Apr 23, 2024

Can Var Energi's Venus HIW bring further exploration opportunities in the immature West Barents Shelf Edge?

By Alex Wyer, Rebecca Vyse, and Yulia Khorikova

After a nearly 7-year hiatus, the Bjornoya Sub-basin of the West Barents Shelf Edge will soon welcome a fresh addition to its deepwater inventory of wells. Var Energi's new-field wildcat 7219/6-1 is scheduled for spudding in April 2024. Targeting the promising Venus prospect in the operator's PL 1025 S, the well will be drilled in a water depth of 399 meters by the "Transocean Enabler" semi-submersible. Var Energi ASA assumes the lead role with a majority interest of 60%, while Equinor Energy AS and Petoro AS each hold a 20% stake.

The immature West Barents Shelf Edge, which lies to the west of the highly prospective and similarly immature Barents Sea Platform, had 2 gas discoveries made in 2014: 7319/12-1 (Pingvin) in open marine sandstones of the Upper Cretaceous Kveite Formation; and 7220/2-1 (Isfjell) in the shallow marine sandstones of the Upper Triassic to Middle Jurassic Realgrunnen Group. Notably, the last wildcat, 7318/12-2, drilled in 2017 by Eni Norge AS which targeted the Bone prospect, encountered approximately 60 meters of tight sandstone in the primary target, the Realgrunnen Group, although it proved to be water-bearing.

The Venus prospect, targeting the Paleogene (Eocene/Oligocene) Torsk Formation, is a compelling exploration opportunity and success would signify the inception of a new play in the region. The operator has identified two reservoirs within the prospect: an upper reservoir situated at 1,458 meters (with a thickness of 25 meters) and a lower reservoir positioned at 1,583 meters (with a thickness of 35 meters). The estimated potential recoverable resources stand at 353 MMboe, encompassing both oil and gas. With a planned total depth of 1,672 meters, the drilling operations, which include a potential side track, are expected to last up to 45 days. Notably, the prospect is located approximately 28 kilometers northwest of the Johan Castberg field which has oil and gas-bearing sandstones in the Realgrunnen Group.

The Torsk Formation, discovered as a reservoir in 1992 in the Vestbakken Volcanic Province, is historically significant. Well 7316/5-1 found gas-bearing sandstones at 1,340.0 to 1,358.5 meters, with a net pay of 9.75 meters and porosity and water saturation at 28.2% and 35.9%. Another sandstone layer encountered at 1,442 to 1,469 meters was water-bearing, leading to well abandonment. Repsol's well drilled in 2013 on the Darwin prospect located in the Veslemoy High found thin, tight Torsk sandstones with some gas shows. The Torsk Formation is shallower in surrounding wells, typically at 500-700 meters, compared to Venus's reservoir depth.

