S&P Global — 21 May, 2020

COVID-19 Daily Update: May 21, 2020

By S&P Global

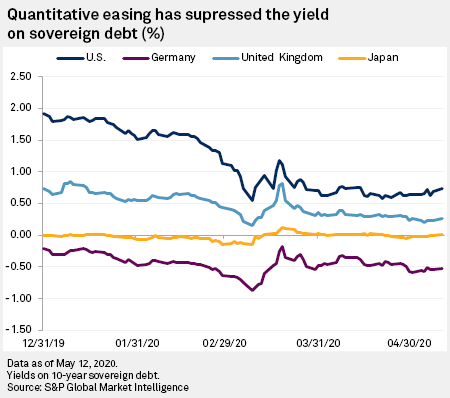

The role of central banks in society has been transformed in months as the coronavirus pandemic froze economic activity and turned the heat up on companies and countries’ access to liquidity. The U.S. Federal Reserve, European Central Bank, and other monetary policy authorities are providing immediate stimulus relief to enterprises and markets during the current downturn. As assets on the balance sheets of the Fed, ECB, Bank of England, and Bank of Japan near $20 trillion, the coronavirus pandemic could alter the ways in which central banks support economies.

Fed officials expressed concerns about the “substantial likelihood of additional waves of outbreak in the near or medium term” that would unfurl “further economic disruptions, including additional periods of mandatory social distancing, greater supply chain dislocations, and a substantial number of business closures and loss of income” and ultimately “lead to a protracted period of severely reduced economic activity,” according to minutes released yesterday from their April 28-29 policy meeting. “In this scenario, a second wave of the coronavirus outbreak, with another round of strict restrictions on social interactions and business operations, was assumed to begin around year-end, inducing a decrease in real GDP, a jump in the unemployment rate, and renewed downward pressure on inflation next year.”

Breaking from the consensus of some of his central bank colleagues, James Bullard, leader of the St. Louis Fed, said yesterday that he is “relatively optimistic about the second-wave scenario because I think we are not naive about that” and that “we are more or less on track for where we would have expected to be at this point” due to aggressive policy responses. “We have every chance of a good recovery in the second half,” Mr. Bullard said during a virtual Missouri Growth Association event.

According to S&P Global Market Intelligence, the Fed’s goals are more closely aligned to those of the U.S. government now than in recent years. In order to support the U.S.’s recovery from the coronavirus-caused downturn, the central bank has announced an open-ended government bond purchasing program and the Treasury needs to issue unprecedented amounts of debt to support $3 trillion of government spending commitments. Such extraordinary actions from the Fed may test the independence of the central bank in the long-term if and when policymakers need to regulate inflation against the potential fiscal repercussions of greater government borrowing costs.

A similar situation exists in the U.K. On March 11, when the Bank of England cut rates on May 11 to 0.25%, the British government pledged a $39 billion fiscal stimulus package just hours later. One week later, the BoE announced it would resume its quantitative easing program to the equivalent of approximately 9% of the country’s GDP and further cut rates to 0.1%. As “the measures being taken to contain the virus will result in an economic shock that could be sharp and large, but temporary,” the BOE said in the statement at the time, “the role of the Bank of England is to help to meet the needs of U.K. businesses and households in dealing with the associated economic disruption.”

On May 20, the U.K. sold its first-ever government bond with a negative yield, prompting investors to pay to lend capital to fund the government’s coronavirus response. The Debt Management Office’s auction sold three-year gilts worth £3.8 billion ($4.66 billion) at a 0.003% negative yield. BoE Governor Andrew Bailey said yesterday in a parliamentary Treasury Committee meeting that he has “changed his position a bit” on negative rates and now believes it would be “foolish” to rule out slashing the record-low rates to negative. “We’re not ruling it in, but we’re not ruling it out,” he said.

U.K Chancellor of the Exchequer Rishi Sunak said on Tuesday that he is considering “what degree of long-term scarring is there on the economy” and said that “all economic forecasters and economists would agree the longer the recession is, it is likely the degree of that scarring will be greater.”

