02 Dec 2021 | 09:49 UTC

Russia, OPEC+ seen moving closer on fiscal breakeven oil prices

Highlights

Increase in oil output would require drilling investment

Russia has pushed for increase to output quota in past

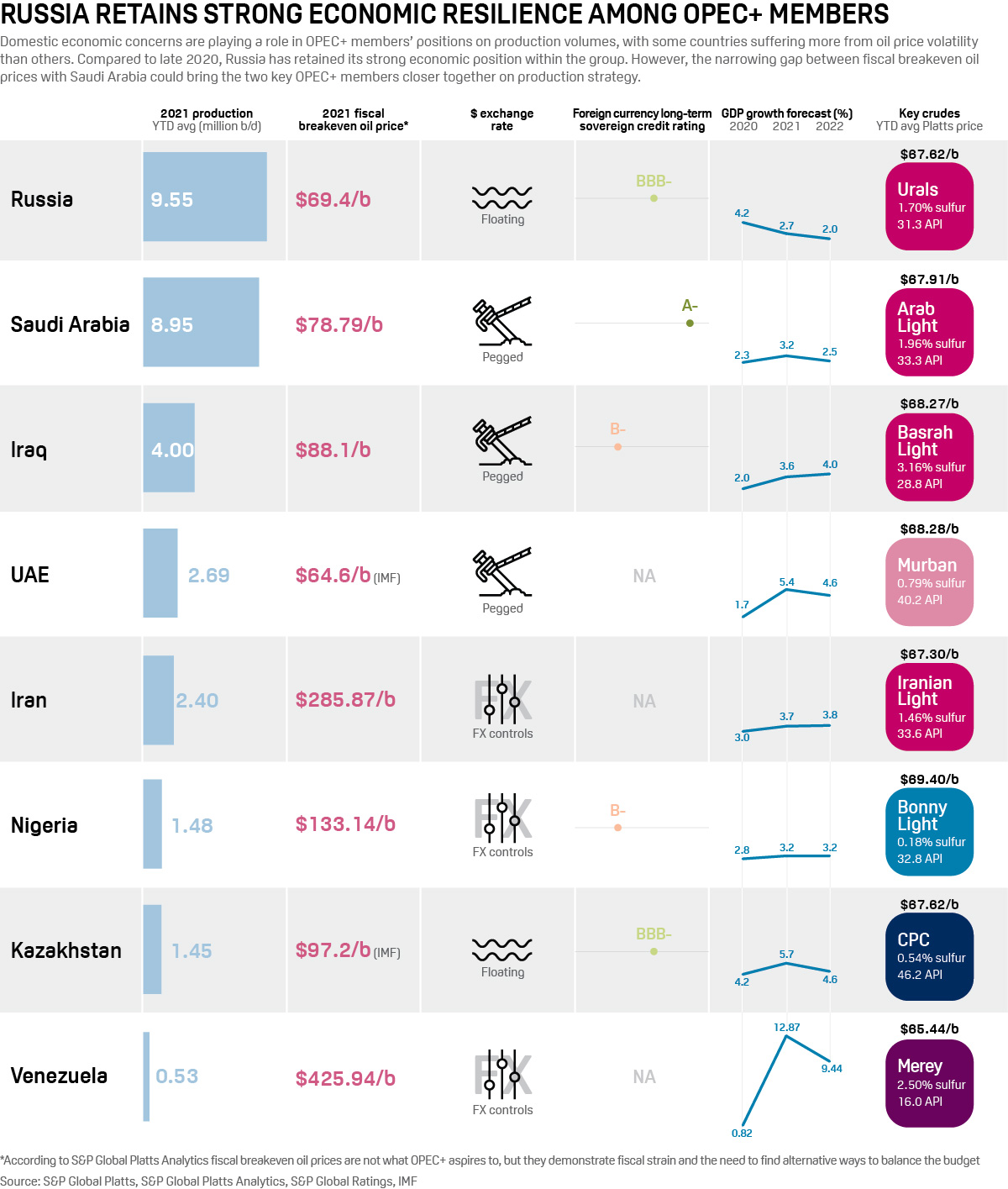

Gap narrows between Russian, Saudi Arabian breakeven oil prices

Lower fiscal breakeven oil prices may help Russia and OPEC's core Persian Gulf producers align their production policy in 2022 despite lingering concerns in Moscow about the demand outlook and availability of spare capacity, according to analysts.

