22 Apr 2020 | 20:43 UTC — Insight Blog

Insight Conversation: Jeff Currie, Goldman Sachs

By Paul Hickin

Jeff Currie, head of commodities research at Goldman Sachs, spoke to Paul Hickin shortly before OPEC+ revived an agreement on output cuts, and oil prices spiraled to unprecedented lows. This is an extract from their conversation, which ranged over the impact of coronavirus on oil, gas and LNG, metals and more.

With the cuts in capex and crude oil production shut-ins, could we see a sharp rebound at some point?

It’s important to emphasize that when you shut in oil production, it’s very different from shutting in, let’s say, a manufacturing process. It’s going to take time to bring it back online. We don’t know what happens when you shut in this much shale oil, you may have to re-frack a good portion of them, or in the case of older, mature, smaller reservoirs, you do permanent damage requiring redrilling. It all takes time.

So the way I describe it is the supply story is likely to be L- shaped, the demand story is likely to be V-shaped. For the demand to recover, we simply go out and drive driveways and get into our cars and start driving again.

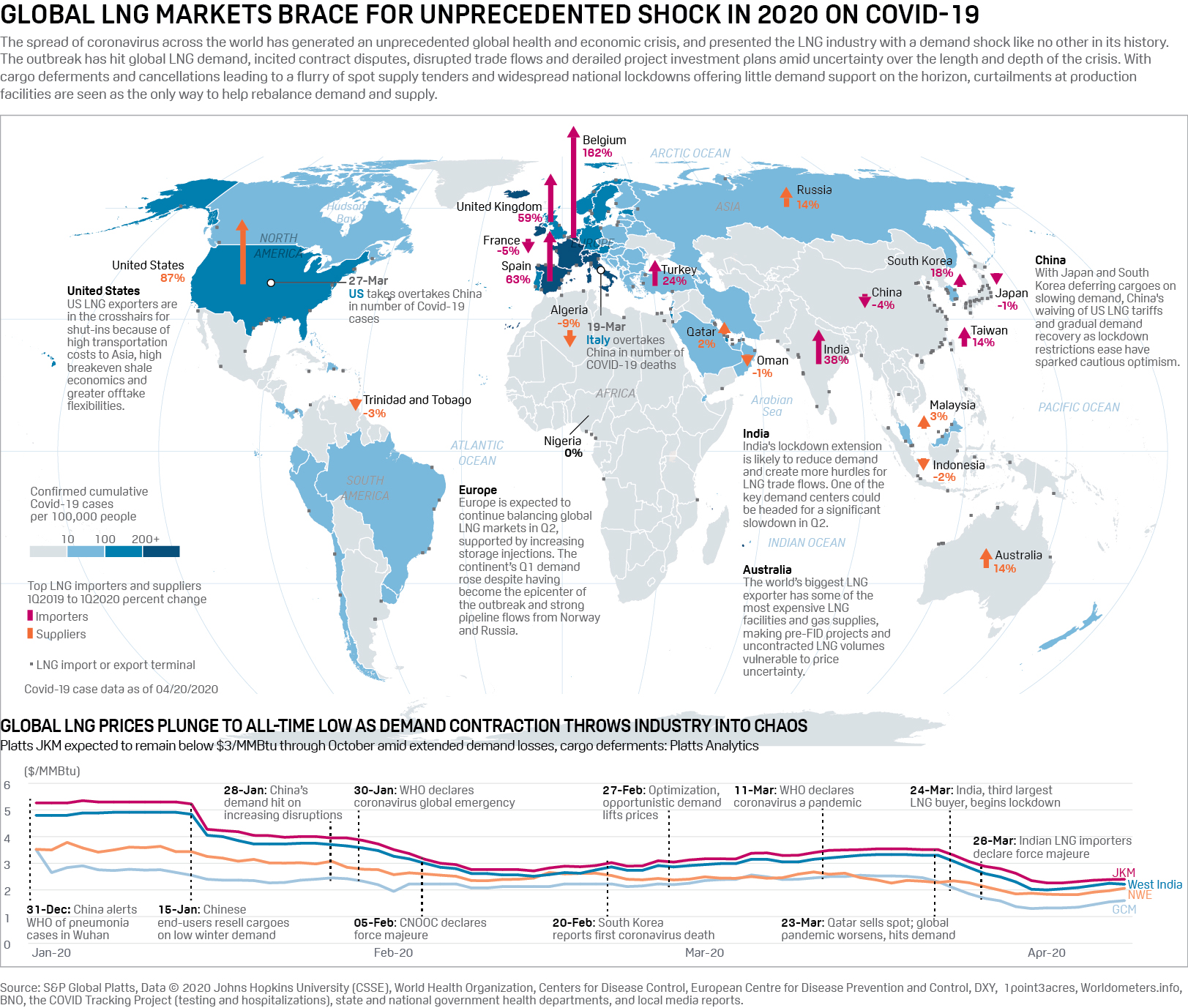

Go deeper: Listen to the extended interview in S&P Global Platts’ Commodities Focus podcast

And the other thing to think about oil, when we think about the damage to demand, oil sits in the crosshairs of the current corona crisis. Why is that? It’s because [when] we look at oil, it really creates social contact as well as globalization. And what are the two things we’re trying to stop right now? Social contact and globalization.

Therefore, when you look at the hit to oil demand, it’s likely two times or even two and a half times that to economic activity, which is why when we start to repeal these social distancing measures it’s likely to create a very V-shaped recovery in demand. Now a lot of you probably are asking, what is the permanent damage to demand?

There, I think there’s two issues, around commuting, and air travel. Commuting represents roughly 8 million barrels per day. Let’s say people decide, I like working from home one day of the work week. So instead of commuting for five days they commute four days, which would be roughly a 20% hit to that 8 million barrels per day. And that would probably be your limit on it.

