20 Dec 2021 | 06:01 UTC — Insight Blog

China’s energy transition: Walking a thin line between decarbonization and disruption

China's efforts to decarbonize its power sector have triggered intense debate about the role of its existing fossil fuel-based electricity system and the extent to which the system will have to be recalibrated.

There is general consensus that an electricity supply chain based predominantly on renewables will have to be fundamentally different from one based on fossil fuels, mainly to handle intermittency issues and introduce market-based mechanisms for both power and carbon trading.

The debate, however, is largely around securing a smooth energy transition, ensuring stable power supply and the pace and criteria for decommissioning coal-fired plants.

The recent energy crisis exacerbated concerns around indiscriminate phasing down of coal, the economic impact of high energy prices and volatility if electricity prices are deregulated in a market-based system.

Chinese policy makers and top power utilities have adjusted their stance on coal-fired power generation after the crisis and called for a more realistic assessment of the energy transition instead of impulsive plant closures that endanger energy security.

The reassessment includes making room for gas in the energy transition as a bridging fuel with half the emissions footprint, as well as keeping coal plants as back-up power sources instead of complete decommissioning, until technologies and costs to solve the intermittency of renewables meet a certain threshold.

Chen Zongfa, Deputy General Counsel with China Huadian Corp., one of China's largest state-owned generation utilities, said a previous estimate of coal-fired power peaking within 1,200 GW had been raised to 1,250 to 1,300 GW.

"Like it or not, we still cannot get rid of coal-fired power in a relatively long period, because we need it as the 'ballast' that ensures energy security," said Xu Xiaodong, senior consultant with government-backed think tank China Electric Power Planning & Engineering Institute.

Meanwhile, China's carbon market is gathering steam and could cover two or three more sectors as early as 2022, in addition to the power sector. The implies a faster-than-expected rollout of China's carbon market for the eight sectors identified including refining and petrochemicals, chemicals, building materials, steel, nonferrous metals, aviation and paper.

China's largest industrial groups, energy companies and financial institutions are rapidly building internal systems for the measurement and reporting of greenhouse gas emissions, and developing capabilities for trading carbon credits.

Several of China's largest oil companies, manufacturing companies and power utilities had announced net-zero plans ahead of Beijing's official announcement of carbon neutrality target by 2060. Before the launch of the national carbon market in 2021, Chinese exchanges were already running pilot programs to test carbon trading.

Companies in China's most emission-intensive sectors are laying out their climate and carbon strategies due to pull and push factors that include domestic climate policy, and demands from international customers for proof of green electricity usage.

China's carbon market will see a few major trends – tighter supply of allowances, the introduction of institutional market participants, and rapid growth in the voluntary emission reduction market called Chinese Certified Emissions Reductions, possibly faster than the compliance market, which is driven by regulatory policies.

