain will enable companies further up the chain to target the root cause of the problem.

The second lesson is to decommodify commodities. Supporting smallholder farmers by paying not only for the crop, but also for the ecosystem services provided by intact vegetation, will empower communities to protect nature.

The third is to agree on standards. Because of the mass adoption of NDPE sourcing policies among consumer goods companies and traders, an estimated 28% of the land conceded for palm oil plantations in Indonesia is now not viable for palm oil development. NDPE's stringency means that some NGOs now view these lands as potential stranded assets.

The fourth lesson is to make use of degraded land. More efficient agricultural practices can permit greater yields from already-cleared lands. Such efforts are already being promoted in the Cerrado for soy cultivation, where it is estimated that 18 million hectares of degraded pasture could be made available.

Finally, disclosure is something that can be applied to all soft commodities and the companies that rely on them. For investors, understanding which companies are proactive in addressing deforestation can allow for prudent and effective allocation of capital, and will come more into focus with the Taskforce on Nature-related Financial Disclosures.

Conclusion

Biodiversity and natural capital are arguably garnering more attention now than ever, and the imperative to act has never been more urgent. The effects of climate change will likely make the risks of biodiversity loss even more immediate and dramatic, with scientists estimating that under a business-as-usual warming scenario of 4.3°C above pre-industrial temperatures, the extinction rate could be as high as one in six species. The political will to protect biodiversity is growing, and the next UN Conference of the Parties to the Convention on Biological Diversity in China this October could be a turning point in our approach to biodiversity protection. Equally, companies with exposure to deforestation risks in their supply chains are increasingly aware of the reputational and financial risks of inaction. Robust supply-chain monitoring of soft commodities is now increasingly seen as a quick route to success. However, any meaningful halting or reversal of biodiversity loss will need us to completely reassess our interactions with nature. Reconfiguring our connection to the natural world--if the pandemic has taught us anything--is an urgent next step we cannot ignore.

The authors would like to acknowledge the contributions of Ronni Anand and Charlotte Toon of Moorgate Finn Partners to this research.

Content Type

Theme

Location

Segment

Language