26 Jan 2022 | 15:15 UTC

Infographic: Insufficient lithium supply could decelerate energy transition

By Henrique Ribeiro and Melenie Yuen

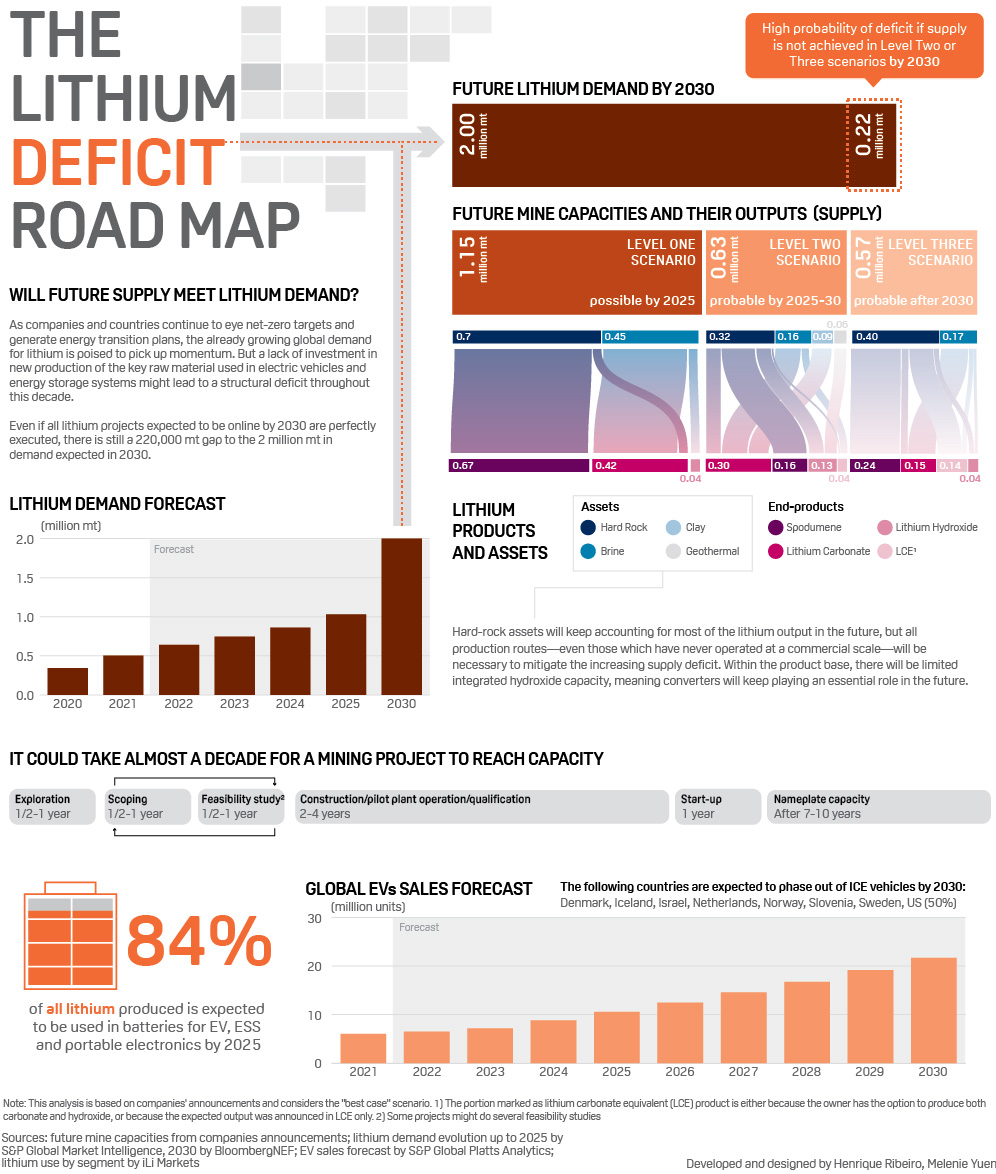

Lithium is a key raw material for electric vehicles and energy storage systems, but the lack of investment in new supply in previous years might generate a structural deficit throughout this decade, data from the expected supply versus expected demand (both until 2030) demonstrates.

