S&P Dow Jones Indices — 2 Jun, 2020

Big Sector Shifts in Low Volatility Composition

By Fei Mei Chan

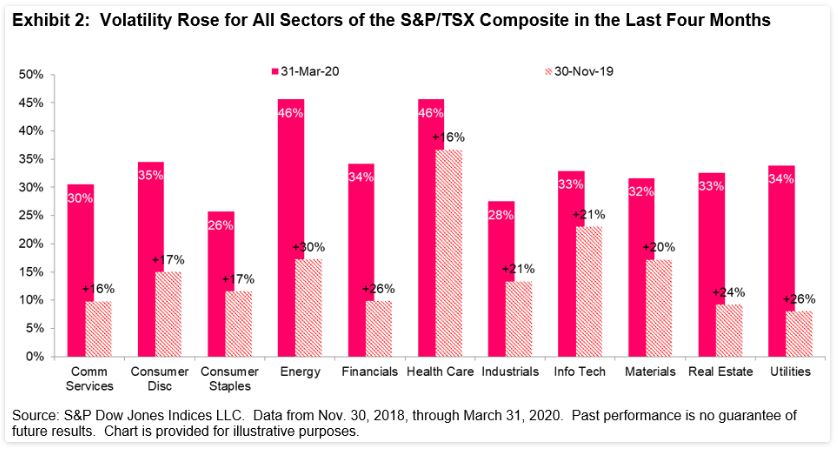

In March, COVID-19 inspired volatility roiled markets across the globe. Similarly, the volatility of the S&P/TSX Composite also jumped. The increase, however, was not balanced across all sectors. We see this manifested in the most recent rebalance for the S&P/TSX Composite Low Volatility Index.

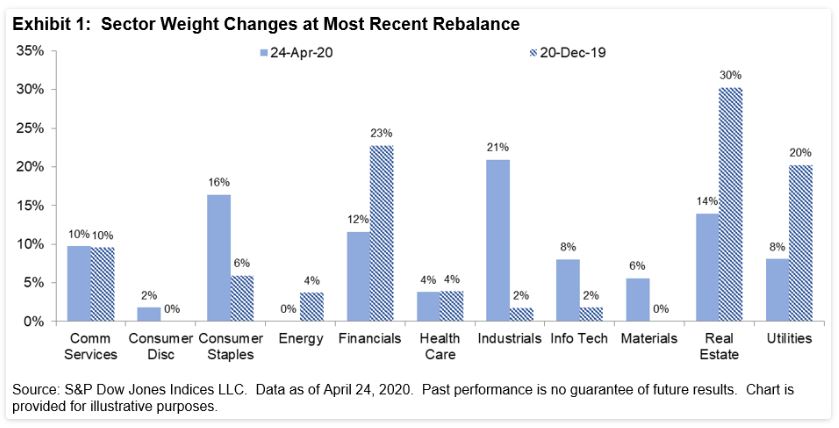

Effective after the close of trading April 24, 2020, Exhibit 1 reflects the sector allocation of the low volatility index. Thirty of the 50 names were replaced in the index, for a weight change of 56%. (For context, median annual turnover for the index is 60%.) Needless, to say this reflects a quarter of major commotion.

Notably, we saw a significant scaling back of Real Estate (-16%), Utilities (-12%), and Financials (-11%). In their place, Industrials (+19%) and Consumer Staples (+10%) rose as the two highest allocations of the index.

S&P DJI’s low volatility methodology does not apply constraints around sector allocations. Though the low volatility index searches for the lowest volatility at the stock level, sector allocations (as shown in Exhibit 2) can sometimes offer context around where things are relatively more stable. Not surprisingly, Energy, Utilities, and Financials experienced the biggest spikes in volatility, and all are on the higher end of the volatility spectrum while Consumer Staples and Industrials are relatively less volatile.

Content Type

Theme

Location

Language