The ECB and Bank of Japan have already taken the plunge into negative rate territory. On April 30, the central bank in charge of monetary policy for the E.U.’s 19 member countries that have adopted the euro lowered its interest rate to negative 0.5%. The BoJ has maintained its target negative 0.1% interest rate during the crisis.

On May 18, Germany and France proposed a $549 billion coronavirus recovery fund, with capital to be raised through E.U.-backed bonds. German Chancellor Angela Merkel said at a press conference announcing the fund, which would add to the half-trillion dollars in emergency measures agreed upon by the bloc’s 27 leaders last month, that the current crisis “requires this unusual, one-off effort that Germany and France are now prepared to take.” Austrian Chancellor Sebastian Kurz said on Tuesday that Austria, Denmark, the Netherlands and Sweden, known as the E.U.’s “frugal four,” will propose a counter-proposal to the plan.

After speaking with the leaders of the International Labor Organization, International Monetary Fund, Organization for Economic Cooperation and Development, World Bank, and World Trade Organization yesterday, Merkel said that “the answer to the pandemic can certainly not be to renationalize all international supply chains now, then everyone would pay a very high price” as it is “clear that multilateralism faced a major challenge even before the pandemic, and this challenge has not become smaller.”

Considering that the principal task of central banks is to target inflation typically at around 2%, the increasing government debt ensures that any additional rate hikes by independent central banks to lower the money supply and encourage saving will likely increase the cost of the debt burden, S&P Global Market Intelligence reported.

The International Monetary Fund forecasted in its World Economic Outlook, published in April, that inflation in the U.S. will drop to 0.6% in 2020, from 1.8% last year, while the euro area and Japan are expected to see the rate drop to 0.2%.

“With interest rates at record lows and public debts at historical highs in many countries, how can advanced economies best prepare for and respond to future downturns?” IMF World Economic Outlook deputy division chief John Bluedorn and IMF African department economist Wenjie Chen wrote in a May 18 article. “Central banks may still use unconventional monetary policy tools more intensively—like large-scale asset purchases—to deliver additional support, as they have recently in response to the pandemic. However, relying on monetary policy alone to respond to shocks might not be enough and also raises questions about side effects on future financial stability and threats to central bank independence.”

Today is Thursday, May 21, 2020, and here is today’s essential intelligence.

Uncertainty Across the Global Economy

Funding COVID-19 debt splurge risks the independence of major central banks

"Now is not the time to worry about debt, but use the great fiscal power of the U.S. to avoid deeper damage to the economy." The statement by Federal Reserve Chairman Jerome Powell on April 29 marked the completion of an extraordinary reversal in the relationship between the Federal Reserve and the U.S. government. In December 2018, Powell appeared a paragon of central bank independence as he clashed with President Donald Trump and pushed up the federal funds rate to 2.25%-2.5% to keep a lid on what it perceived to be an overheating economy. Now, the goals of the Federal Reserve and the U.S. government are much more closely aligned. Treasury needs to issue unprecedented amounts of debt to support $3 trillion of government spending commitments to rescue the economy from its coronavirus-induced slump, while the Fed has announced an open-ended program of government bond purchases.

—Read the full article from S&P Global Market Intelligence

Germany’s Constitutional Court Complicates The ECB's Crisis Response

By potentially influencing future amendments to current asset purchase programs, the May 5 German Constitutional Court ruling on the ECB's Public Sector Purchase Programme may constrain the independence of the European Central Bank. Nevertheless, S&P Global Ratings’ baseline expectation is that the ECB will continue to counter below-target inflation and monetary fragmentation in all jurisdictions of the eurozone via low interest rates, liquidity injections into the banking system, and balance sheet-expanding asset purchases, mindful of the EU Treaty, but with a determination to purchase flexibly. Based on S&P Global Ratings’ current economic forecasts, the ECB response to this crisis is expected to widen. This could take the form of an extension of the PEPP in scope, size, or duration. Since April 13, 2020, S&P Global Ratings has affirmed ratings on Austria, Belgium, Spain, France, Germany, Italy, and Portugal. A key assumption in these affirmations was that under pre-existing and new initiatives, Eurosystem national central banks will purchase most of the sovereign debt newly created this year because of the COVID-19 pandemic.

