Dec 05, 2023

Clean energy investments in the “Global South”: Challenges and opportunities in the electric power sector

By Etienne Gabel

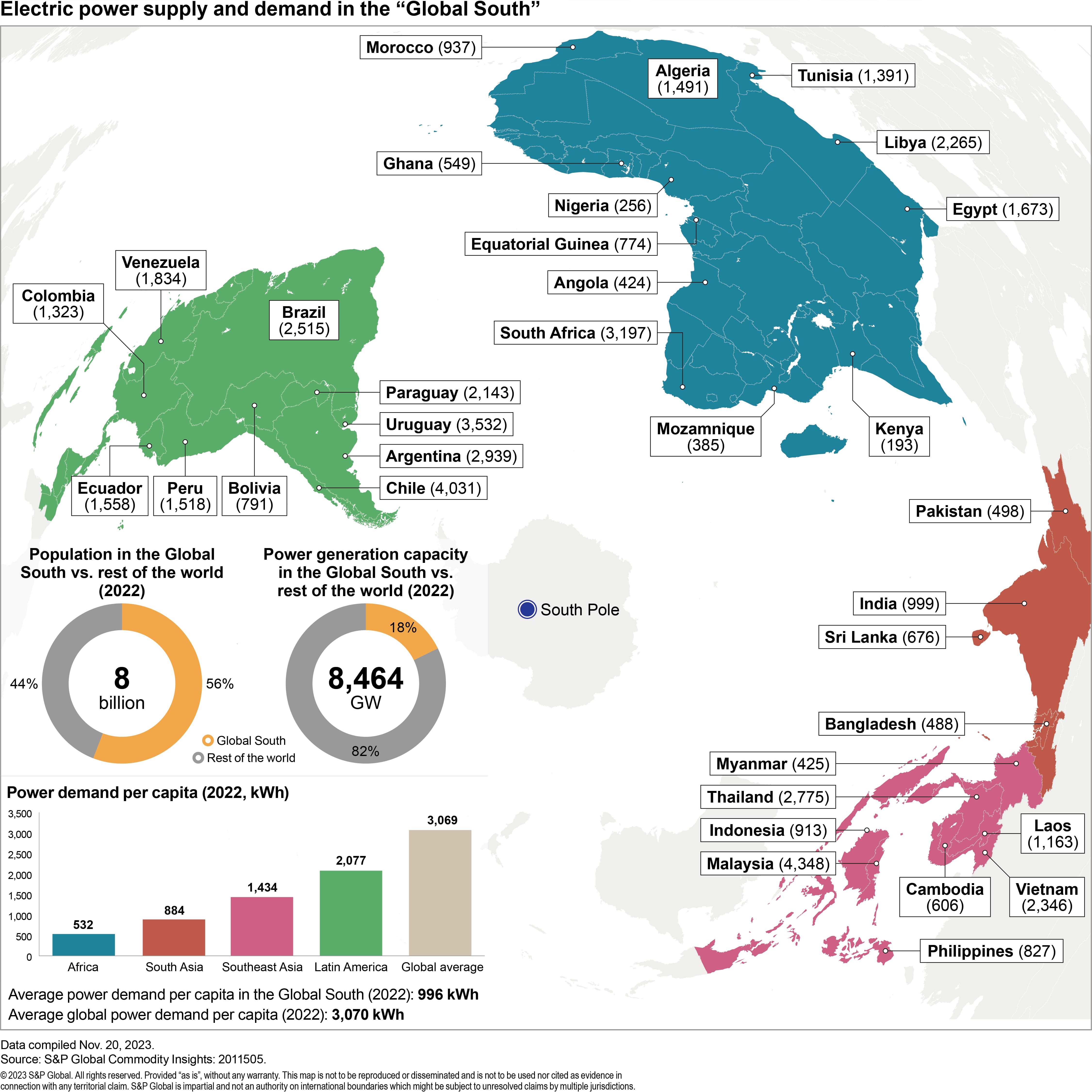

The "Global South"—a term often used for the developing countries of South Asia and Southeast Asia, Latin America, and Africa—houses 56% of the world's population but holds only 18% of its power generation capacity (see figure below). Power demand per capita, at about 1000 kWh/year (about the same as a clothes dryer), is less than a third of the world average.

Population growth, urbanization and economic development will lead to very rapid electricity demand growth in the Global South—300 TWh of additional consumption every year for the coming 25 years, according to S&P Global reference outlooks.

How to decarbonize the power mix under these circumstances, in markets where public funds and foreign capital can be scarce, and where fossil fuels still produce 60% of electricity, creates a unique set of challenges and opportunities for private sector investments in clean energies.

Ahead of COP28, S&P Global Energy held a webinar discussing the power sector landscape and what companies may need to consider when evaluating opportunities in the region. Below we share a portion of the discussion topics. The full webinar is available here.

