S&P Global — 10 Mar, 2022 — Global

Daily Update: March 10, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

With roughly one week until the U.S. Federal Reserve is expected to announce its first interest rate increase in years, markets will be watching to see how the economic consequences of Russia’s invasion of Ukraine and increasing inflationary pressures affect the central bank’s monetary policy changes.

Markets are confident that the Fed will begin its policy changes at its next Federal Open Market Committee meeting, on March 15-16. S&P Global Ratings expects six rate hikes of 25 basis points each in 2022, with the first almost certainly coming next week, followed by five more hikes in 2023-2024. But persistently high inflation shows no signs of abating. In February, inflation roared year-over-year to a new four-decade high of 7.9%, according to the latest Consumer Price Index reading from the U.S. Bureau of Labor Statistics, released today. Russia’s invasion of Ukraine and the resulting increases in energy prices and prolonged supply chain disruptions are expected to ignite inflation further.

"Inflationary pressures in the U.S. economy are already intense and in the near term are likely to get even stronger," James Knightley, chief international economist at the financial services firm ING, told S&P Global Market Intelligence. "It may not be until 2023 that we see inflation readings declining back toward the 2% target.”

The U.S. economy’s improving COVID health situation could support strong economic conditions for this year, but the implications of the Russia-Ukraine conflict may add uncertainty to the outlook. S&P Global Ratings now projects that U.S. economic growth could come in 70 basis points lower, at 3.2%, this year, driven by policy developments and higher energy prices and limited effects from slower Russian growth. Notably, inflation could jump to 6% by year-end.

“How high the Fed policy rocket will fly depends on inflation dynamics and the economic fallout from the Russian-Ukraine arms conflict, with a 50 basis-point (bp) rate hike off the table in March,” S&P Global Ratings Chief U.S. Economist Beth Ann Bovino said in a March 4 report. “Still, based on a strong job market and soaring prices, it’s virtually assured that the Fed will ‘lift off’ in March with a 25 bp hike. This will be the first interest rate hike since 2018 and the first of up to six rate hikes that we see for this year.”

“We're now forecasting the U.S. Federal Reserve will start normalizing monetary policy sooner and faster than originally expected. This reflects higher and more persistent inflation than previously forecast, with a larger demand-driven component requiring a policy response,” S&P Global Ratings Chief Global Economist Paul Gruenwald said in an abbreviated global macroeconomic forecast on March 8. “The Fed’s tapering of asset purchases has ended, and we expect an announcement on the strategy around reductions in the size of the balance sheet later this year.”

Energy and commodity markets have been particularly affected by Western sanctions against Russia. Already-elevated prices have skyrocketed and are expected to continue to rise. Benchmark oil prices hit a 14-year high this week, soaring on March 7 above $130 per barrel on the ICE Brent crude futures contract, according to S&P Global Commodity Insights. Some market participants have warned oil prices could surge to $175 per barrel if the Russia-Ukraine conflict continues to affect the global economy due to one of the largest energy supply shocks in history, while Russia threatened that the sanctions could force oil prices to top $300 per barrel. S&P Global Ratings believe prices will remain elevated in the near-term as the Russia-Ukraine conflict remains the biggest risk to oil and gas prices.

Fed Chairman Jerome Powell told the U.S. Senate Banking Committee on March 3 that every $10 increase in the price of a barrel of oil generally results in an increase in inflation of 20 bps, according to S&P Global Market Intelligence.

The U.S. yield curve has continued to flatten ahead of the Fed’s upcoming meeting. The spread between two-year and 10-year Treasury yields has narrowed from 160 bps in March last year to just over 20 bps as of March 8, and spreads this low are often seen as an indicator of recessions, according to S&P Dow Jones Indices.

“Although higher rates are generally seen as negative for risk assets, the initial stages of a monetary tightening cycle have not been disastrous for the U.S. stock market historically. However, while the overall market may muddle through just fine, the same may not be true for the different sectors and factors that compose a broad benchmark like the S&P 500,” Benedek Vörös, director of index investment strategy at S&P Dow Jones Indices, said in a March 8 commentary. “The overall takeaway from our analysis is that for both sectors and factors, the fact of a rate hike often played second fiddle to exogenous forces, such as a speculative bubble in dot-com stocks. While the Federal Open Market Committee’s activities are no doubt of importance to the relative returns of factors and sectors, an excessive focus on monetary policy at the expense of the broader economic and market environment could lead market participants astray when appraising prospects for the year ahead.”