—Read the full report from S&P Global Ratings

Economic Research: European Short-Time Work Schemes Pave The Way For A Smoother Recovery

The unprecedented use of short-time work schemes in the eurozone's largest economies has so far prevented a surge in unemployment, which rose only 0.1 percentage point in March to 7.4%. Given that 27% of Europe's workforce is now on short-time work, the schemes have clearly helped protect jobs and household income and will likely encourage consumption as lockdowns are loosened. Despite these measures, S&P Global Ratings still expects unemployment to rise to 8.5% in 2020. Short-time work schemes are also likely to cost less than unemployment benefits to governments as the burden of lower economic activity is shared with firms. Plus, the schemes allow for a quicker economic recovery because they keep workers tied to their firms—therefore maintaining the productivity of the human capital and avoiding a large, permanent rise in precautionary savings. However, phasing out short-term work schemes as the economy recovers will prove difficult because some sectors, like tourism and hospitality, are likely to see a much slower recovery.

—Read the full report from S&P Global Ratings

As automakers ease off investment gas, private equity could rehome some assets

The biggest risk to carmakers before the pandemic was simply that of standing still. One-time laggards in electrification, who dismissed it as unprofitable and impractical, have scrambled to incorporate hybrid and battery electric into their offerings as regulators turn against fossil fuels. Meanwhile, the big prizes of market leadership in shared mobility and self-driving cars are still up for grabs. Now, as the novel coronavirus pushes automakers into what Volkswagen AG refers to as "task force mode" to protect the health of their employees and balance sheets, spending sacrifices that could impact these innovations will need to be judicious if they hope to win the battle for survival without losing ground in the longer-term technological war.