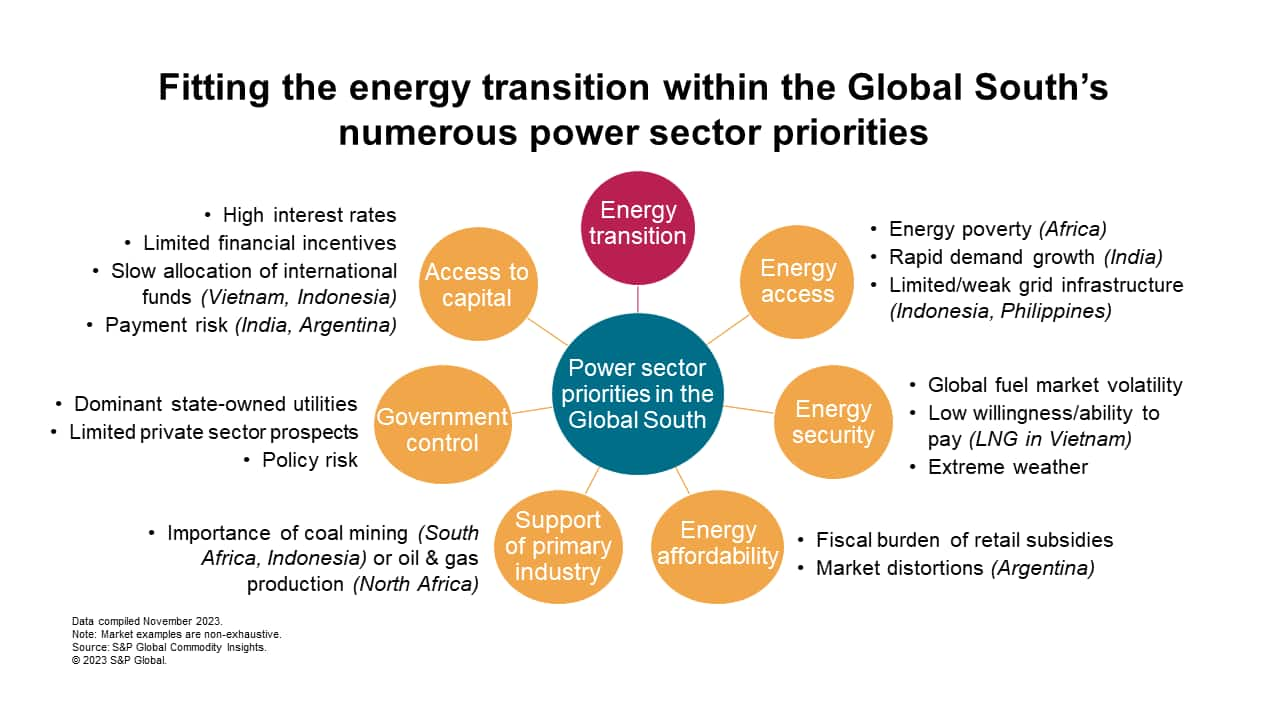

Fitting the energy transition within the Global South's numerous power sector priorities

The Global South's long road towards decarbonization must fit within a set of policy and market priorities that has governed the power sector's development to date (see figure below). These priorities in turn affect the business models suitable for private sector investments in the region's renewable resources.

- Energy access: Demand growth, as discussed above, places huge pressure on energy infrastructure. Longstanding underinvestment in the grid further complicates the deployment of variable renewable resources. Not all supply resources and not all business models are scalable at high pace, especially in the Global South where access to capital is an issue.

- Energy security: The availability of local resources has been determinant in the Global South's fuel choices to date. Domestic coal is cost-effective in South and Southeast Asia, conventional hydroelectric power is abundant in Latin America, and oil and gas are economical in parts of Africa. Conversely, price swings in global LNG have caused constraints in exposed markets in Southeast Asia. Yet today new wind and solar projects are typically competitive compared with even existing conventional assets.

- Energy affordability: This acute imperative can dictate policy direction, with many countries offering subsidies that keep retail power prices artificially low for the end users. This in turn can create market distortions and financial burden for power players (e.g., in India, distribution companies have $75 billion in outstanding dues to generators), in a way not seen in developed nations. These then alter the risk profile of investments.

- Support of primary industry: In most countries of South and Southeast Asia, and in South Africa, coal is central to the broader economy and employs a large local workforce. In India, the government already indicated that coal will stay to support energy security. Business models to deploy renewables must regularly look to co-exist rather than replace these ingrained industries.

- Government control: Many Global South power markets are highly regulated, which limits the role of private players. Major reforms are often needed, from the clarification of the role of private players (like in South Africa), to opening the wholesale market (as occurred in Vietnam), or tariff reforms (India). At the same time, these markets require huge private capital injections, typically from abroad.

- Access to capital: Companies struggle to obtain attractive financing when facing high interest rates (e.g., Pakistan), high inflation (Argentina), and foreign exchange risk (e.g., Egypt). Developing a project in the Global South, where government incentives are limited, requires a different business evaluation than in developed nations that allocate billions of dollars in funding and tax rebates. Financing from multilateral institutions is often key, but delays in the funds' distribution, like in Vietnam or Indonesia, cause issue.

Learn more about our global power and renewables research.

Etienne Gabel, a senior director at S&P Global Energy with the Global Power and Renewables team, specializes in the analysis of market and regulatory developments in power sectors worldwide.

Posted 5 December 2023

This article was published by S&P Global Energy and not by S&P Global Ratings, which is a separately managed division of S&P Global.