24 Sep 2020 | 12:10 UTC — Insight Blog

After Hin Leong: collapse of a Singaporean oil prodigy

By Eric Yep

The Hin Leong scandal rocked the Singapore trading community earlier this year, topping many earlier bankruptcies in the commodities space in terms of financial losses. As the dust settles, Eric Yep unpicks the company’s path to self-destruction and assesses the fallout.

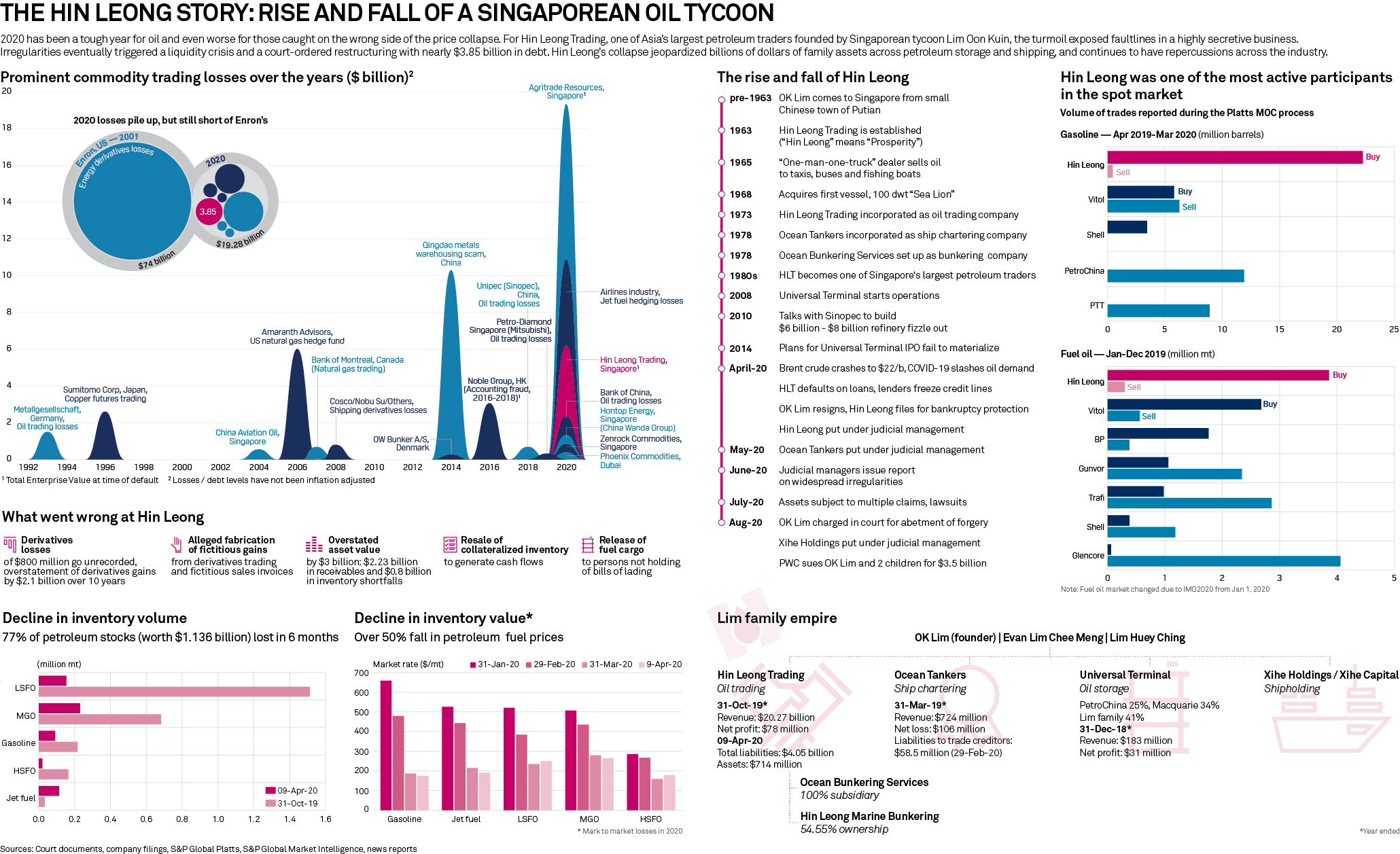

Hin Leong’s bankruptcy filing, on April 17, marked one of the world’s largest collapses of an oil trading firm. The story of the Singaporean company and its founder, Oon Kuin Lim, is inextricably linked with the history of the petroleum trade in Singapore and the Asia-Pacific region.