Today is Thursday, March 10, 2022, and here is today’s essential intelligence.

Written by Molly Mintz.

Economy

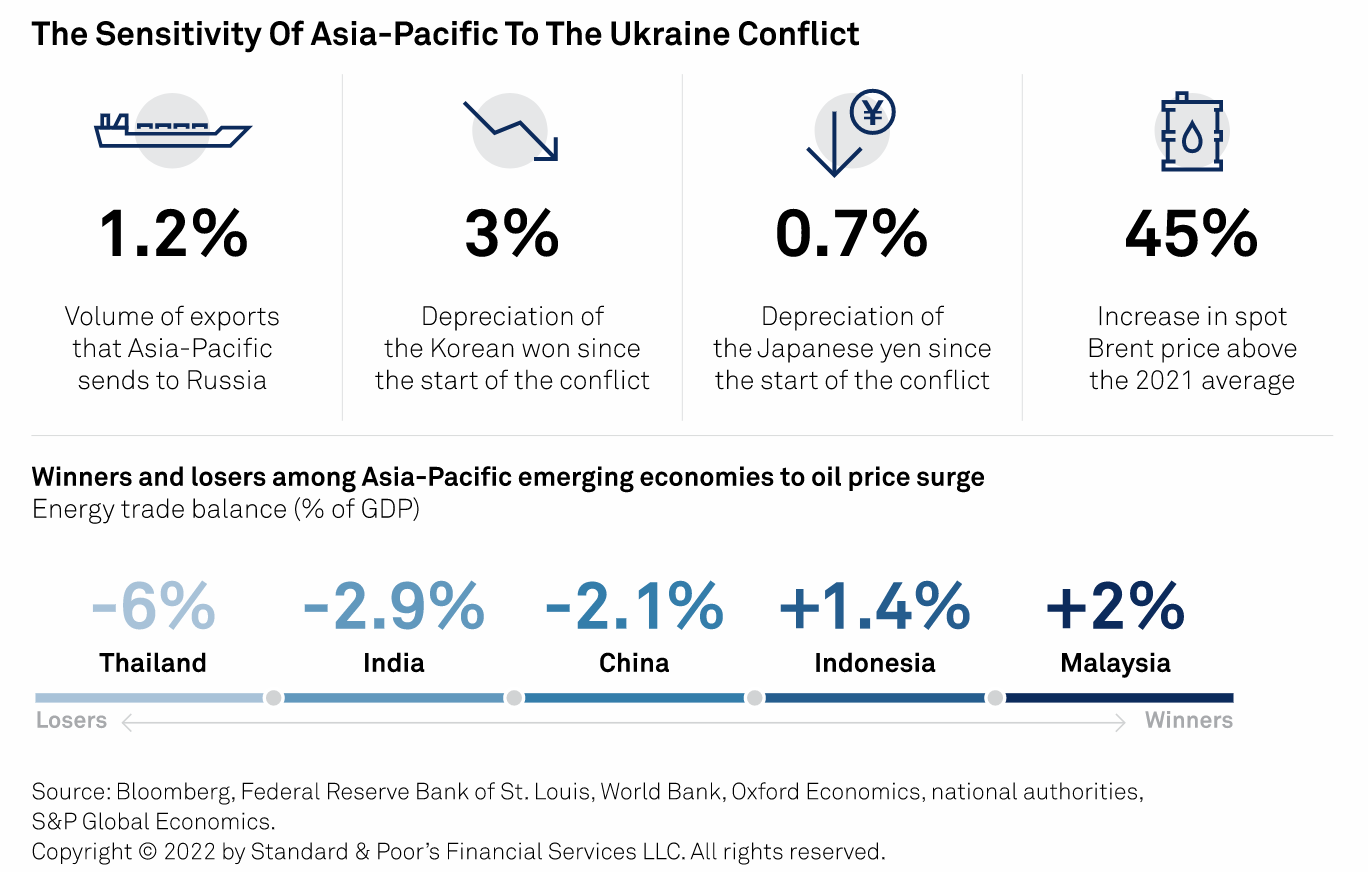

Ukraine Conflict Divides Asia's Energy Haves And Have-Nots

The fast-moving events of the Russia-Ukraine conflict are splitting Asia by energy haves and have-nots, havens and non-havens. The most obvious effect lies in surging oil prices. This divides those nations that export oil and coal, and those that rely heavily on energy imports. S&P Global Ratings also believes that heightened market risk could pull capital out of Asia's emerging markets, hitting currencies, and raising funding costs. The bigger economies are drawing investors seeking safety, as reflected in the stability of the yen and renminbi compared with the euro.