But I think the key point here is that it’s not as substantial as you might think. Turning to the jet component. That’s another 8 million barrels per day. That one, the leisure component won’t be touched. Actually, there, you could see a surge in the leisure component of jet travel, given the fact nobody is taking any holiday right now, and we’re all working incredibly hard.

But I think the issue that potentially could be lost here really has to do with the business travel. The question about, will we get in plans and travel out from here in London to some place like Los Angeles, it starts to become a much larger question. So instead of one trip every quarter, are people going to be doing one trip every year? That’s the part that I would argue is the most notable. But then again, how much of that 8 million barrels per day, maybe it’s a couple of million barrels per day. So it’s not this catastrophic gloom and doom backdrop that I think people are concerned about.

Will [demand] rebound to 100 million barrels per day immediately? The answer is no. But will it rebound above 85 million or 90 million barrels per day, it’s extremely likely.

With the decimation of oil demand, where else can oil go?

The only real outlet that I can envision would be some type of strategic petroleum reserves. Now the problem in the US is you’ve got roughly 77 million barrels available, of which 30 million has already been leased out.

And then when you look at China, maybe another 100 million barrels. They talked about taking their overall coverage from 90 to 180 days, but I think the real key issue there is that they’d have to build it. Now with China, that can erect a hospital essentially overnight, building that strategic reserve could be rather quick for China.

But why is that storage capacity so critical? The example I like to give is, let’s look at metals, and what have we learned about metals during the slowdown of Wuhan in China during February? They did not shut down those steel mills, aluminum smelters or anything – why? because it takes time to bring them back online. The demand can drop and come back real quickly but not the supply. With metals, all you need is a parking lot, a chain link fence and maybe a guard dog to protect the metal, and you’re good to go, you can just stack the stuff to the moon, which is essentially what we did. If you look at the inventory piles and steel in China, they’re astonishing.

