Jan 18, 2022

Africa Energy and Economy Review and Outlook (2021-22): A Time of Transition to an Uncertain Destination

By Daniel R. Berkove, Farrah Boularas, Justin Michael Cochrane, Natznet Tesfay, Roderick Bruce, and Silvia Macri

A Time of Transition to an Uncertain Destination

I. Introduction

Buffeted by a historic recession in 2020, Sub-Saharan Africa's energy sector and economy experienced a challenging 2021, exacerbated by COVID-19-related complications. Now the region's economies are rebounding. And spurred by the global energy transition, governments are decarbonizing across the energy value chain. But the size and scale of these economic and energy transitions, both of which are occurring simultaneously, is unprecedented. Moreover, Omicron—and, perhaps later, other COVID-19 variants—is disrupting progress and clouding the future trajectory of initiatives taken today. With the region beset by a multitude of uncertainties, the only thing clear about what these transitions mean for SSA in 2022 is that there is no clear line-of-sight ahead. This blog reviews the progress that was made over the course of the past year, and provides an outlook identifying the complexities and questions the region will face in the coming year.

Join our Africa authors of this blog live in the first of four instalments of IHS Markit's 2022 Africa Energy Outlook series, covering upstream to downstream, as they map the significance of the events of 2021 and explore what's ahead for 2022. Register here

|

Key Implications Economics and Country Risk

Upstream Oil & Gas

Downstream

Power

|

II. Economics and Country Risk

Subdued growth and divergent recovery trajectories through 2022

In 2021, Sub-Saharan African (SSA) economies grew by 3.5%. This rebound from the historic 2020 recession, which saw a -2.3% contraction in the region's economies from 2019 levels, comes on the back of a recovery in global trade, more buoyant commodity prices, debt service suspension initiatives, and a loosening of COVID-19 related restrictions. Yet the rebound lags significantly behind the global rate, which is expected to increase 5.5% this year. This gap between SSA and the world is expected to remain through 2022, albeit shrunk slightly, when SSA's growth rate is expected to remain stable at 3.5% while global growth dips to 4.2%.

In 2022, economic growth across SSA will be uneven and largely dependent on countries' ability to provide vaccines and more effective treatments, adapt businesses, and rebalance consumer spending from goods to services. Most critically for Africa, Mainland China—the region's largest trading partner—is expected to resume a long-term trend of decelerated growth, slowing from 8.1% in 2021 to 5.5% in both 2022 and 2023. Consequently, Chinese appetite to extend loans—China loaned over USD134 billion between 2009-2019 largely to fund major infrastructure projects across the region—has decreased. At the November 2021 triannual Forum for China-Africa Cooperation (FOCAC), China pledged only USD40 billion in funding over three years, a third less than the USD60 billion total pledged at the 2015 and 2018 summits.

Recovery trajectories for the region's economies are expected to diverge in line with their respective economic structures. Large oil exporting economies such as Angola and Nigeria are forecast to grow only by 0.05% and 2.6% respectively, which will significantly weigh down the pace of SSA's overall recovery. The more diversified markets of South Africa, Kenya, and Cote d'Ivoire, however, are expected to grow by 4.7%, 4.0%, and 5.9%. But to maintain in 2022 the 2021 regional growth level of 3.5%, policymakers will have to navigate around a number of major downside risks, including inflation, fiscal constraints and political instability.

Monetary authorities must contend with growing price pressures in the region

In 2021, supply chain disruptions manifested less severely in SSA than they did globally. South Africa was an exception, however, since the country is more integrated into global trade flows than other SSA countries. Nonetheless, the broader region is affected by same the inflationary pressures the rest of the world is experiencing. For most SSA countries, central bank policy rates held steady during 2021. But interest rates may rise in 2022, particularly if, as expected, US interest rates increase, which would especially affect such countries as South Africa that are reliant on portfolio inflows as an important source of external liquidity. Moreover, a resilient US dollar combined with softer global commodity prices (except for oil) is likely to weaken SSA national currencies against the greenback in 2022, with the pace of depreciation determined by emerging market investor sentiment expected to be volatile in the face of rising interest rates in the US and key markets such as Brazil and Russia. Managed float exchange rates such as Nigeria's naira are expected to move sideways during 2022 to buffer local price pressures.

