08 Mar 2021 | 09:55 UTC — Insight Blog

Commodity Tracker: 6 charts to watch this week

Growing 5G infrastructure needs support demand for niche metal iridium, while OPEC+ signals and US rig data are key talking points for oil markets. Plus, the latest UK power capacity auction generates a record price, and Asian aromatic petrochemicals are buoyed by a combination of unusual events, while PVC prices spike on tight supply.

-

1. 5G metal iridium could see more upside after all-time high

What's happening? Platinum group metal (PGM) iridium has been on a tear over the past three months, rising nearly three-fold since December 2020. The Platts New York Dealer iridium price rose to $4,800-$5,125/oz for the Feb. 26-March 4 period. On March 5, Johnson Matthey – the largest secondary PGM refiner in the world – said in its iridium base price stood at $5,100/oz, while refiner Engelhard Materials Services (BASF) of Germany quoted $5,500/oz. Market sourcestold Platts the latest rally was caused by supply shortages from South Africa, which accounts for 81% of global iridium mine supply, and PGM producers coming into the market to buy due to contractual commitments. Another key bullish driver has emerged recently: 5G-related demand. Iridium is a critical element in several niche products, including temperature resistant crucibles used to grow lithium tantalate crystals for electronics and telecommunications systems.

What's next? Supply issues in South Africa and robust demand look set to continue in the near-term. Further out, there is a potential use for iridium potentially in the production of green hydrogen via electrolysis, suggesting demand upside in the future.

-

2. OPEC+ sticks to cautious oil output plan, surprising market

What's happening? OPEC and its allies agreed to largely keep their production cuts unchanged in April, including Saudi Arabia's voluntary 1 million b/d curtailment, at their latest meeting March 4. The decision, which wrong-footed traders who had been expecting more supply to be released, means the group will keep about 8 million b/d of crude production, or roughly 8% of pre-pandemic supply, off the market for another month. And it keeps the OPEC+ alliance firmly in control of global oil supply, with US shale companies still financially limping and coping with the aftermath of the Texas freeze.

What's next? Saudi Arabia said it would begin gradually releasing its extra 1 million b/d cut after April, but it would depend on market conditions. The kingdom also wants to see high quota compliance by the other members of the alliance. OPEC+ ministers justified their conservative approach by citing uneven vaccine rollouts across the world, still-bloated inventories, and stringent lockdown measures that continue to be a damper on oil demand. The alliance will convene again on April 1 to decide on May production levels.

