20 Mar 2023 | 17:03 UTC

Infographic: Bank turmoil hits oil markets but fears of 2008 repeating itself look overdone

Highlights

SVB collapse triggered drop in oil, fears of 2008 crisis

Oil market structure seen different to last crisis

Oil traders and OPEC adopt a wait-and-see approach

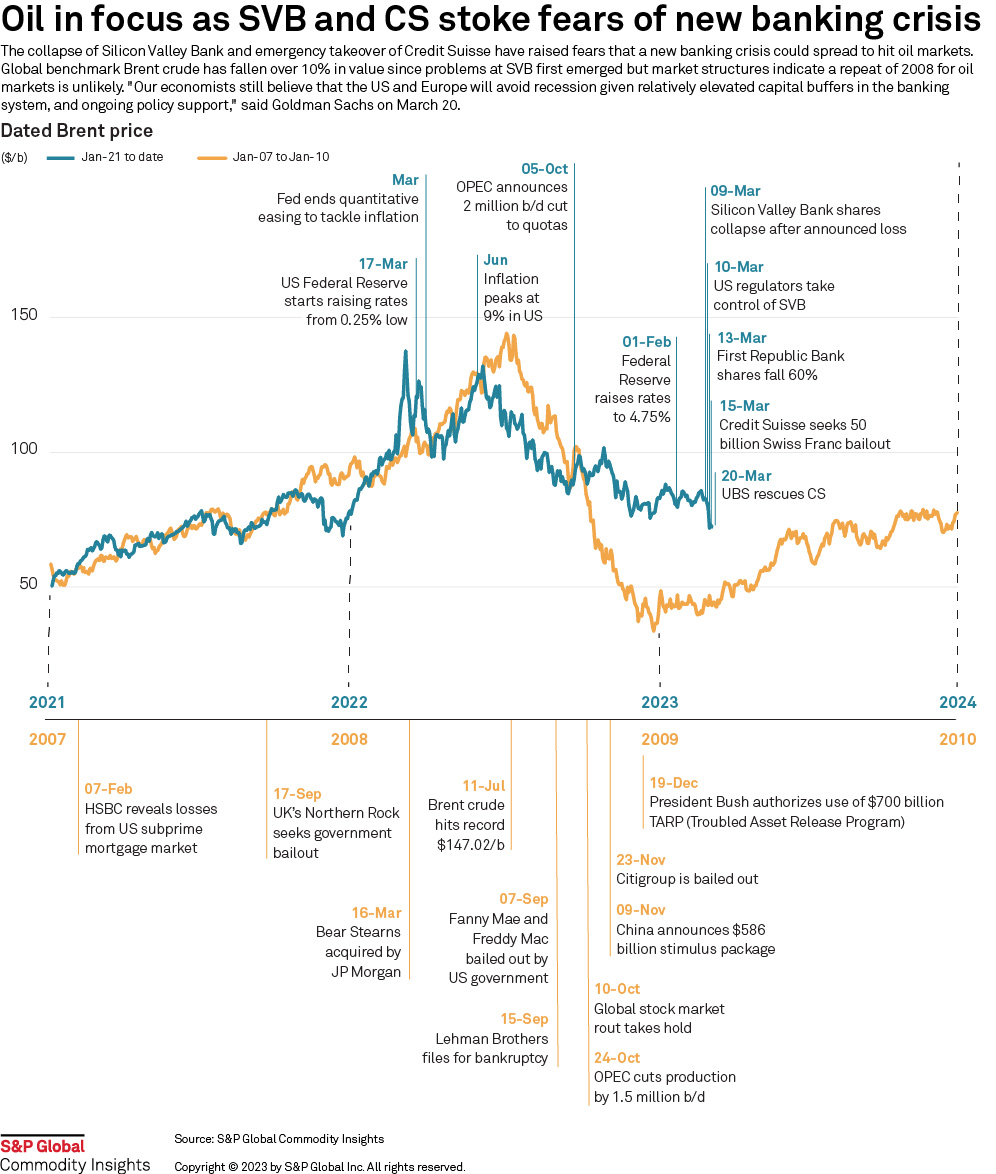

Oil traders were weighing the prospect March 20 of a new global banking crisis similar to 2008 hitting hydrocarbons demand, but a backwardated market structure signals prices could be more resilient to financial turmoil.