Energy, you cannot do that, because it must live within the pipelines, the storage facilities, the refineries processing facilities and so on down the line. That’s what distinguishes energy from all other commodities. And that’s also why they’re far more volatile. But what it tells you is that you cannot run a surplus and definitely [not] like you can in steel. And as a result, you get the shut-ins. And the shut-ins are what creates that bullish story as we begin to look out towards the end of next year and beyond, because it’s just going to take time to bring on that production.

So the key point here is avoid the shutdown. How can the G20 avoid the shutdowns? Create storage capacity so you don’t breach infrastructure capacity constraints.

With global gas prices at record lows, do you think producers will have to curtail production? If so, which producers would act first?

Absolutely. We’re already beginning to see that. And most of it’s going to come from the associated gas in the United States, meaning the gas that comes off of the oil production. In fact, one of our more bullish calls across commodities is for calendar 2021 US natural gas to reach $3.30.

And really driving that view is the reduction in supplies that are associated with the potential shut-ins on the shale production. So that would be one area in which we see a significant risk to supply and hence, global LNG supply. We’ve already seen Cheniere tender for LNG cargoes closer to Europe to be able to meet its contractual need to avoid having to load LNG in the US. Which tells you, we’re likely to start to see problems in the US going forward.

Click for full-size infographic

Again, like the oil story, we still have some downside risk, we think [there would be] $0.10/mmbtu of near-term downside supply or price risk. But again, the shut-ins start to create a much more bullish story further out. Looking beyond the US, the other two big marginal suppliers into the European markets are Norway and Russia.

When we saw the price for oil develop back in early March, we like to point out It wasn’t just a price war around oil. There was also a price war around gas because the European market has been the central point of the dumping ground of excess gas supply everywhere. We look at the LNG demand in China, it dropped by 40%, as you saw the Chinese economy shutdown around the coronavirus. That excess LNG went into the European market.

You look at US LNG, it gained market share from 1% to 7%, and this started to create excess supplies in Europe. In all my career, I never saw JKM or the equivalent of it before there was a JKM, where gas prices in Asia were traded at a discount to Europe. And we saw that beginning back in March as those excess supplies began to mount. So there is going to be a lot of pressure on production in Europe. The biggest candidate there would be Norwegian supplies, particularly as they go down for maintenance in the May time period. So those would be the two big candidates we’d be focused on.

Will the current crisis accelerate the move away from fossil fuels?

The demand side, yes, the supply side, it will actually slow it. It goes back to my point that carbon-based or unsustainable industries sit at the center of social contact and globalization.

We’ve talked about airlines, autos, cruise lines, and it’s not just the oil side. The auto sectors are getting – they’re down to 75%, 85% in terms of output. So it’s not just oil that’s likely getting hit here. It’s also autos, aircraft and so forth.

When we look at other industries, though, take beef and livestock – 50% of beef demand is in restaurants. And as many of you know here in London, the restaurants aren’t open, similarly to many other parts of the world. So we’re seeing a significant drop in the demand for livestock, which is foreseeing many animals to be slaughtered, which is going to be bringing the same question about, do we redrill these wells? Do we go back and rebuild the livestock herds? all this stuff takes time, the average livestock herd can take upwards of 20 to 24 months.

Let’s think about fresh food. What does fresh food required? Migrant workers as well as jet aircraft, both of which are in short supply right now. And as a result, people are eating less fresh food or locally grown food. So we’re forcing that energy transition or let’s say sustainable transition, on the demand side right now, and a lot of it will probably stick in terms of us changing our behaviors and so forth.

The supply side is going to be difficult. The technology is not ready to replace all of the world’s, airplanes and cars, with other types of technologies like EVS. And we just don’t have the technology to replace the aircraft. So we’re going to be stuck with the question, do we rebuild these fossil fuel-based transportation sectors after this and increase drilling for fossil fuels? I tend to think we’re going to have to, which means they’ll bring up the whole question of ESG. We have a lot of divestiture going on in many of these companies, which is going to make it incredibly difficult to make the investments that are going to likely be needed on the other side of this.