—Read the full report from S&P Global Ratings

Access more insights on the global economy >

Capital Markets

Banks Confront Possible Loss Of Russia Businesses Amid Ukraine Crisis

Foreign banks with operations in Russia are weighing the prospect of losing their investments in the country as international tensions build following Russia's invasion of Ukraine. French banking group Société Générale SA, Austria's Raiffeisen Bank International AG, and Hungary-based OTP Bank Nyrt., which have some of the largest exposures to Russia among nondomestic lenders, moved in recent days to assure investors and analysts that they could absorb the potential loss of their Russian units without any significant threat to their financial stability.

—Read the full article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

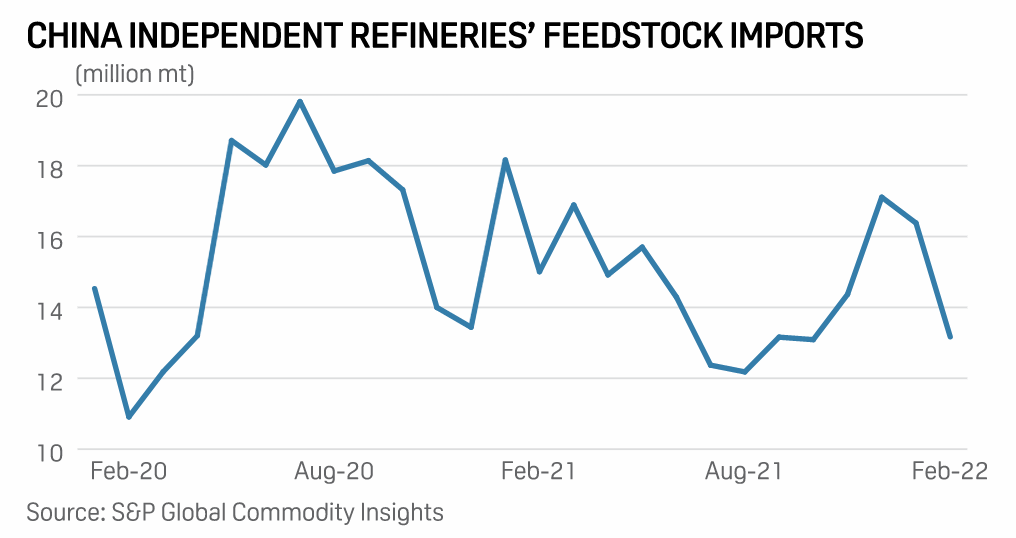

China Data: Independent Refineries' Feedstock Imports Fall 20% On Month In Feb

The feedstock imports for China's independent refineries fell by 19.6% on the month to a four-month low of 13.17 million mt in February, latest data compiled by S&P Global Commodity Insights showed on March 9. Feedstock imports included crude, bitumen blend, and fuel oil. Pure crude imports, which utilize crude import quotas, fell by 26.1% from January to a six-month low of 11.3 million mt in February, the data showed. The lower imports in February were largely in line with market participants' expectation. The independent refineries—mostly Shandong-based—cut throughputs amid the Lunar New Year and the Winter Olympics in Beijing, all of which fell in February.