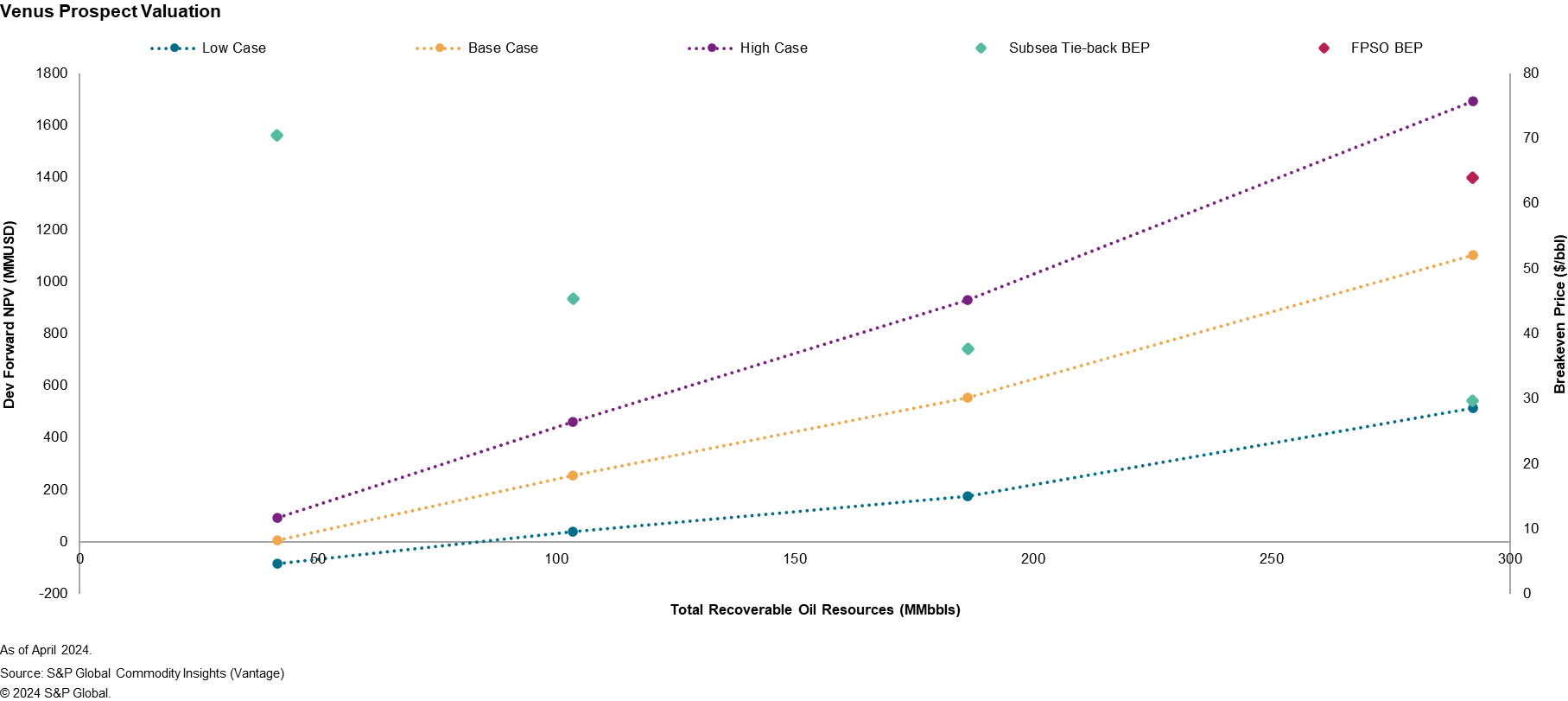

Should the Venus exploration well prove successful, a 28 km subsea tie-back to the Johan Castberg Floating Production Storage and Offloading (FPSO) vessel is the most likely development concept for all resource scenarios, due to its proximity and fast-track development options. Several cluster developments are already planned in the Johan Castberg area, with Venus estimated to be included in Phase 2 which is scheduled to come onstream within the next decade. Whilst Venus is expected to be oil-dominated, it was assumed that any discovered gas would be reinjected into the Johan Castberg reservoirs using its pre-existing gas injection wells due to a lack of gas export solutions in the Barents Sea. For this exercise purpose, a standalone FPSO development solution was also modelled for the high-end resource scenario. However, this option returned a breakeven price (BEP) of over $60/bbl which was double that of the subsea tie-back solution. The higher BEP was primarily driven by the increased capex/opex associated with the FPSO, as well as a longer lead time between a Final Investment Decision (FID) being taken and Venus coming onstream.

At a base case oil price of $75/bbl, the minimum economic field size is estimated to be around 40 MMbbls recoverable, whilst a discovery at the estimated 353 MMboe (reported by Var Energi) is expected to have a Net Present Value (NPV) of around $1.1 billion. A discovery near the midpoint between these two scenarios is expected to return an NPV above $500 million, expected payback within 4 years, and an IRR of 18.7%. The BEP drops significantly between the 50-100 MMbbls resource mark before stabilizing around the $30-$50/bbl out towards the high resource scenario. This is attributed to the fact that all scenarios include the 28 km pipeline costs, with the main increase in capex coming from drilling more production/water injection wells rather than implementing additional export infrastructure.

Should the Venus HIW be a success, it would discover further exploration opportunities within the immature West Barents Shelf Edge basin and further de-risk any prospects targeting the Torsk Formation. Its proximity to the Johan Castberg FPSO provides a clear near-field development opportunity that could extend the peak production rate through the facility until the mid-2030s.

For more information regarding well, field & basin summaries, please refer to EDIN

For more information regarding asset evaluation, portfolio view, and production forecasts, please refer to S&P Global Vantage

For more information regarding our country activity reporting, please refer to our Upstream Intelligence solutions

For more information regarding E&P costs please refer toS&P Global Que$tor

Author of this report:yulia.khorikova@spglobal.com , alexander.wyer@spglobal.com, rebecca.vyse@spglobal.com.

For any additional comments or questions please reach out to yulia.khorikova@spglobal.com

***

This article was published by S&P Global Energy and not by S&P Global Ratings, which is a separately managed division of S&P Global.