S&P Global Platts Analytics estimates Saudi Arabia's fiscal breakeven price at $79/b Brent in 2021, down from $87/b in 2020. It estimates Russia's breakeven price at $69/b Brent for 2021, also down from $76/b in 2020, but well above the prepandemic average of $52/b in 2018-19.

"The narrowing of the two OPEC+ leaders' respective fiscal requirements likely portends greater cohesion on production strategy than would have been the case even in 2019, when the gap exceeded $30/b," said Paul Sheldon, chief geopolitical adviser for Platts Analytics.

Click here to see the full-sized infographic

S&P Global Platts assessed Dated Brent at $70.96/b Nov. 30, down 15% from $83.13/b on Nov. 24 when warnings about the new variant began to emerge. Russia's key crude grade Urals also dropped by 15% during this period to $68.55/b on Nov. 30.

In the past, Russia has frequently pushed for increases to its production quota, and retains a strong economic position within the OPEC+ alliance, making it comparatively resilient to oil price shocks. Russia will discuss production policy as part of the OPEC+ meeting later Dec. 2 amid growing concerns that the spread of the new omicron variant will hit demand in 2022.

SOVA Capital Analyst Mitch Jennings said Russia's and Saudi Arabia's positions on output volumes may be closer at this meeting than previously.

"It could be Russia sides with Saudi Arabia and may want to exercise caution, especially with a potential new strain of COVID-19 as a threat, and with the coordinated release of strategic reserves," he said.

Spare capacity

Russia's shrinking spare production capacity could also be a factor in its position.

"Even before the news of the omicron variant spread, Russia was more likely than not to advocate for a halt to the scheduled output ramp-up. In addition to its relatively more comfortable macroeconomics than for the rest of OPEC+, Russia has been pumping crude at near-full capacity," said George Voloshin, head of the Paris branch of Aperio Intelligence.

Russian production capacity has changed significantly over the last year. Producers have already brought most of their spare capacity back on stream, as OPEC+ quotas increased throughout 2021.

Platts Analytics estimates Russia's sustainable crude production capacity to be around 10.5 million b/d, excluding condensate, which is exempt from OPEC+ quotas. This is 70,000 b/d below April 2020 and 240,000 b/d below the December 2018 all-time high. Platts recorded Russia's crude production at 9.96 million b/d in October.

In recent conference calls, two of Russia's biggest crude producers Rosneft and Gazprom Neft said they have largely used up spare capacity while Lukoil has indicated it has around 30,000b/d.

"Getting more oil out of the ground would require drilling new wells, which is problematic in more than one respect," Voloshin said.

Economic factors

Current oil prices remain well above levels included in Russia's state budget. The Kremlin recently approved a budget including price forecasts of $44.20/b in 2022, $45/b In 2023 and $45.90/b in 2024.

"Russia still feels much more comfortable from a macroeconomic perspective than most of its peers within OPEC+. For instance, Russia's 2020 budget deficit amounted to 4% of GDP while in Saudi Arabia, it exceeded 11%," Voloshin said.

A key element in Russia's resilience is the fiscal rule introduced in 2017, which has softened the impact of oil price fluctuations on its economy and budget.

The mechanism uses a baseline oil price assumption. If crude prices are above this level revenues are diverted to the National Wealth Fund, if they are below that level the government can draw from the NWF.

Russia's international reserves were at $626.3 billion on Nov. 19, up from $584.9 billion on Nov. 20, 2020. The NWF has also grown from $167.63 billion on Nov. 1, 2020, to $197.75 billion a year later.

The free-floating currency is also a major stabilizing factor for both the Russian state budget and its oil producers. With costs primarily in rubles and export revenues in dollars, Russian producers can minimize the impact of low oil prices on their operations.

While immediate operational and demand issues may dominate discussions this week, these economic factors are likely to continue to impact the Russian government and oil producers' approach to the OPEC+ agreement.