Oon Kuin Lim, more popularly known as OK Lim in industry circles, started his oil distribution business around 1965, the same year that Singapore separated from Malaysia to chart its own future, after several years of political differences.

In his first affidavit to a Singaporean court in April, OK Lim said he was a “one-man-one-truck” oil dealer, selling oil bought wholesale from the oil majors to taxi companies, bus companies, and fishing boat operators as the tiny Southeast Asian country built its economy.

OK Lim, born in China’s Fujian province, built his fleet of tank-trucks in Singapore over the years and incorporated Hin Leong in 1973 as an oil trading company, followed by Ocean Tankers in 1978 as a ship chartering and management company. He started the Universal Terminal tank farm in 2008.

The early years of Lim’s business were turbulent decades for the oil industry in Singapore, whose iconic downstream refining sector has seen everything from the rise of Asian crude grades such as China’s Shengli and Malaysia’s Tapis to the rise of US shale. The city state even helped fuel the Vietnam War at one point.

By virtue of being at the heart of Asia’s fuel supply chains, Singapore has also been home to the quintessential oil trader who arbitraged between prices, regions, fuel quality and geopolitics to profit from a barrel of oil. It was briefly the stomping ground of Glencore founder and legendary commodities trader Marc Rich, who, like OK Lim, had an immigrant rags-toriches story of his own in the US.

It is not so extraordinary, then, that OK Lim grew his fortunes in Singapore, eventually becoming one of the largest traders of petroleum products in the region and a regular on the Forbes list of Singapore’s richest people. Hin Leong’s bunkering arm was Singapore’s third largest bunker supplier in 2019, accounting for 10% of local bunker sales, and was a key supplier to countries like Indonesia and Myanmar in Southeast Asia.

Anatomy of a decline

When Hin Leong’s troubles became public it was the equivalent to the collapse of an institution, shaking Singapore’s commodity trading community to the core, not only those who had exposure to the company but also everyday traders who had dealt with OK Lim for decades.

In mid-August 2020, OK Lim was charged in Singapore’s court with abetment of forgery for the purpose of cheating, after investigations by the Commercial Affairs Department into Hin Leong’s business activities.

Click for full-size infographic

According to the charges, OK Lim had instigated a Hin Leong employee to forge a document that looked like it was issued by UT Singapore Services, which operates the Lim family’s Universal Terminal tank farm, stating that Hin Leong had transferred more than 1 million barrels of gasoil to China Aviation Oil (Singapore).

The forged document was used to secure more than $56 million in trade financing from a financial institution, Singapore Police said when the charges were made public, adding that investigations were ongoing into other offences possibly committed by OK Lim.

Two weeks later, PricewaterhouseCoopers (PwC) Advisory Services, the judicial manager for petroleum trader Hin Leong Trading, sued OK Lim and his two children for $3.5 billion. The sum represented Hin Leong’s outstanding debts, according to a statement from Drew & Napier, the law firm representing Hin Leong Trading, as instructed by PwC.

PwC also sought to recover another $90 million in dividends that the Lim family, which includes his two children, Evan Lim Chee Meng and Lim Huey Ching, paid themselves in previous years out of Hin Leong’s disputed profits, it said.

Interim judicial managers had laid out the scale of “irregularities” at Hin Leong in detail in June, in an interim report seen by S&P Global Platts, covering everything from the fabrication of documents to derivatives trading losses and accounting cover-ups.

“The scale of the irregularities uncovered in just the financial year ended 31 October 2019 alone is highly troubling, and suggests that the company had, possibly for many years, been carrying on its business by presenting a picture of financial health that was a far cry from the underlying reality,” the report said.

The report went on to say that financial statements for the year ended 31 October 2019 grossly overstated the value of assets by “an astonishing amount of at least $3 billion” comprising $2.23 billion in accounts receivables which had no prospect of recovery and $0.8 billion in inventory shortfalls.

“The overstatement existed to conceal significant losses that the Company had accumulated over the years,” according to the report.

The investigators said there was evidence of accumulated derivatives trading losses of about $808 million over the past 10 years, in line with OK Lim’s own affidavit, but added that these losses were concealed through the overstatement of derivatives gains by as much as $2.1 billion over the same period.

They said receivables were overstated through the manipulation of accounting entries, and the use of “control accounts” to make inter-bank transfers that gave the false impression of payments, when none were actually received from customers.

The bank transfers were facilitated by using “fabricated documents on a massive scale” and the scale and regularity of the fabrication suggested that “the practice was routine and pervasive,” the report said. These included forged bank remittance advices, bank statements, bills of lading, sales contracts, sales invoices, swap trade confirmations, swap trade tickets, deal settlement slips and inter-tank transfer certificates.