—Read the full article from S&P Global Market Intelligence

The Future for Energy & Commodities

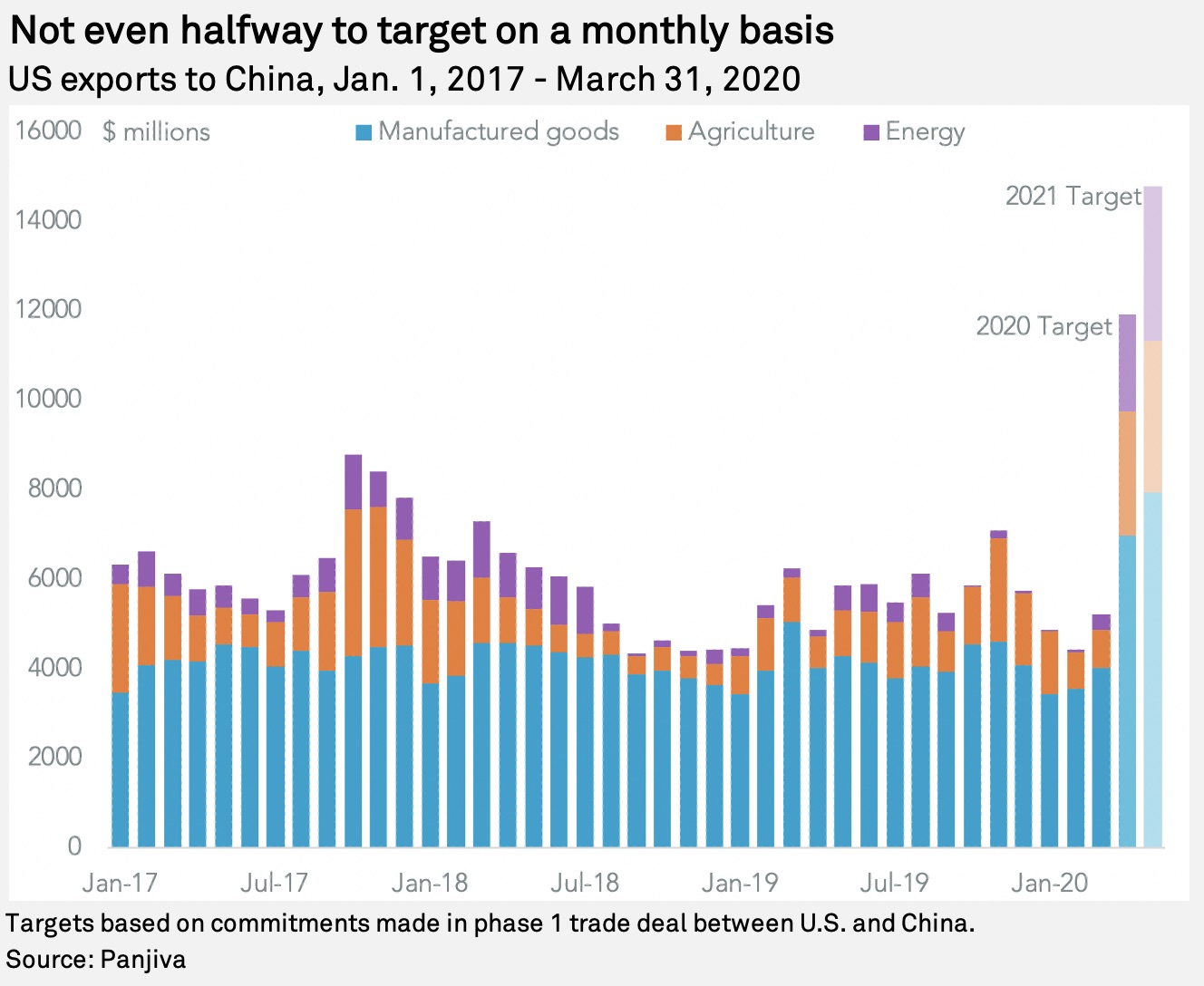

US LNG flows to China short of targets as outlook for trade deal grows bleak

Five tanker ships hauling U.S. LNG in March offered a rare bright spot for exporters staring down a brutal summer for the global gas market. The cargoes set out to be the first U.S. LNG deliveries to China in more than a year, made possible by tariff exemptions that followed an agreement between the two countries that was designed to help resolve an ongoing trade war. But deteriorating market conditions and another flare-up of geopolitical tensions between China and the U.S. — President Donald Trump has threatened new tariffs amid frustration with China over the coronavirus outbreak — have dimmed the prospects of an increase in U.S. LNG shipments to China.

—Read the full article from S&P Global Market Intelligence

Feature: Uneven impacts expected as capex cuts trickle down to gas pipelines

Billions of dollars in spending cuts by producers and pipeline operators likely will reshape what and when natural gas midstream infrastructure is developed over the next several years. But the deep capital expenditure cuts and broader energy market woes are likely to carry uneven ripple effects for interstate natural gas pipeline projects, according to a range of analysts.

—Read the full article from S&P Global Platts

Global steel sector faces uncertain road to recovery in wake of pandemic

Steelmakers responded quickly to the sudden plunge in demand caused by the coronavirus pandemic with capacity cuts, but the timing and extent of a recovery remains uncertain with key consuming industries remaining under pressure. As of May 18, production stoppages had halted 7% of global output capacity excluding China, according to research from VTB Capital. Europe's already strained steel sector has borne the brunt of shutdowns as the coronavirus spread from east to west, with 18.9 million tonnes or 12% of its capacity closed, while 13.6 Mt or 15% of capacity was idled in the U.S.

