12 Mar 2020 | 22:06 UTC — Insight Blog

China reopens its doors to US LPG, but path to recovery may be slow

After an eighteen-month hiatus, Chinese liquefied petroleum gas (LPG) buyers are peering west again, as the country looks to the US to fill its burgeoning import demand.

Propane and butane, key feedstocks for plastics and synthetic rubber, were hit hard by the prolonged trade spat between the US and China, which resulted in tariffs across a raft of raw materials and manufactured goods.

Resumption of US-China trade flows has been the talk of the Asian LPG market since March 2, as Beijing started accepting applications for tariff exemptions on 696 US-origin goods – including crude, LNG and refined products such as LPG, in a move that will allow it to meet purchase targets under the US-China trade deal.

US LPG shipments crushed by tariffs

Chinese buyers halted imports of US LPG in August 2018 after the government imposed retaliatory tariffs on US imports, including propane and butane, following the US' implementation of 25% tariffs on an additional $16 billion worth of Chinese imports from August 23 that year.

Chinese tariffs on US LPG currently stand at 26% for propane and 28.5% for butane, according to China’s Ministry of Finance, after China cut butane tariffs on February 14 by 2.5 percentage points, from 31% previously.

In 2017, before the imposition of tariffs, the US was the second-biggest supplier of LPG to China, totaling 3.54 million mt, comprising 3.37 million mt of propane and 162,668 mt of butane.

The volume shrank by 54% to 1.62 million mt in 2018 due to trade tensions and in 2019 only 2,443 mt of US propane was imported, customs data showed.

To mitigate the loss of US-origin material, Chinese propane dehydrogenation (PDH) plant operators including Wanhua Chemical and Oriental Energy have proactively sought to diversify their LPG supply sources over the past two years, notably committing to several long-term contracts with Middle Eastern producers. They have also increased imports from Africa and the North Sea.

Traders eye US LPG again

Following Beijing’s announcement on February 17 last month to start accepting applications for waivers, most Chinese LPG buyers have told S&P Global Platts they were preparing documentation to apply for tariff exemptions on US LPG for the March loading cycle.

A number of these companies have since received approval for tariff exemptions, some as early as March 3, including Oriental Energy, Wanhua Chemical and Zhejiang Satellite, according to trade sources.

Other Chinese LPG importers were expected to follow suit, given they currently have to pay at least $10/mt more for Middle East spot cargoes over US LPG, trade sources said.

Although on the surface any sensible Chinese importer would be applying for exemptions right now, resumption of US-China trade flows is expected to be gradual as the market grapples with the exact mechanism of the tax waiver, and demand destruction from the ongoing coronavirus pandemic.

There remains a great deal of uncertainty as to what system will be used to issue tax exemptions on US imports. The current application is only for March and April deliveries, while subsequent quotas will have to be applied for on a monthly recurring basis, at the start of each preceding month.

There were suggestions from trade sources of a banking system for unused import quotas, to allow them to be stored for use later on. However, this was by no means definitive and could discourage importers from applying waivers in the short term.

It is not immediately clear if entities will be permitted to trade or exchange their unused import quotas, or whether these will simply be allowed to expire at the end of the time period.

This could put off companies who were planning on running new PDH plants this year from applying waivers on US imports – they may now defer these plans due to poor PDH margins from the impact of coronavirus.

Long-term impact on LPG prices

So far, there has not been a major impact on prices resulting from tariff exemptions, with many traders remaining cautious.

A trader pointed out that Chinese end users were still willing to pay a premium of $40-50/mt over the Saudi Contract Price for April spot arrivals from the Middle East, a sign that demand remains healthy in the near term for Middle East origin LPG among Chinese importers.

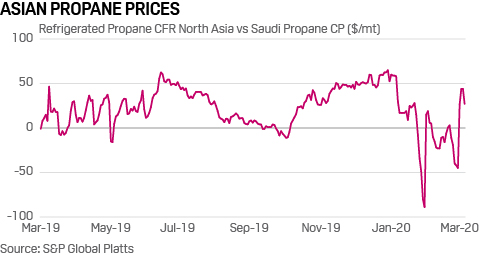

The spread between Platts CFR North Asia refrigerated propane cargo and Saudi Aramco contract price (CP) swaps averaged minus $12.23/mt for the month of February, indicative of the strength in Middle East market versus the Asian CFR market.

The spread has since flipped back into positive territory going into March, S&P Global Platts data showed.

The longer-term impact on pricing is probably too early to determine, as Chinese importers are still coming to grips with the new exemption system. Some traders have questioned whether US-origin LPG would possibly be preferred to Middle Eastern material, given the state’s obligation to increase US energy imports under the phase 1 trade deal, all other things being equal.

If that happens, it is not hard to envisage Chinese importers asking for a discount on Saudi Aramco CP for Middle East cargoes, as opposed to the big premiums they were paying last year.

Coronavirus weighs on Asian demand

On the other hand, Chinese LPG demand has been low since end January, with both the residential and petrochemical sector consumption dampened by measures to contain the spread of coronavirus, which nearly halved China’s LPG imports in the first two weeks of February versus the February 2019 average.

This has also raised market concerns that it could prompt Chinese importers to seek deferral on term arrivals, or force them to re-offer these cargoes in the spot market, should the situation persist through April.

Elsewhere, there were concerns that the recent surge in coronavirus cases reported in both Japan and South Korea would put a huge dent in demand from Asia's largest and second-largest importers of US LPG respectively, effectively closing the arbitrage for US exports into Asia.

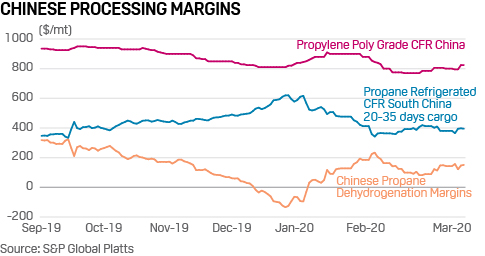

LPG demand from Chinese PDH plants has been lackluster in the first quarter of Q1 2020 as margins shrank and downstream polypropylene (PP) prices fell ahead of the Chinese New Year holiday in January.

While PDH plants enjoyed a good run last year, margins have averaged just $22.28/mt over December to January, S&P Global Platts calculations showed. Industry sources surveyed estimate that pressure from high PP inventory in China will alleviate only in the second half of 2020. Until then, PDH margins will likely be subdued.

Chinese demand for LPG, however, is expected to recover in the coming month, with renewed buying interest from end-users heard for April-loading cargoes as the lockdown on some Chinese cities has been relaxed and more workers are returning to work.

Traders last week have estimated LPG imports into west China to total 1.4 million-1.5 million mt for April compared to just 1 million mt for March, early signs that recovery may be around the corner.

As trading on April delivery LPG cargoes started last week, Middle East-origin LPG is expected to continue making up the lion’s share of Chinese LPG imports in the near term. However, higher premiums commanded by these cargoes, in addition to a reduction in demand from other major Asian importers, could see a gradual increase in US LPG shipments to China in the coming months.