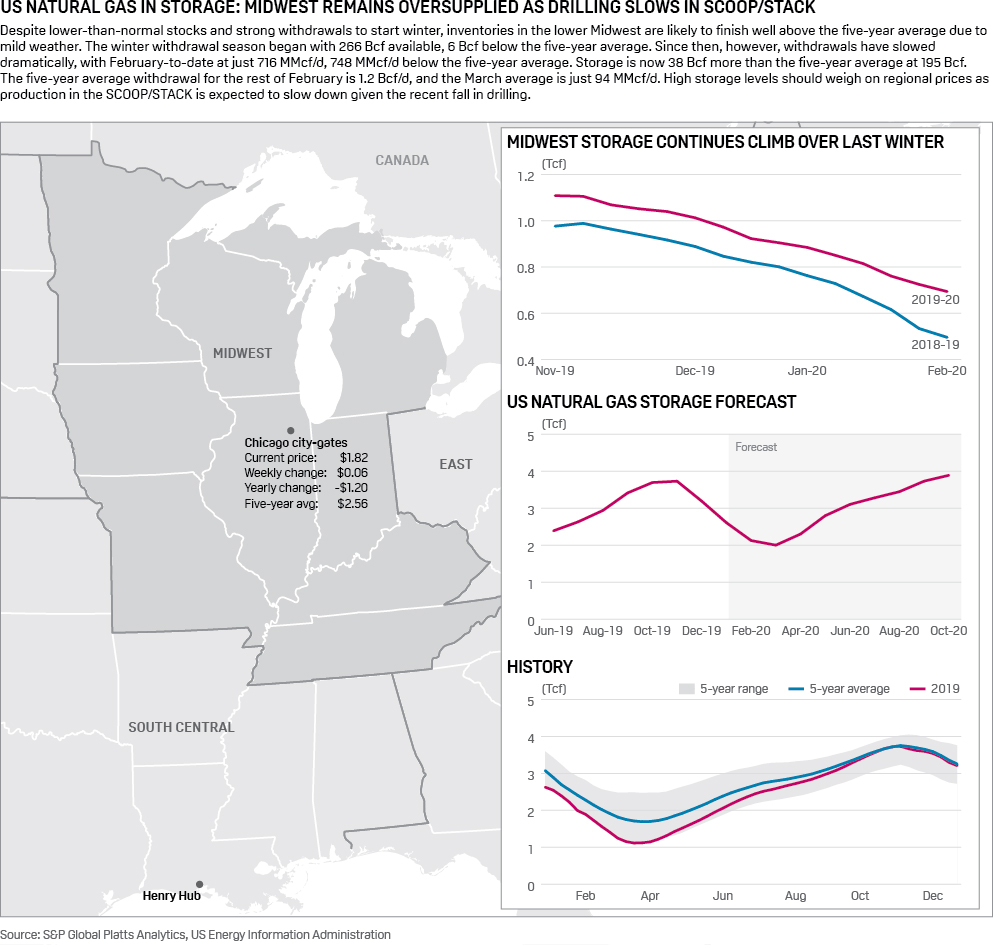

13 Feb 2020 | 19:43 UTC — Denver

US working natural gas in underground storage decreases by 115 Bcf: EIA

Highlights

Inventories 31.7% higher year on year

Stocks 9.4% above five-year average

Denver — US working natural gas storage inventories fell by 115 Bcf to 2.494 Tcf for the week ended February 7, which was slightly more than the market expected, the Energy Information Administration data showed Thursday morning.

However, Henry Hub futures still fell slightly following the release of the data.

The pull was more than an S&P Global Platts' survey of analysts calling for a 108 Bcf withdrawal. It was also more than the 101 Bcf pull reported during the corresponding week in 2019 but less than the five-year average draw of 131 Bcf, according to EIA data.

Massive storage volumes now tower 601 Bcf, or 31.7%, more than the year-ago level of 1.893 Tcf and 215 Bcf, or 9.4%, more than the five-year average of 2.279 Tcf.

After significant production declines throughout January, Texas production estimates gained 700 MMcf/d week over week, further tipping the US balance towards the supply side, according to S&P Global Platts Analytics. The lack of significant heating demand in 2020 so far has built up a sturdy inventory surplus which will be hard to chip away at during the shoulder season, extending the current bearish risks at least until power burn can ramp up during peak summer demand days.

The NYMEX Henry Hub March contract was static at $1.84/MMBtu during trades following the weekly storage report, slightly recovering in the past two days after hitting a nearly four-year low for prompt month gas on Monday when it settled at $1.77. The forward curve continues to price successively higher each month over the next year, reaching $2.58 by January, before falling slightly in February.

Expectations for a possible production pullback in the face of such low prices may not materialize in the near term, at least based on early production guidance that has started to roll in from leading US producers. Despite huge cuts to spending, producers are still targeting modest production growth in 2020 compared with 2019 levels, which may look more like a flattening-out due to the steady gains that accrued in the second half of last year.

With this persistent amount of supply seemingly locked in, demand is more important than ever in keeping the market in balance. However, the warmer-than-normal winter has put inventories above normal levels and set the market on course for a possible bearish summer ahead.

A forecast by Platts Analytics' supply and demand model expects a 118 Bcf draw for the week ending February 14, which is 18 Bcf below the five-year average.

For the week in progress, demand is expected to have increased by 6.3 Bcf/d as supplies also grew by more about 1 Bcf/d. The demand gains have been fairly equally distributed across the Northeast, Midwest and Southeast regions. Upstream, total supplies are averaging 97.8 Bcf/d, with Texas production gains once again driving the majority of the overall supply increase.

Click here for full-size infographic

{kind=link}