—Read the full article from S&P Global Market Intelligence

China fast-tracks infrastructure investment, will support steel demand

China has picked up the pace of new infrastructure project approvals in 2020, with more support expected to be announced during the "two meetings" starting in Beijing this week, helping to drive steel demand. Over January-April, China approved nine airport projects with a total investment of Yuan 100.16 billion ($14.1 billion), equivalent to 55% of total approvals in 2019, according to S&P Global Platts analysis.

—Read the full article from S&P Global Platts

Iraq, Saudi Arabia vie for oil crown in India as coronavirus hits demand

Saudi Arabia is wrestling with Iraq to be the No. 1 oil exporter to India as OPEC's two biggest producers fight for dominance in the world's third largest oil importer amid the coronavirus outbreak. Saudi Arabia exported 1.084 million b/d to India in April, beating Iraq's 760,000 b/d, according to Kpler data. Iraq had been the main oil supplier to India since 2017 as it replaced Iranian and Venezuelan crudes, which are currently under US sanctions. In March, Iraq shipped 969,000 b/d vs Saudi Arabia's 716,000 b/d.

—Read the full article from S&P Global Platts

ESG in the Time of COVID-19

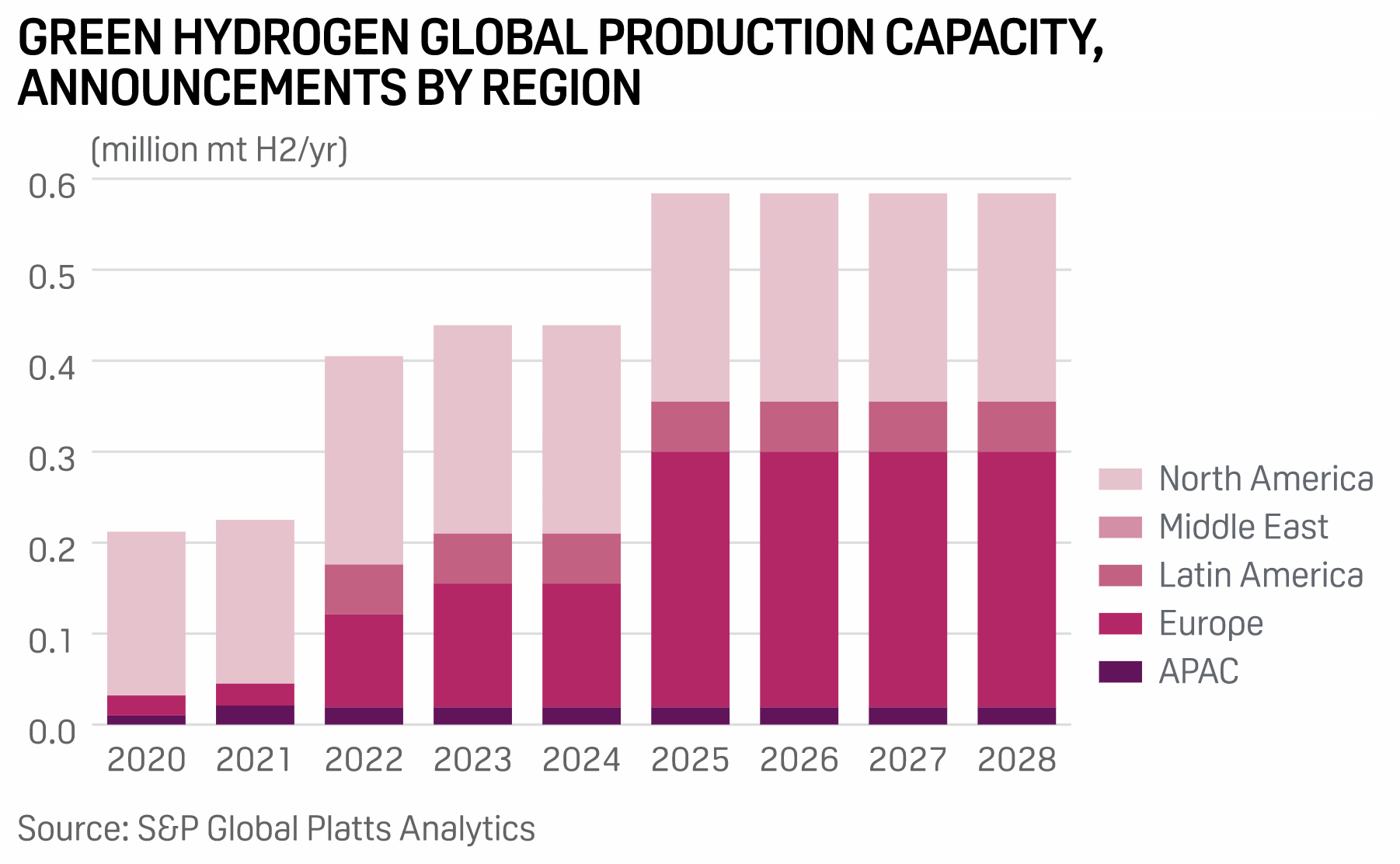

Green hydrogen developer plans California startup of world's largest facility

The developer of what is said to be the world's largest green hydrogen production facility said Wednesday it plans to start operations in southern California by 2023, promising to supply the state's burgeoning market with the zero-carbon fuel at a cost competitive with conventional hydrogen production technology. SGH2's Lancaster, California plant will produce some 40,000 tons of green hydrogen annually, sufficient to fuel 2,200 fuel cell electric vehicles per day. The plant also dramatically expands the US' announced production capacity for the carbon-neutral fuel, currently estimated at 180,000 tons/year, according to S&P Global Platts Analytics.

—Read the full article from S&P Global Platts

Extended tax credit makes US a 'bright spot' in global renewables slowdown – IEA