Attempts at fiscal consolidation to stem the region's rising public sector debt burden

Commodity-related exporting countries benefitted from a tax windfall over 2021 amid more buoyant prices. But spending obligations combined with rising debt servicing costs maintained a high overall fiscal deficit-to-GDP ratio across the region. Access to concessional lending through IMF support programs will nonetheless offer a solid anchor for fiscal consolidation over the medium-term, and governments can take advantage of debt-neutral financing options such as the additional IMF's Special Drawing Rights allocation during 2022. The G20 Common Framework on Debt Treatment, which replaces the Debt Service Suspension Initiatives (DSSI), allows for debt restructuring and reprofiling for countries in distress, including the Republic of Congo and Mozambique, as well as other high-risk countries such as Cameroon, Ghana, and Kenya. Only Zambia, Ethiopia, and Chad, however, have agreed to participate in the G20 Common Framework. Their progress, and especially the pace of debt restructuring, will be monitored closely across Africa as a bellwether for the difficulty of securing support across a more diverse creditor landscape. Fiscal capacity across SSA will remain constrained over 2022 due to debt servicing obligations and expected political opposition to revenue-raising initiatives. This includes taxation, as seen with Ghana's e-levy debate, as well as planned privatisations in Kenya, Ethiopia, Angola, and Nigeria, among others, due to concerns of low asset valuations, size of liabilities, and regulatory uncertainty.

Political unrest, constrained fiscal capacity, rising cost of living, and upcoming elections are likely to drive further government instability across the region

SSA was hit by four successful coups in 2021 (Mali, Chad, Guinea, and Sudan) as well as the outbreak of civil conflict in Ethiopia. These disruptions derailed economic recoveries in each of these countries, which also face increasing international isolation due to sanctions or the suspension of support such as financial aid and preferential trade access. While the littoral countries of West Africa are relatively more stable, in 2022 they will focus on curbing the expansion of jihadist activity from the Sahel region. The COVID-pandemic has also led to increased instability across SSA. Since 2020, 37 million Africans have fallen into poverty, according to the United Nations, and an additional 13 million people lack access to electricity, according to the International Energy Agency. The degraded livelihoods of so many citizens, together with eroding governmental fiscal capacity and rising inflationary pressures, heightens the risk of unrest across Africa, particularly in countries heading into leadership elections such as Angola, South Africa, Kenya, and Nigeria. Also noteworthy is that support from international donors such as the US and European countries is evolving to the provision of primarily financial and technical aid to allies who demonstrate loyalty. This is evidenced in 2021 by the withdrawal of French troops from Mali and the deployment of regional forces to aid Mozambique's counter-terrorism efforts.

AfCFTA's evolution

Since the launch of the Africa Continental Free Trade Area (AfCFTA) in January 2021, there has been incremental progress around key sticking points such as tariff liberalization schedules and rules of origin (RoO). However, progress continues on the diplomatic and infrastructural fronts to deepen trade linkages, including South African President Cyril Ramaphosa's tour of West Africa in late 2021 and the roll-out of the Pan-African Payment & Settlement System (PAPSS) in January. The AfCFTA, which is the world's largest free trade area by number of countries, can serve as a catalyst for industrialization and the development of regional value chains, particularly as global supply chains restructure in the wake of COVID-19 and in anticipation of an energy transition. IHS Markit estimates that the AfCFTA can, if fully implemented, increase the total trade in goods between its members by a third, and that trade between AfCFTA countries that do not currently share the same free trade agreement would increase from USD13 billion to USD32.5 billion annually. For AfCFTA, 2022 will be a critical year for gaining traction, especially through securing agreements within the continent's regional economic communities (RECs)—the building blocks underpinning the AfCFTA—over key sticking points. Similarly, lack of political resolution within RECs over common tariff liberalization schedules and RoO especially for goods produced in special economic zones will delay full AfCFTA implementation.

