05 May 2020 | 22:26 UTC — Insight Blog

Did Gulf Coast crudes go negative on oil’s most historic day?

Featuring Matthew Eversman and Laura Huchzermeyer

When one of the world’s most prolific oil futures contracts plunged deeply into negative territory April 20, S&P Global Platts’ pricing team was faced with the question of whether physical crude outside of Cushing, Oklahoma was also worth less than zero.

With no ambiguity, Platts' methodology answered with a resounding “no”. With the exception of May WTI at Cushing, Platts did not assess any North or South American crudes at negative values that day.

CME Group’s NYMEX Light Sweet Crude Oil Futures contract, known as NYMEX WTI, is the world’s most liquid and actively traded oil contract and has long been regarded as the de facto pricing benchmark for a plethora of crude grades with various qualities and locations around North, Central and South America.

But May NYMEX WTI collapsed on April 20, settling at a record low of -$37.63/b. That settle price and the events that led to it exposed some major cracks in the system – raising some important questions about how crude oil is priced in the Americas.

However, three key pillars of Platts’ methodology led to assessments that day that reflected tradable value for physical oil at key distribution hubs outside of Cushing – values that in Platts’ view were not negative.

Firstly, Platts prides itself on applying a consistent approach to daily assessments, which includes independent, data-driven judgment in “how to normalize data and where to assess final value subject to review by Platts’ editorial management.”

Next, Platts’ methodology gives precedence to outright prices over differentials, so – all else being equal – a collapse in the futures contract should not pull outright values negative. “In the event of an observed conflict between outright values and differentials, outright values prevail in Platts’ final published assessments,” states the Methodology Guide.

Lastly, Platts Market on Close assessment process tracks bids, offers and trades over the course of the day to help determine the value of crude oil precisely at 1:30 CT. The assessment of physical crude is synchronized with the NYMEX contract settlement, so Platts’ differentials could fully account for – not lag – the negative settlement value April 20.

Technical, fundamentals factors lead to collapse

On April 20, the world was a few months into the devastating coronavirus pandemic and economies were reeling from the effects. For the oil and energy markets coronavirus created world-wide demand destruction with fewer people driving and taking flights. That shot to demand had already sent oil prices very low and storage hubs, including Cushing were filling quickly.

It was also one day before the May NYMEX WTI contract expired, which added a critical technical element to that particular trading day. The NYMEX WTI contract is physically deliverable at Cushing – a major pipeline and storage hub. However, with weakening demand for crude, storage in Cushing was near capacity. May contract owners who could not take physical delivery of oil needed to sell, but were having a hard time finding willing buyers.

By the Singapore close that day May NYMEX WTI had fallen to $14.24/b. At the London market close it continued to fall, hitting $10.44/b. By mid-day in Houston, the contract was hovering slightly above zero. At 1:08 pm CT WTI went negative and for the next 22 minutes continued to fall before settling at -$37.63/b.

Deals point to positive outright values

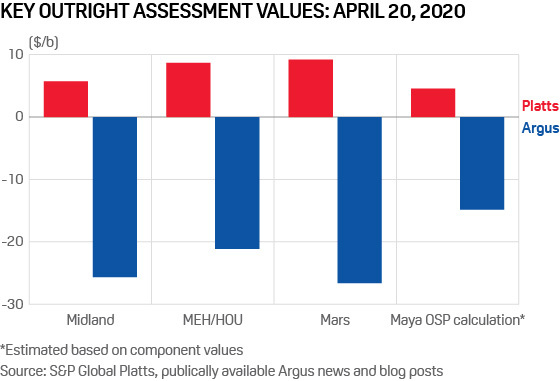

May NYMEX WTI was clearly negative at market close, and with no market information calling for a significant Exchange of Futures for Physical (EFP) value, so was “Cash WTI.” However, Platts’ crude pricing team did not identify any trades for Gulf Coast crudes that day with negative outright values. And with NYMEX WTI falling so fast in the last 20 minutes of trading it was impossible for crude differentials to keep pace with the falling benchmark.