The forged documents in turn misled banks into extending financing to the company and also acted as supporting documentation for fictitious gains or profits, the IJMs said. To keep the losses concealed, Hin Leong had to maintain the flow of liquidity for which it obtained financing from banks through schemes that involved the sale and repurchase of cargo at a loss, forged documents, non-existent inventory, or the sale of the same inventory to multiple parties; leading to competing legal claims on the same cargo.

“The cumulative effect of the above irregularities was that a vastly misleading picture of the Company’s financial health was presented to external parties, possibly for many years, with the result that the Company was able to continue to trade and obtain financing,” the IJMs concluded. Not only had Hin Leong been unprofitable in the last few years but its total liabilities at the time of the report came to $3.5 billion while its assets were only $257 million, the report said.

On June 25, the Lim family issued a statement to the press saying they had not been given opportunity to respond to the allegations in the interim report and that OK Lim was deemed medically unfit to work at the time the investigations were being conducted. They said they reserved their rights against all relevant persons and would address the report and its findings in the right fora.

They had not issued a public statement on either the charges or the lawsuit as of early September.

Business as usual?

The Hin Leong episode has raised pertinent questions for the trading industry and everyone that deals with it, even as casualties from this year’s disruptions are still piling up, such as Zenrock Commodities Trading and Hontop Energy.

HSBC in May filed an application in Singapore’s High Court to put Zenrock Commodities under judicial management, citing “suspicious” transactions and trade practices in its affidavit. Hontop filed for debt restructuring with the High Court in March.

Hin Leong’s alleged fraudulent actions were discovered only when the coronavirus pandemic stressed out already overextended credit lines used to cover the company’s losses. When Brent crude sank below $30/b in March it was the proverbial straw that broke the camel’s back. The trader defaulted on some payments, which is when the real scrutiny into its transactions began.

If the coronavirus pandemic had not happened, how much longer could Hin Leong have continued? How widespread is the scale of losses at trading houses this year? What if the contango trade, which helped trading desks boost their profits and recoup losses in the second quarter, had failed?

Most large private commodity trading houses remain relatively opaque, even as they replace oil majors in remote countries with unstable governments, to the extent of financing the extraction of natural resources. Traders, including Hin Leong, prefer to control all aspects of the supply chain including shipping and storage to gain that extra optionality for the marginal profit on a barrel.

New light has been thrown on lax industry practices on payment and collateral, such as the use of letters of indemnity in place of bills of lading, which carry the actual title to a cargo, for payment. LOIs were devised as a solution as the original bills of lading are often not available, especially when a cargo passes through many hands in a physical trade. But use of LOIs carries risks that are not always properly accounted for. Traders are more cautious now, but it remains to be seen whether industry practices will change permanently.

The current crisis has also exposed the true valuations of petroleum assets in the midst of a crisis as oil majors write-off billions of dollars in reserves and projects. The Lim family’s shipping and storage assets – Ocean Tankers and Universal Terminal – are likely to be on the chopping block with both the companies now under judicial management.

Ocean Tankers charters or operates Singapore’s largest fleet of tanker vessels and was one of the world’s largest tanker fleet operators with over 150 vessels, according to OK Lim’s affidavit. Its total exposure to Hin Leong’s trades was $2.67 billion. Universal Terminal, 41% owned by the Lim Family, is the largest independent petroleum storage complex in Singapore and one of largest tank farms in the world with 2.23 million cu m of storage capacity.

Market participants say that storage assets are worth more in this crisis, but shipping assets and shipping company stocks have seen their value slashed.

Lastly, there is the question of regulation and risk management in the industry. Banks have scaled back significantly from lending to the commodities sector in 2020, a move accelerated by incidents like Hin Leong.

Risk management divisions are working overtime to scrutinize trades, and Singapore has deployed data-crunching technologies to assist investigators in the Hin Leong case and other fraud cases such as Wirecard earlier this year, and the 1MDB scandal several years ago.

Tighter measures are expected by the industry in coming months, although it is unclear what form they will take. As commodity trading itself gets digitized, the types of “old-school” Ponzi schemes and fraud we are seeing alleged here would no longer be possible. But that does not necessarily mean the renegade trader will disappear.

Marc Rich, in his biography ‘The King of Oil’ said the US shoots small birds with big cannons, referring to his indictment by the US government for trading Iranian crude amid sanctions. In the aftermath of the Hin Leong bankruptcy, it remains to be seen whether the big guns will be brought out.