Africa and COP-26

Many African governments sent high-level delegations to COP26 to advocate their position that any transition must be "just" and consider the economic asymmetries between countries. African governments, through the joint lobbying organization the African Group of Negotiators on Climate Change (AGN), also demanded fulfilment of Article 9 in the Paris Agreement which requires developed countries to provide financial resources to assist developing countries with mitigation and adaptation, thereby supporting a fiscal balance between the two geographies. To date, however, this funding pledge has not been met. According to the Organization of Economic Co-operation and Development (OECD), between 2016 and 2019, 43% of climate finance went to Asia, while only 26% went to Africa. Moreover, 79% of such funding provided in 2019 was in the form of largely non-concessional loans, which means that their recipients, including developing countries across SSA, will pay commercial interest rates to access these instruments. In the lead up to COP-27, which will be hosted in Egypt, African leaders are likely to push for increase in concessional financial support. President Ramaphosa is on the record stating that Africa needs USD240 billion a year to shift to clean energy, mainly from grant funding.

III. Upstream Oil & Gas

Upstream development activity is constrained, and the competitor mix is shifting

Pandemic disruption and energy transition-related pressures on company E&P strategies and financing will continue to constrain upstream project development in SSA in 2022, and the scale of any post-COVID rebound in upstream project development remains unclear. Even so, an uptick in E&P activity is likely in 2022.

Only four FIDs were taken on new projects in 2020, but 10 were sanctioned in 2021, including Eni's sanctioning of the Agogo Phase 2 development in Angola's Block 15/06, highlighting international oil company (IOC) focus on short-cycle projects offering quicker returns. Notable start-ups during 2021 included including Chevron's (formerly Noble Energy) Alen gas hub in Equatorial Guinea, marking the first third-party gas to be processed at the EG LNG plant.

While around twenty projects in the region are FID-ready today, in 2022 fewer than half of these may be sanctioned. Many of the sanction-ready projects are in Nigeria, but the 2021 Petroleum Industry Act (PIA) may not offer enough incentives to effectively support their development—which highlights the challenges that even governments seeking to expedite and maximize resource monetization may face. It is expected, however, that Uganda's long-awaited upstream developments at Lake Albert will be sanctioned in 2022, as the critical enabling agreements and legislation for the related East Africa Crude Oil Pipeline (EACOP) via Tanzania were signed in 2021. But whether EACOP will secure finance remains a question, as several financial institutions have declined to offer project loans under pressure from civil society groups concerned about the project's environmental impact.

Meanwhile, the evolution of Africa's upstream competitive landscape is accelerating as IOCs revise their strategies—to increasingly focus on "agile" short-cycle projects and "advantaged" developments with lower costs and emissions—and new players emerge. Legacy asset sales by major IOCs (such as Shell in Nigeria, Total in Gabon, and ExxonMobil in Chad) and some NOCs (such as Sonangol) are expected to continue amid policy, shareholder, and financing constraints. Independents, foreign NOCs, local players, and private equity-backed firms will be key buyers. Where buyers are unwilling, IOCs may seek creative solutions for declining assets in the mold of BP and Eni's cooperation in Angola: joint-venture portfolio mergers to boost efficiency and reduce costs. But such shifts in the competitor mix may give rise to labor unrest, and NOCs will have to grapple with financial and technical gaps left by departing majors.

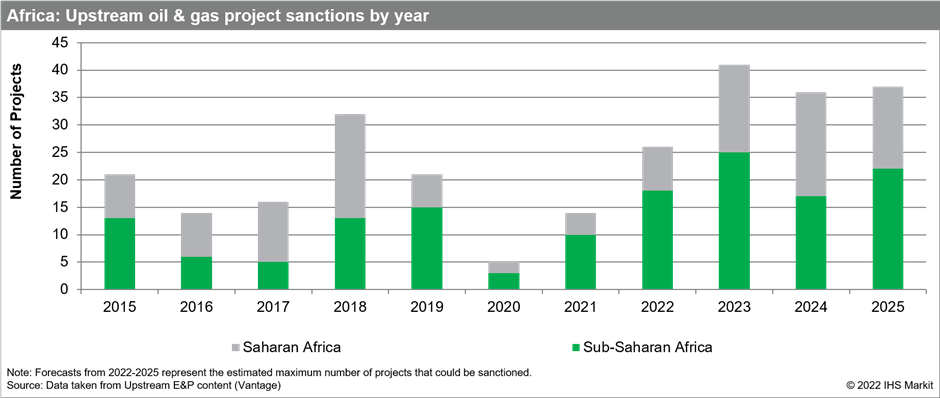

Governments face challenges with new upstream licensing, but Africa leads on frontier drilling