So Platts focused on a trade for WTI at the Magellan East Houston terminal done at about 12:40 CT at a $7/b premium to the front-month contract. With May NYMEX WTI at $2.55/b at the time, the trade implied an outright value of $9.55/b.

A trade for Light Louisiana Sweet was done with a similar timestamp at a $10/b premium to WTI. Platts was also reported trades for sour crude Mars at WTI plus $7.75/b and plus $7.50/b before NYMEX WTI went negative.

Those Gulf Coast trades showed positive outright values, but applying the observed differentials to the closing NYMEX WTI value would have called for massively negative assessments. In a collective decision with input from senior leadership, it was decided that in this case Platts’ methodology called for outright values to take precedent with differentials a secondary calculation.

Time-adjusting values without NYMEX WTI

With pre-futures crash deals pointing to modestly positive values, Platts still needed to account for the change in price for the last 50 minutes or so of the trading day between the trades and Market on Close.

Platts determined that with the technical factors and volatility in NYMEX futures that afternoon the NYMEX values were not suitable for time-adjusting the value of physical crude outside of Cushing. Instead, Platts opted to use ICE Brent given its status as a barometer for global crude values and because of Gulf Coast WTI’s ties to the export market.

June ICE Brent declined 86 cents/b over the 50 minutes between the previously mentioned WTI MEH trade and the Market on Close.

Adjusting the prices of trades earlier in the day for the movement in ICE Brent provided final outright values for Platts’ assessments. In keeping with Platts’ stated observance of outright prices over differentials in times when the two conflict, the assessed differentials reflected the difference between the outright assessments and the settlement—not the differential value observed earlier in the day before the huge, sudden drop in WTI.

Crude VWAs vulnerable to pricing basis volatility

In recent years, much of the crude oil pricing in the US has relied on NYMEX WTI paired with Argus Media’s volume-weighted average derived differential assessments of physical crude at key trading hubs.

This approach pairs a trading day volume-weighted average differential with a day-end futures contract settlement to arrive at an outright value. As long as the NYMEX contract does not have a big flat-price move close to settlement time, the average of the traded differentials should align reasonably well with the settlement value. In a highly volatile market, this rigid approach can run into problems.

When NYMEX WTI collapsed some $40/b in the last 20 minutes before the close, it showed what can happen when the futures contract divorces from the average of the differentials traded earlier in the day: negative assessments for physical crudes hundreds of miles from Cushing.

Argus summarized this dynamic in a news story documenting its April 20 assessments: “Many Argus volume weighted average prices largely went negative as differentials of deals struck earlier in the day lagged the afternoon descent of the futures price.”

In this case, adherence to a formulaic assessment approach may have led to assessments that did not reflect the tradeable value of crude around the Gulf Coast.

That scenario might be okay for a market participant that had hedged their exposure to both the NYMEX contract and the differential, but a crude seller with either side unhedged or naked exposure to the outright price might have been on the wrong side of this historic event.

Methodology in times of market stress

The impact of a severely negative NYMEX WTI settlement and negative Gulf Coast physical assessments will continue to reverberate during the current market turmoil and beyond.

While the NYMEX WTI plunge below zero proved to be short lived, it can’t be written off as a one-day phenomenon. The potential for changes in differentials to “lag” futures values is here to stay, and the risk of futures volatility continues to grow with stressed fundamentals and financial market participation in this physically deliverable contract.

This market event has raised concern about exposure to the conventional US oil pricing mechanisms, particularly for the growing volume of crude exports from the Gulf Coast. The event has spurred some crude oil producers, refiners, and other traders in the US market to explore alternatives for pricing barrels, including fixed price.

Methodologies will continue to be tested in times of stress, and when this happens, the events of April 20 show the importance of combining data and independent judgment to determine market value.