The impact of the coronavirus pandemic will cause a temporary dip in the pace of global renewables installations in 2020, slowing down the green energy expansion for the first time in two decades, according to the International Energy Agency. But growth in the U.S. and China is expected to be largely undeterred as investors rush to complete projects before tax credit and subsidy phase-outs. The agency, or IEA, predicts that the world will add 167 GW of renewable power capacity in 2020, 13% less than in the previous year, it said in its latest market update on May 20. Although installation levels will likely rebound to 2019 levels next year, the IEA now expects growth for 2020 and 2021 combined to be 10% lower than it had previously forecast before the outbreak of the virus disrupted supply chains and hampered construction schedules and financing activity.

—Read the full article from S&P Global Market Intelligence

With cleaner options available, data centers double down on diesel

The global coronavirus pandemic has driven "two years' worth of digital transformation in two months," according to Microsoft Corp. CEO Satya Nadella. While some segments of the economy are in a tailspin, demand for Microsoft's online services and infrastructure is booming. Microsoft and other tech giants, including Amazon.com Inc., Apple Inc., and Google LLC, as well as smaller multi-tenant data center specialists like Digital Realty Trust Inc., Equinix Inc. and Switch Inc., are aggressively adding data centers to meet surging demand. Those facilities are power-hungry, and much of the power they consume comes from fossil fuels, including backup generators that burn diesel fuels, one of the most carbon-intensive sources of electricity. Data center operators have amassed an impressive portfolio of wind and solar power contracts to fuel their facilities. But variable renewable resources rely heavily on natural gas-fired generation when the sun is not shining and the wind is not blowing. And data centers remain dependent on diesel-fired backup to keep operating when the grid goes down.

—Read the full article from S&P Global Market Intelligence

EU hydrogen strategy to drive use in industry, transport: Simson

The European Commission's upcoming EU hydrogen strategy paper is to look at how to drive demand in a range of sectors, including heavy industry and transport, according to EU energy commissioner Kadri Simson. The hope is that hydrogen can help lower emissions in these difficult to decarbonize sectors, as part of the EU's efforts be climate-neutral by 2050, Simson told the European Parliament's energy committee late Tuesday. The EC's paper is to look at how to use hydrogen in new ways, how to produce it competitively at scale, and how to speed up research and development to give EU industry an edge in global markets.