-

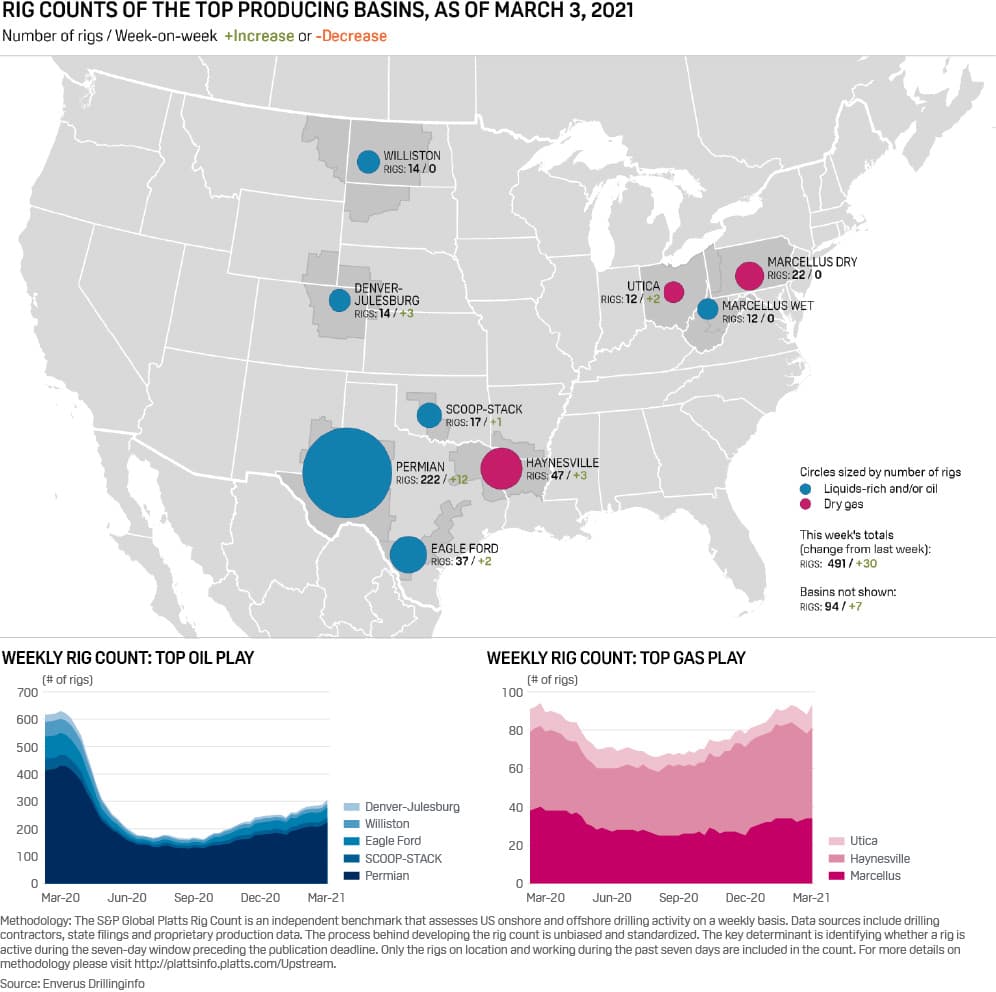

3. US upstream activity ramps up, aided by oil price rise and thawing weather

Click to enlarge

What's happening? The US oil and gas rig count leaped 30 in the week ending March 3 to 491, rig data provider Enverus said, reaching the highest total since late-April 2020, as WTI oil prices climbed amid buoyant outlooks at a major energy conference, CERAWeek by IHS Markit. The Permian Basin, sited in West Texas and Southeast New Mexico, was the clear focus area for growth, with a weekly increase of 12 for a total 222. Rig totals in the Permian are now at the highest since late April 2020.

What's next? S&P Global Platts Analytics noted that while a large week-on-week gain, it was a needed one after two weeks of flat rig numbers. The unit also said the recovery may have been delayed by the late-February freeze in the US, which could mean steadier additions in the coming weeks. At CERAWeek, upstream players repeated their intentions to stick to austere capital budgets, growth targets of 5% or less per year and give sizeable cash returns to shareholders, alongside cost cutting and efficiency drives.

-

4. February's US freeze, Japan earthquake among factors lifting key Asian aromatics prices

What's happening? Benzene, toluene and xylenes margins in Asia have surged above 2020 levels thanks to a slew of unprecedented events in the previous month. The products are most commonly used in gasoline blending and production of downstream polymers. Factors behind the price jump ranged from winter storms in the US and an earthquake in Japan, to the start of refinery maintenance season. This led to an unusual scenario, with both paraxylene and benzene, the two largest product markets for aromatics, both bullish but on unique circumstances.

What's next? Asian BTX prices could continue to be supported in the short term as Asia has only just started to enter the maintenance season, against a backdrop of healthy demand for aromatics. Another support factor comes from the upstream oil market, which reacted to the winter storms that disrupted major production sites in the US, with return to normal operation is still uncertain. Higher BTX prices could render some gasoline blendstocks such as toluene and mixed xylenes unattractive for blending, which could redivert the materials back to the BTX pool for the production of downstream polymers.

-

5. US production woes drive PVC prices to multi-year highs

What's happening? European supply of PVC, a key polymer used in the construction and automotive sectors, has been tight over recent months due to unexpected outages and force majeures occurring at major European producers. Recent weather-related events on the US Gulf Coast caused around 57% of US PVC capacity to shut down, creating an even tighter global PVC market, pushing prices to multi-year highs and beyond in the European and Turkish markets, and across the globe.

What's next? Spring maintenances at multiple European sites scheduled for March–April will continue to keep European PVC supply tight, while the expected restart dates and return to full operation of producers located in the US are currently unknown and supporting pricing levels globally.

-

6. Record price for UK year-ahead capacity market auction ahead of four-year sale

What's happening? Last week's T-1 2021/22 UK capacity market auction result (GBP45/kW/yr) was a new record and over five times the price achieved in the four-year-ahead T-4 auction for the same period (GBP8.40/kW/yr). The market pays the clearing price in monthly installments to successful bidders, ensuring availability of offered capacity for the agreed period. The latest price reflected the high level of capacity being acquired, after National Grid lifted the target capacity by 2 GW to 2.4 GW in light of the risk around non-delivery of a number of contracted units (notably Calon's gas fleet, EDF's nuclear fleet and the new ElecLink interconnector). "It also reflects the relative lack of value in the wholesale market,” S&P Global Platts Analytics said.

What's next? This week sees the UK's T-4 CM auction open March 9, seeking 40.1 GW for 2024/2025 delivery. The volume is down 1.1 GW on the Department for Energy, Business and Industrial Strategy's July 2020 guidance, and down 3.2 GW on the last T-4 auction for 2023/2024 delivery. Before that, target capacity for 2021/22 was 49.2 GW, and more than 50 GW for 2020/2021. Nevertheless, after last week's outturn, participants will be keeping fingers crossed for an improvement on March 2020's T-4 clearing price of GBP15.97/kW/year.

Reporting and analysis by Callum Colford, Filip Warwick, Sue Koh, Maxim Grama, Henry Edwardes-Evans, Starr Spencer and Herman Wang