Disruption, delay, and muted investor interest characterized upstream licensing rounds in 2021, with more countries since having turned to direct licensing. Last year's rounds in Gabon, Liberia, Senegal, and Uganda disappointed, but Angola's onshore round was successful in attracting new, smaller foreign players and local firms. In general, smaller firms were more prominent in bidding in 2021. But 2022 deepwater rounds in Angola and Mozambique are aimed at major players, which will test investor interest in established and frontier basins, respectively.

Despite lackluster results in 2021, African exploration holds promise for 2022

At the time of writing two of Sub-Saharan Africa's most exciting exploration wells were underway in offshore Namibia within the Orange-Sub basin—both Shell's Graff - 1 and TotalEnergies Venus - 1 have the potential to start 2022 off with a bang. Africa, like most regions, has hosted far fewer exploratory wells in recent years than in the past; the 2014-15 oil price crash depressed exploration appetite worldwide, and just as the market seemed to again be picking up, the COVID pandemic struck, which precipitated the 2020 oil price crash. But 2021 showed an uptick in exploration drilling relative to 2020.

Africa's largest discovery for 2021 was the Baleine discovery within the Côte d'Ivoire Basin in offshore Côte d'Ivoire, followed by the Eban discovery within the Tano Basin in offshore Ghana and the Cuica discovery within the Congo Fan in offshore Angola. All discoveries were made by Eni and located in deepwater. Both the Eban and Cuica discoveries were the result of "infrastructure-led exploration," a strategy of focusing on plays that leverage nearby existing infrastructure. The Baleine discovery, on the other hand, was a frontier play within a more mature basin. These three discoveries comprise over 90% of the recoverable resources discovered in Africa in 2021, while the Baleine discovery alone represents more than two-thirds of the resources discovered within the year.

In 2022, it is expected that the success of infrastructure-led exploration campaigns will continue to drive a "value over volume" approach to exploration budgets. As such, it is expected that several infrastructure-led exploratory wells will be drilled in offshore West Africa. However, Africa will host between five and eight high-impact wells in 2022, including in Sao Tome Principe, Zimbabwe, Mozambique, Gabon, Congo, and South Africa.

African governments grapple with the pandemic, slowing E&P policy progress

To compete for increasingly scarce investment dollars, host governments in SSA are under pressure to align fiscal and contractual terms for upstream oil and gas with the revised strategies of IOCs. African government capacity remains stretched, however, due to the political, economic, social, and healthcare challenges posed by the COVID-19 pandemic, pushing energy policymaking down the agenda. Heightened international concern about climate change has further complicated the strategic policy outlooks for established hydrocarbon producers and new frontiers alike, as policymakers attempt to reconcile their desire for domestic resource monetization with the objective of reducing carbon emissions.

Nevertheless, in August 2021 a landmark moment was reached when Nigeria's PIA was signed into law. This far-reaching hydrocarbon-sector reform was first proposed in 2008, but the political will to overcome vested interests protecting the status-quo coalesced only in 2021 due to Nigeria's increasingly serious economic woes and related domestic instability driven by two recent oil-price shocks. Accelerating IOC disengagement from Nigeria amid corporate capital discipline, portfolio consolidation, and climate pressures also drove belated progress on reform.