—Read the full article from S&P Global Platts

The European Commission plans draft EU green battery rules by October ahead of EV surge

The European Commission plans to propose EU sustainable battery rules by October in a bid to challenge China's dominance of the global battery market, which is projected to grow to Eur250 billion per year ($274 billion) by 2025. The EC hopes the rules will become binding by 2022, in time for an expected surge in electric vehicle output in 2023, EC vice-president Maros Sefcovic said after a European Batteries Alliance video conference on Tuesday.

—Read the full article from S&P Global Platts

Move over Millennials: ESG Investing Is a Multigenerational Conversation

The COVID-19 pandemic has shaken financial markets and led many market participants to take a closer look at their investments. While emotionally and psychologically challenging, these selloffs can create opportunities to enhance long-term portfolio objectives. In this environment, advisors can demonstrate their value by helping clients invest in strategies they find meaningful and motivating. Investors are reimagining the future state of investing in the aftermath of the pandemic, and record flows into environmental, social, and governance (ESG) ETFs undoubtedly reflect that mindset. Assets in ESG ETFs and ETPs listed globally increased by 4.93% at the end of February 2020, to a new record of USD 67.99 billion. The recent surge of ESG ETF asset growth raises the question of who is investing in ESG-focused funds.

—Read the full article from S&P Dow Jones Indices

Banking Sector Under Pressure

Big bank loan growth lags as corporate paydowns offset small business activity

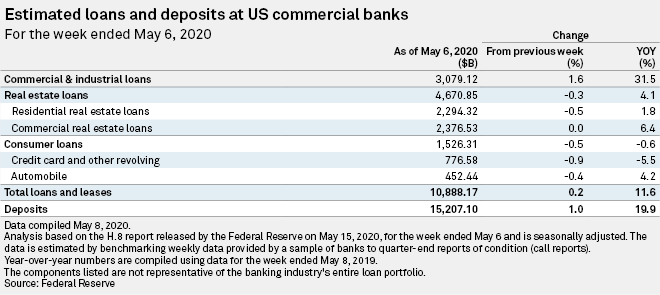

Small U.S. banks have continued to post blistering growth in commercial lending as federal small business relief loans pile up on balance sheets, while increases at large banks appear to have been restrained by paydowns of corporate credit lines. Meanwhile, consumer loans continued to drop across the industry. The widespread collapse in consumer spending amid the COVID-19 pandemic appears to have outweighed a deterioration in credit card payment rates as borrowers opt into forbearance programs offered by lenders. Excluding the 25 largest banks by assets, commercial and industrial lending increased by 3.9%, or $34.2 billion, during the week ended May 6, according to seasonally adjusted data in the Federal Reserve's most recent H.8 report on commercial banks operating in the U.S. Overall, C&I loans have increased 36.7%, or $247.06 billion, at these banks since Feb. 26.

—Read the full article from S&P Global Market Intelligence

Extraordinary Actions for Unprecedented Times: Bank Responses to COVID-19 Crisis in Lending, Deposits and Cash Management

In mid-April, Greenwich Associates and S&P Global Market Intelligence launched a study to track the banking industry’s response to the COVID-19 crisis. A total of 36 wholesale banking divisions from 25 U.S. commercial banks participated in the first joint COVID-19 Response Study.

—Read the full report from S&P Global Market Intelligence

Many Chinese banks raise 2019 dividends, drawing queries from analysts

At least two-thirds of listed Chinese banks are returning more of their 2019 earnings to shareholders, a move that pleases investors but raises questions from analysts concerned about the lenders' draining of capital buffers amid the economic slowdown. Among the 45 listed Chinese banks that disclosed dividend information for both 2018 and 2019, 30 increased their 2019 payout ratios by an average of 698 basis points from a year earlier, according to data from S&P Global Market Intelligence.

—Read the full article from S&P Global Market Intelligence

Written and compiled by Molly Mintz.

Content Type

Location

Language