The sudden collapse of Silicon Valley Bank in the US and emergency takeover of Credit Suisse with the help of Switzerland's central bank have helped to push crude lower. Platts -- part of S&P Global Commodity Insights -- assessed Dated Brent at $71.705/b on March 20. The measure is down almost 15%, or $11/b, since SVB's shares collapsed after it announced losses on March 9, triggering regulators to seize control a day later.

The sudden fall in oil prices is reminiscent of the events marking the beginning of the last major banking crisis when HSBC in February 2007 unexpectedly revealed losses from the US subprime mortgage market. Eventually the collapse of Wall Street investment banks and an unprecedented $700 billion bailout of banks by the US federal government would trigger a period of extreme volatility in energy markets.

Crude hit a record $147.02/b on July 11, 2008, just months before US mortgage lending giants Freddie Mac and Fannie Mae were bailed out. However, oil traders argue it's too soon to predict the current uncertainty hitting banks turning into an economic contagion on a scale of what was seen in 2008.

"So far it doesn't look like the same kind of situation [as 2008] but we don't know what we don't know," said Trafigura Chief Economist Saad Rahim, speaking at the FT Commodities Global Summit in Lausanne.

Rahim's caution was also shared by Vitol, the world's largest independent oil trader.

"Energy markets remain vulnerable to both economic and geopolitical risks," said Vitol CEO Russell Hardy in a trading update on March 20. "The extreme volatility of energy markets during 2022 highlighted the importance of prudent physical and financial risk management; accordingly, we will continue to manage our business and financial position carefully and conservatively."

Vitol sees oil demand growing by 2 million b/d this year driven thanks to the continued return of China and air transport outweighing any concerns of a full-blown banking crisis. Hardy's cautious optimism is also reflected in market structure.

Backwardated market

"The oil market backdrop to the 2008 financial crisis was vastly different to that of today's financial intrigue," said Joel Hanley, global oil director at S&P Global Commodity Insights. "Crude oil prices had generally been on the rise since the end of the 1990s and this came to a head, fueled by a weak dollar from 2006 onwards, when Brent crude futures rose over $147/b in July 2008."

According to Hanley, market structure in 2008 was in very steep contango, with front-month Brent at deep discounts to the following month, leading to full land storage and hitherto unseen levels of floating storage being used.

"At one point, 22 VLCCs of crude were floating off the UK coast alone, which does not speak of a strong physical market," Hanley said. "The currency and sentiment-led overheating of the commodities markets were not always backed by physical demand, leading to a crash in oil prices of over $100/b before the end of 2008. It was then that OPEC acted to remove barrels from the market and stabilize prices. The current market has a firmer sense of economic growth and demand underpinning it, with supply volatility more likely to cause upside than down."

For others like Goldman Sachs, quick action to limit the fallout from SVB and the underlying strength of economies in major consuming countries will help markets avoid a hard landing.

"Our economists still believe that the US and Europe will avoid recession given relatively elevated capital buffers in the banking system, and ongoing policy support," the bank said in a recent note.

Click to see full-size graphic

OPEC+ monitors

OPEC+ has so far rebuffed any suggestion the current uncertainty concerning banks requires a rethink of its plan from last year to cut 2 million b/d from supply. However, should prices dip below the $70/b threshold it may be forced to act. Crude at these levels would also compromise the effectiveness of price caps imposed by G7 members on Russian oil.

Delegates told S&P Global on March 20 the group, which is due to hold a meeting of its Joint Ministerial Monitoring Committee next month, is likely to wait for more data to emerge before jumping to any conclusion.

In its latest oil market outlook published March 14, just days after the collapse of SVB, the OPEC Secretariat downgraded its estimate of how much crude the producer group would need to pump to balance the market, despite increasing its forecast for Chinese demand.

The call on OPEC crude will average 28.77 million b/d in the first quarter of 2023, dipping to 28.62 million b/d -- below the 28.91 million b/d that the bloc produced in February -- lending support to potential further output cuts, with output from non-OPEC producers expected to rise more than previously thought.

It added that rapidly changing economic conditions continue to warrant a cautious approach to managing oil production volumes.

"Given the ongoing high level of uncertainty with regard to the timing and extent of a full global economic recovery to pre-pandemic levels in all sectors, the OPEC and non-OPEC countries participating in the [Declaration of Cooperation] continue to carefully monitor market developments," the secretariat said.

OPEC has allied with Russia and several other key oil producers on a series of output cuts, the latest of which are scheduled to last through the end of 2023.