The PIA covers the entire hydrocarbon value chain and replaces a host of laws—several of which date back decades—underpinning Nigeria's petroleum-sector institutions, regulations, and fiscal terms. One of the most significant impacts of the PIA is a reduction in income tax and royalty rates for projects across onshore, shallow-water, and deepwater. But foreign investors remain concerned by the overall burden of costs, levies, and taxes in Nigeria, which the PIA expanded. So far, the impact of the new legislation appears mixed, with some new projects such as Total's Preowei apparently now moving forward, while others such as Shell's Bonga Southwest further delayed.

South Africa's revised Upstream Petroleum Resources Development Bill (UPRDB), which was submitted to parliament in July 2021, is another important policy initiative for Africa's upstream sector. Since South Africa's government approved the draft bill, the likelihood of major revisions appears low and it should be passed in the first half of 2022. The legislation will increase participation by Broad-based Black Economic Empowerment (BBBEE) firms and by the newly merged national oil company the South African National Petroleum Company (SANPC). Fiscal elements expected in a separate Treasury bill may moderately raise overall tax take, but the certainty afforded to investors by passage of the bill should facilitate the continued expansion of South Africa's hydrocarbon sector.

Further investor-friendly changes to E&P terms across Africa are likely to emerge in 2022 as governments seek to attract and retain investment, with Equatorial Guinea among the countries said to be considering improvements. Tanzania, meanwhile, is actively re-engaging with Equinor and Shell over terms for LNG development, aiming to sign a key Host Government Agreement (HGA) in 2022.

Despite climate policy and civil society pressures on fossil fuels, African resource holders remain committed to gas

The global debate continues over the acceptability of gas as a lower-carbon fuel for the energy transition. Nigeria's 2060 net-zero pledge made at Glasgow's COP26 climate meeting was an important signpost about SSA's engagement with the energy transition. But Nigeria's pledge is contingent on using gas until at least 2040, and the PIA promotes new investment in gas development and distribution to drive economic growth and electrification. Countries such as Côte d'Ivoire, Mozambique, Senegal, and South Africa are similarly committed to utilizing their vast domestic gas resources for economic development.

In 2021 the African E&P sector faced increasingly insistent challenges from civil society and constraints on financing due to climate concerns. High-profile opposition to hydrocarbon development occurred in South Africa (to E&P activity in environmentally sensitive areas by Eni and Shell), Mozambique (a legal challenge by Friends of the Earth to UK government-backed financing of Mozambique LNG), and, as noted above, Uganda (a letter signed by 263 civil society organizations calling on banks to not finance the EACOP) among others, and such legal challenges and civil society pressure are likely to expand in 2022 and beyond.

IV. Africa Downstream

SSA was the world's fastest growing region for oil product consumption. But in 2020 the pandemic put a hard brake on this growth, curtailing Sub-Saharan demand for the first time in over two decades. The region saw substantial demand destruction, in particular, in major oil producing countries and economies heavily reliant on tourism. Yet compared to volume losses registered in other regions around the world, many African economies proved to be more resilient than predicted.

Sub-Saharan Africa oil product demand bucked the trend

In 2021, product demand in SSA grew by almost 7% from the previous year, standing at only about 3.5% below pre-pandemic levels. This compares to global demand for refined products, which is still about 7% lower than 2019 levels. One reason for this is that, with a few notable exceptions such as South Africa, there were fewer restrictions on mobility in Africa than in the rest of the world. This difference was highlighted in 2021 when demand for products in transportation, especially gasoline, already reverted to pre-pandemic levels. For gasoil, however, the recovery of demand was weaker and consumption has remained under pre-pandemic levels. But the decline in demand in 2020 was less pronounced than expected owning to the sustained appetite for gasoil driven by the transportation of essential goods and the extractive industry, led by China's strong comeback in the sector. This was most notable in East Africa and in the Democratic Republic of Congo and Zambia, where growth rates for gasoil were positive even in 2020. Jet fuel demand has yet to recover as other fuels have, however, despite the aviation sector beginning to recover in line with eased travelling restrictions seen in 2021.