—Read the full article from S&P Global Commodity Insights

Access more insights on global trade >

ESG

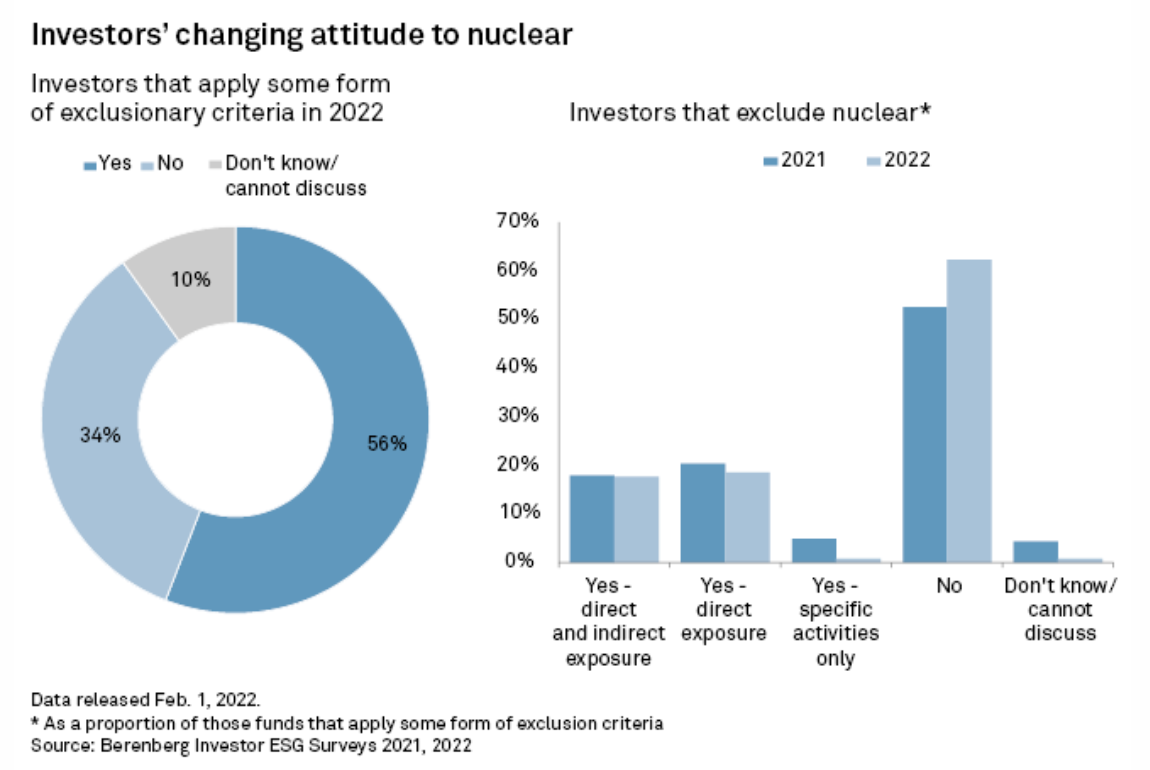

ESG Investors Warm To Nuclear Power After EU Green Label Award

Europe's ethical investors may soften their attitude toward nuclear power after the carbon-free technology won EU recognition as a sustainable activity. Nuclear will join the EU's green taxonomy next year, potentially easing investor concerns about whether it should be considered environmentally friendly. The move could in turn open new funding sources for European nuclear operators, such as Electricité de France SA, or EDF, and Fortum Oyj, as the industry faces up to €550 billion of investment needs through 2050, based on EU forecasts.

—Read the full article from S&P Global Market Intelligence

Energy & Commodities

OPEC+ Posts Biggest Output Gain In 7 Months, Still Misses Targets: S&P Global Survey

OPEC and its allies posted their highest monthly crude oil output increase in February since July 2021, but the 19 members with quotas still fell 764,000 b/d short of their collective targets, according to the latest S&P Global Commodity Insight survey. OPEC's 13 countries raised output by 480,000 b/d from January, pumping 28.67 million b/d of crude, while their nine non-OPEC partners, led by Russia, produced 14.07 million b/d, up 80,000 b/d, the survey found, with many members recovering from disruptions and technical problems.

—Read the full article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

Google May Spur Cloud Cybersecurity M&A With $5.4B Mandiant Buy

Google LLC's proposed acquisition of a cyber defense services provider may spur a further surge of M&A activity in the cloud cybersecurity sector. The Alphabet Inc. unit on March 8 agreed to acquire cybersecurity company Mandiant Inc. for $23 per share. The all-cash transaction is worth about $5.4 billion, inclusive of Mandiant's net cash, with a gross transaction value of about $7.3 billion. Google hopes the Mandiant deal, expected to close later this year, will enhance the range of security operations and advisory services offered by Google Cloud, which remains a key market player amid a robust demand for cloud services.

—Read the full article from S&P Global Market Intelligence