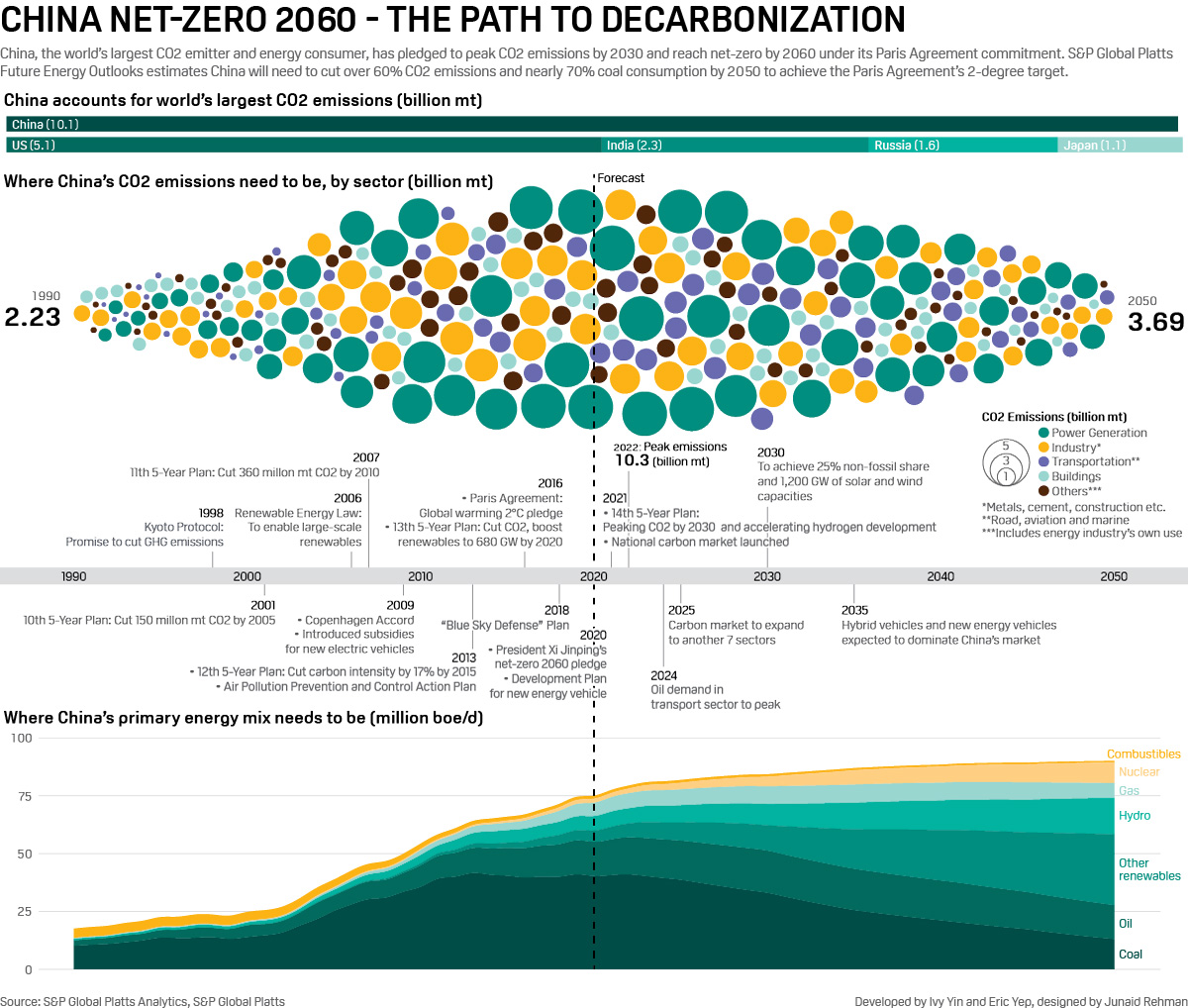

Key targets in China's 2030 carbon peaking action plan

|

Key Performance Indicators |

Targets |

Target Year |

|

Energy intensity (Energy consumed per Yuan of GDP) |

Reduced by 13.5% from 2020 level |

2025 |

|

Carbon emission intensity (CO2 emitted per Yuan of GDP) |

Reduced by 65% from 2005 level |

2030 |

|

Renewables' share in energy mix |

25% |

2030 |

|

Total solar and wind capacity |

1,200 GW |

2030 |

|

New hydropower capacity |

80 GW |

2030 |

|

Total storage using new technologies |

30 GW |

2025 |

|

Total pumped hydropower |

120 GW |

2030 |

|

Primary oil refining capacity |

Capped at 1 bil mt/year (20 mil b/d) |

2025 |

|

Utilization rate of refining facilities |

Above 80% |

2025 |

|

Total oil consumption for land transport |

Peaked |

Before 2030 |

|

Aviation and shipping |

40% of new vehicles by clean energy |

2030 |

Source: State Council of China

The decarbonization process clearly wont be limited to the power sector, with the refining and petrochemical sector expected to be covered as early as 2022-2023, in a move that will bring China's national oil companies — which are some of the world's largest oil and gas producers, importers, refiners and distributors — into the carbon fold, and cover a large segment of the petroleum supply chain.

The action plan to peak carbon emissions before 2030 announced by the State Council, the country's top executive body, on Oct. 26, outlined measures for major sectors on the path towards carbon neutrality.

It includes formalization of curbs on coal consumption growth by 2030, capping oil refining capacity at around 20 million b/d by 2025, achieving peak oil consumption for land transportation by 2030 and including hard-to-abate industries like steel and metals for the first time

Meanwhile, China is rapidly building up its manufacturing capacity for hydrogen electrolyzers, which is expected to reach 1.5-2.5 GW in 2022, to cater to increasing orders from both domestic and overseas customers.

Several private sector companies are formulating plans to leverage China's manufacturing expertise to lower the cost of equipment used in the hydrogen supply chain and produce electrolyzers, which crack the water molecule, at less than half of the cost of overseas manufacturers, the executives said.

Bringing down supply chain costs will help commercialize large-scale green hydrogen production and Chinese manufacturers are keen on replicating their dominance in global solar panel production in the race for hydrogen.

China's Sinopec has started the construction of the world's biggest solar-based green hydrogen plant, a 20,000 mt/year capacity project in Kuqa, Xinjiang Uyghur Autonomous Regions and is expected to commission the plant and start production in June 2023.

This will be one of Sinopec's four green hydrogen projects that are in the pipeline. China has been boosting its hydrogen development plans and Beijing is expected to release it hydrogen industry development plan soon.

China's hydrogen-powered fuel cell electric vehicles are expected to be cost-competitive by 2030 with conventional vehicles powered by gasoline or gasoil, in terms of both the purchasing price and the fuel cost.

Fuel distributor Sinopec Marketing expects that by 2025 green hydrogen will cost lower than Yuan 30/kg (approximately $4.69/kg) and hydrogen-powered trucks' fuel cost will be competitive against gasoil-fueled ones. Current hydrogen fuel costs range around Yuan 40-70/kg (approximately $6-11/kg), which is still significantly higher compared with diesel and petroleum costs.

Chinese policymakers already consider the energy transition to be as important as its emergence from economic isolation and the opening up of the Chinese economy, and expect the green economy to drive the next industrial revolution.