Omicron has slowed jet fuel demand recovery and 2022 is expected to be shrouded with uncertainty

The aviation sector showed positive signs of recovery over the past year. In Ethiopia and South Africa—Africa's main aviation hubs—jet fuel demand in Q2 2021 reached the highest levels since the start of the pandemic, standing at 70% and 80% of their 2019 levels, respectively. However, the discovery of the Omicron variant triggered flight bans that cascaded across Southern African countries, resulting in plummeting demand for jet fuel. While many African countries have been reluctant to reimpose disruptive domestic measures in response to Omicron, the path to jet fuel demand recovery in 2022 remains fraught and will be closely tied to how countries respond to new variant outbreaks. In the near term, the slow rollout in Africa of COVID-19 vaccine programs along with recession-like conditions such as GDP loss, lower foreign direct investment, and less disposable income are all factors expected to constrain demand growth for all fuels.

Refinery closures are unlikely to reverse in 2022

Most of the region's markets have no refining capacity and are entirely dependent on refined product imports. This gap in product supply has been only exacerbated by continued growth in product demand and by the closures of existing refineries over the past decades due to high operational costs, caused largely by unfavorable yields, and to a lack of maintenance along with low utilization levels across an aging and non-efficient regional refining system. Consequently, existing refineries are effectively reliant on government support in one form or another—and 2021 was no exception. Since the beginning of the pandemic, a wave of refinery closures has swept across SSA, most notably in South Africa and Nigeria. Crude runs in Nigeria have been particularly weak in recent years and fell to zero in 2020 when all NNPC refineries were officially closed for much-needed—and long-awaited—upgrades at a time of depressed demand. Although the financing for this work was reportedly secured, the fate of the NNPC refineries remain uncertain, especially with the giant Dangote plant expected to come on-line. In South Africa, half of the crude refining capacity was lost due to industrial accidents. While Engen officially announced last year that its plant will be converted into an oil terminal, whether Astron Energy's Cape Town refinery will reopen remains highly questionable in light of today's uncertain markets. Elsewhere in SSA, several refineries are unlikely to reopen this year, if not all, notably Cameroon's Limbe refinery, which was shutdown following a fire, and Zambia's Indeni plant, closed for refurbishment work. All this suggests that imports across SSA will increase further in 2022, pushed even higher by recovering demand.

The road ahead: a refinery renaissance, or an accelerated retreat?

While several new refining projects were announced in SSA, most of them have fallen flat, with a few exceptions. The 30,000 b/d Ugandan refinery project gained momentum in 2021, but reluctance among banks to finance the oil pipeline puts it at risk of further delays or cancellation. In Nigeria, the 600,000 b/d Dangote project was originally slated for 2021, although IHS Markit expected that the plant would come on-stream no earlier than 2023. It is questionable whether continued fall-out from the pandemic, rising project costs, and the venture's rumoured indebtedness will further delay this project, which otherwise some consider to be "too big to fail." And in South Africa's highly competitive market, with refineries already struggling amid shifting demand, it is questionable whether the new government rule of lower sulfur emissions—requiring refineries to undertake expensive upgrades—will become the final nail in the coffin for the industry.

V. Africa Power and Renewables

Power demand rebounded in 2021 and will continue to grow in 2022, but at a slower pace

Power demand across SSA grew by over 5% in 2021, after dropping 4% in the previous year due to the disruptions and economic slowdown caused by the COVID-19 pandemic. Demand recovery was led mainly by the commercial and industrial segments, which grew at around 4% and 8%, respectively. Residential demand also rebounded, even though in 2020 it did not experience negative growth, unlike the other demand segments. Growth in overall power demand is projected to continue into 2022, though at a slower pace than 2021 and assuming that economic activity will not be hit especially hard by new waves of COVID-19 variants. It is also important to note is that power demand across SSA remains on average less than 500 kWh per capita—among the lowest levels worldwide.

In 2020, South Africa, which accounts for about 50% of SSA's total power demand, experienced one of the region's steepest declines in demand both due to COVID and to scheduled load shedding, which was exacerbated by the country's worsening power supply crisis. But South African power demand recovered to pre-pandemic levels in 2021 thanks to the swift recovery in industrial sector, where demand increased 8% year-on-year. SSA's second largest power market is Nigeria, accounting for nearly 11% of the region's total power demand but which continues to be challenged by a high level of suppressed power demand as a consequence of persistent supply challenges and low electrification rates. Although in 2021 the recovery of Nigeria's power demand was led by the commercial and industrial sectors, the offgrid sector accounts for about half of the country's total power demand.

