29 Jun 2021 | 11:00 UTC — Insight Blog

Fuel for Thought: Oil demand optimism bittersweet for global refining industry

By Paul Hickin and Elza Turner

The oil refining industry could struggle to return to full health in the next couple of years as analysts predict that the oil demand recovery enables new plants to start outpacing closures bringing extra capacity to the beleaguered sector.

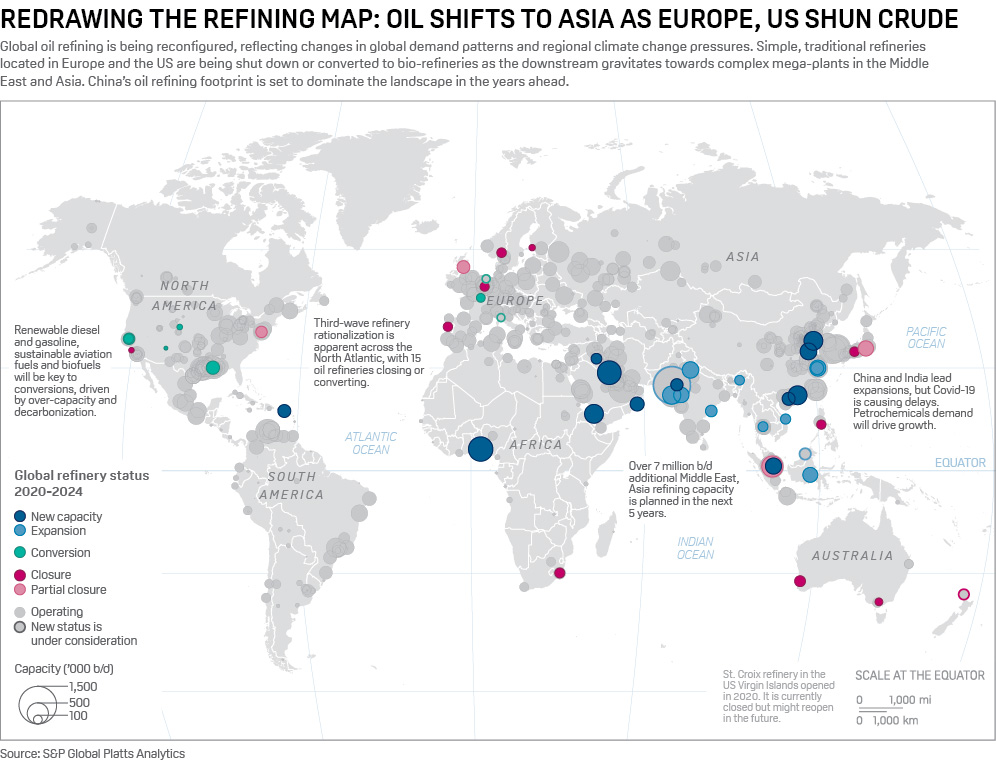

The downstream sector has undergone a metamorphosis. Over the past 18 months a COVID-19 led demand collapse has seen a spate of North Atlantic refiners start to go green or shut down and several Asia and Middle East refiners put plans on hold. The pressures of low margins and new cleaner energy strategies sharpened already emerging trends.

Limetree Bay's recent closure of a 200,000 b/d refinery in St. Croix, US Virgin Islands, shortly after starting it up, is the latest high-profile casualty.

Meanwhile, TotalEnergies is looking to turn its Grandpuits plant in France into bio-refinery, after converting another one - La Mede - few years ago. And Phillips 66 plans for its Rodeo, California, oil refinery to become the world's largest renewable fuel facility.

But that rationalization may not be enough. Even with predictions that global oil demand could far exceed 2019 levels by the end of next year.

Middle East-Asia nexus

Across the Middle East, Asia and even Africa plans to bring on additional refining capacity remain on track, even if some have been delayed by the ill effects of the pandemic. These regions are still unwavering in their focus on turning crude into transport fuels and petrochemicals amid continued urbanization.

S&P Global Platts Analytics estimates almost 3 million b/d of cumulative refining capacity will return by the end of 2022 (versus the end of 2019), noting a sharp turnaround after closures outweighed additions in 2020.

"Global refinery runs are increasing toward 2019 levels, but utilization rates will lag as new refinery capacity growth outpaces closures," Platts Analytics added.

China is leading the way in net additions, which include the second phase of Zhejiang Petroleum & Chemical complex and expansion of the Zhenhai refinery, and commissioning of the Yulong Petrochemical and Guandong Petrochemical and Shenghong Petrochemical complexes. China alone could add more than 2 million b/d in the next couple of years, according to some analyst estimates.

Elsewhere, the 400,000 b/d Jazan, Al-Zour and 230,000 b/d Duqm refineries in the Middle East and the 650,000 b/d Dangote refinery in Africa are due for commissioning in the next two years.

Utilization challenge

"Refiners that have braved the pandemic impact so far by cutting run rates and shutting down parts of their sites will eventually have to decide on whether they can return to normal operations or not," the IEA said in its June oil market report.

With global utilization rates forecast to reach "only" 78% of capacity in 2022, there remains a "high likelihood" of further closures, it said.

Platts Analytics notes that while refinery runs have been creeping higher amid the closures, utilization rates are likely to stay low for the foreseeable future, especially in Europe. Indeed, while many stocks of oil products have been returning to balance, there remains a glut in middle distillates as the recovery in transportation fuels make an uneven and pandemic-riddled recovery.

This balancing act will likely continue through the decade, with analysts suggesting more than 7 million b/d in refining capacity could come online in the next five years across the Asia-Middle East nexus, focusing especially on increased petrochemicals demand and putting further pressure on older, more traditional refineries.