So I know that’s not a straight answer. By the way, I think on demand, we’re going to make a lot of progress. And I think it’s going to be a lot of positive progress. The problem on the supply side is the technology is not there. And the worst thing about it if we do put resources into fossil fuel-based technologies it’s going to divert resources from other types of technologies that can help solve the climate change problem. So it’s two different worlds there. One positive, one is negative. I don’t want to venture what the net’s going to be right now. I think it’s important to keep in mind, I think your question is critical. The climate change debate is going to have to change going forward.

What areas of opportunity do you see around for commodities? Are there particular niche areas that may benefit from as we come out of the crisis?

Let’s talk about what does gold hedge, and what does oil hedge. Oil is the best hedge against inflation, not gold. Gold is a hedge against debasement. The difference is subtle, but very important. Debasement is when a country prints a lot of money and they debase the currency, it leads to a decline in real interest rates. Debasement may or may not lead to inflation, but it will lead to the increased value of gold because gold is basically the currency of last resort. As you print too many dollars or pounds sterling or euro, the value of that pound sterling or euro or dollar goes down. As it glows down, the opportunity cost of holding something like gold that has a negative carry, because you got to store it, starts to go up and then gold prices go up.

When we think about oil, oil is a hedge against inflationary pressures. In fact, I like to point out the best hedge out there for inflation is oil, not gold. And the reason why the only thing moving in our consumption basket is oil is that it’s highly correlated, through the currencies to everything else in our consumption basket.

In contrast, gold is that hedge against debasement. One thing we know without certain economies around the world are debasing the world’s fiat currencies.

That’s just indisputable, which is why on the medium to longer term, our favorite trade right now would be long goal. Our target is $1,800 an ounce, but we’d argue there’s a lot of upside risk to that.

What are some of your final thoughts?

I want to go back to the point that these industries were in high need of restructuring, consolidation and restructuring our balance sheets. And going back to my point that assets don’t go bankrupt only balance sheets and management teams.

If you look at the US, the top five companies in the US by market cap produced 20% of the shale. The other 80% of the shale were produced by the bottom of 50-plus.

That’s an indication you had too many producers that were doing this uneconomically. In fact, I think one of the biggest causes of this really had to do with the production cut decision that OPEC+ initiated in December 2016. It kept prices artificially high in an unsustainable environment. This cost not only the OPEC countries, we estimate, $220 billion in lost revenues per year, but it also costs the debt in equity shareholders at least $1 trillion over this time period. Why? Because there was not a sustainable future. You add that with ESG, we had a problem.

Our outlook for both oil and metals and everything at the beginning of this year was titled “overbuilt, over-levered and over-polluted”. Overbuilt means we just had too many players in the market. The over-levered was too much debt, so the cash flow is having to pay down the debt. And then we had over-polluted, that it was at the center of the climate change discussion. So it needed to deal with these problems. And what’s likely to come out of this is an acceleration in forced restructuring, consolidation, rationalization of the assets, which I think are ultimately very much needed.

And if we think about who are going to be the losers. The losers are going to be those marginal players, highly levered ones. They’re dealing with incredibly low oil prices. They’re likely to restructure. The other ones are going to be producers that are landlocked behind thousands of miles of pipeline that have congestion, to get into their offtake agreements. As a producer, having an iron-clad offtake agreement is critical right now to be able to survive this.

The winner is going to be those who are still producing. And when we see that chart be rebound in gasoline demand as people go out, start driving again, you want to be one of the producers that are producing because that’s going to make in the winner in this environment.

So I’m looking at this, I think no, there’s a lot of winners. There’s going to be a lot of losers here. But ultimately, the big winner will end up being these industries. They will get the restructuring that they need. You will take a lot of the, let’s call it, ineffective, inefficient producers out of this market, which will lead to much higher returns.