Diversification of energy sources away from oil and coal to gas and renewables will continue and gain momentum

In 2021, efforts by governments across SSA to diversify energy sources resulted in less oil-based power as a percentage of total generation as well as the increased utilization of gas and renewables. This trend is projected only to continue as countries and companies increasingly commit to invest in less carbon-intensive sources of power and lower carbon emissions across the economy. With the installation of gas-based plants, such as Afam III in Nigeria (240 MW), and an increasing number of solar photovoltaic (PV) projects in, for example, Ghana, Senegal, and South Africa, the region is shifting towards the use of more carbon-friendly fuels rather than relying primarily on traditional carbon-intensive coal and oil.

Hydropower remains an important source of generation in many Sub-Saharan countries. But hydropower is susceptible to climate-related risks such as drought, with important consequences for economies—Zambia being a case in point. Investment in renewables, particularly solar PV projects, has been a popular option for increasing energy diversification, enjoying generous support from multilateral financing institutions. While coal-fired generation is not predominant in SSA's overall energy mix, in South Africa and Botswana coal holds the largest share in the national power mix. But across the region-and indeed the world—the future of coal-based planned projects is increasingly uncertain as international financial players reconsider their support to carbon-intensive assets, especially for coal.

Countries across SSA are increasingly taking measures in line with energy transition objectives. This includes fuel-switching in existing generation assets from oil to gas where dual-fuel power plants operate, such as in Ghana, decommissioning exclusively oil-fired and coal-fired plants (South Africa is expected to retire 8 GW of coal capacity by 2030 and 22GW by 2040), and increasing investment in renewables-based projects. Such shifts are occurring at a variety of speeds across the region owing to each country's specific power profile, with key determinates including power supply gap vis-à-vis growing power demand, limited financing availability, and the need to provide reliable power at peak hours. In countries such as Nigeria, distributed diesel gensets still represent a vital source of power because low available capacity of the on-grid power plants and unreliable transmission and distribution infrastructure require alternative solutions to compensate the grid supply failure. And decarbonization is already posing a problem for Eskom, the South African utility, where the Department of Environment recently denied its request for a pollution exemption for 16 GW of coal-fired capacity, exposing Eskom to the risk of that its power plants will be forced to shut down even as the country suffers from chronic load shedding. At COP-26, however, South Africa signed an initial pledge of $8.5 billion finance package with France, Germany, the UK, the US, and the EU to help the country to decarbonize and take advantage of new energy transition economic opportunities such as green hydrogen and electric vehicles.

Renewable projects resumed but suffered delays, challenging initiatives to increase energy access

The implementation of renewables projects gradually resumed in 2021 across SSA as COVID-19 related restrictions were reduced or lifted. Delivery schedules were delayed, however, due to the interruption of equipment deliveries and access to construction sites. Chronic bottlenecks in the global supply chain have led to higher equipment costs and supply shortages for solar PV and onshore wind projects, and are expected to continue to affect both new projects, especially in the near-term, and those further advanced and at the cusp of beginning construction. But 2021 also saw the completion and launch of a number of renewables-based projects and competitive tenders to procure over 5 GW of solar PV and wind projects across the region, with South Africa accounting for most of the capacity. Other countries such as Namibia, Togo, and Zimbabwe, however, have also adopted the tender procurement model to accelerate the implementation of renewables projects. But will such projects, along with other resource-based power additions, provide sufficient power to support the needs of SSA, including the lives and livelihoods of 600 million Africans who lack access to electricity—a number that grows continually as Africa's population is projected to double by 1.2 billion in 2050? This is a critical question for African policy makers and is of fundamental importance to the success of global energy transition initiatives.

Learn more from IHS Markit's 2022 Africa Energy Outlook series, covering upstream to downstream, here

This article was published by S&P Global Energy and not by S&P Global Ratings, which is a separately managed division of S&P Global.