During the last lithium price bear run, from mid-2018 to mid-2020, investments shriveled from the specialty chemical. In early 2018, a lot of new spodumene ore capacity started running from previous investments in anticipation to an expected EV boom that didn't start until the second half of 2020; the oversupply crashed prices and halted investments.

This time, the situation is completely different because demand is solid and growing much faster than supply. EV sales accounted for almost 20% of new car sales in China and over 25% in the European Union in recent months, forcing suppliers to try accelerating expansion and new projects. Financing and permitting, however, are considered significant hurdles.

Click here to see the full-sized infographic

This has translated into surging lithium prices. Since early 2021, Platts lithium carbonate CIF North Asia rose 548% to $41,200/mt on Jan. 21, 2022. Lithium hydroxide CIF North Asia moved up 318% to $37,700/mt and the spodumene concentrate used for conversion in lithium chemicals surged 588% to $3,100/mt FOB Australia basis.

Although the battery industry has been investing significantly in downstream battery capacity to power the surging EV demand, lithium is still getting less funding than required — and such investment could be too late to prevent a structural deficit in the coming years.

"Unfortunately, battery capacity can be built much faster than lithium projects," said Joe Lowry, president of consulting firm Global Lithium. "The lack of investment in lithium capacity over the past five years will extend the supply shortage."

The situation is so critical that Lowry didn't want to make demand forecasts beyond 2027 —the supply-demand imbalance could be so serious that supply might end up capping demand, so forecasting beyond that could be misleading, he said.

"Even well-capitalized major lithium companies have struggled to meet their expansion targets," Lowry said. "New producers have seen their project timelines extended in many cases due to Covid and related supply chain issues along with their ‘learning curves' OEMs and battery producers that assumed ‘market forces' would ensure adequate battery raw materials are finally taking note of the supply-demand issue but much too late to solve the problem in the near to mid-term."

The outlook described by Lowry is confirmed by Platts' comparison between the expected supply and the expected demand until 2030 (see infographic below), which shows that supply should not reach the projected 2 million mt demand by the end of the decade. To run the analysis, Platts divided the projects in three levels depending on when they should reach the nameplate capacity.

To see the full list of projects considered in the infographic, as well as the criteria for the categorization, click here.

Carbonate vs hydroxide

Despite the increasing interest for lithium hydroxide, which is required in nickel-rich battery chemistries that have higher energy density (allowing EVs to drive longer at a single charge), most of the existing integrated capacity is dedicated to lithium carbonate.

Although more greenfield projects — including some brines, that necessarily need to produce carbonate in the first place — are expected to include hydroxide conversion, and most of the hard rock supply is targeted for hydroxide, carbonate will still represent a significant portion of supply and hydroxide production will depend on the adequate supply of raw materials for conversion.

The lack of feedstock (usually spodumene) should be a concern for several projects of non-integrated conversion capacity, of which most are eyeing to supply hydroxide. Adding conversion capacity is less capital-intensive and faster than building the underlying feedstock capacity, meaning there could be a mismatch that could leave some hydroxide converters with idled capacity, despite the surging demand, sources said.

Some projects will also have the option to producer either carbonate or hydroxide depending on the market conditions. The surge in demand for nickel-free lithium-iron-phosphate battery chemistries, including official announcements from the likes of Tesla and Volkswagen, means demand for lithium carbonate should stay healthy throughout the decade.

The second generation of lithium projects should also bring new kinds of assets that were never developed before, such as clay and geothermal brines, as well as the potential employment of the direct lithium extraction (DLE) technology. Most of these will also target to increase the integrated hydroxide capacity, but they will still need to prove their commercial viability.

DLE has been touted by some as the holy grail for the lithium industry, yielding higher quality products at a faster production schedule, with lower costs and lower water consumption. Others, however, stress that DLE is not an off-the-shelf solution that can be applied the same way in all projects, as well as the fact that it has never been tested on a commercial scale, meaning its success is still yet to be proven.